Job growth fell well short of expectations in February, as the economy added the fewest workers to payrolls since 2017. Hiring slumped in several industries during the month, but trucking employment increased for the tenth consecutive month.

The Bureau of Labor Statistics (BLS) reported that the economy added just 20,000 workers to payrolls in February, down from a upwardly revised 311,000 gain for January. This fell well short of consensus estimates of 175,000 and marks the weakest monthly gain since the 18,000 jobs added in September 2017.

At an industry level, there was plenty of weakness to be found in the February report. Construction employment, which had increased in every month since the middle of 2016, fell by a whopping 31,000 in February, marking the largest single month decrease since 2010. Manufacturing employment rose by 4,000 workers in February, marking the slowest pace of hiring in 18 months. Retail employment declined for the fourth time in six months, falling by 6,100 during the month.

There were a few bright spots for February however. Job growth slowed, but wage growth improved by 0.4 percent from January’s levels. Annual growth in average hourly earnings is now 3.4 percent higher than at this point last year, which is the fastest pace of wage growth since the second half of 2019. In addition, data from the household survey was more positive, showing that the unemployment rate fell to 3.8 percent in February, nearing the multi-decade lows seen late last year.

Transportation hiring slips, but trucking continues to add workers

The transportation and logistics sector also struggled in February, as payroll employment fell by 3,000. Most of this weakness was driven by a drop in employment among parcel companies, however, which fell by 9,700 during the month. Warehousing and storage continued to add jobs at a rapid pace, with payrolls rising by 3,900 in February.

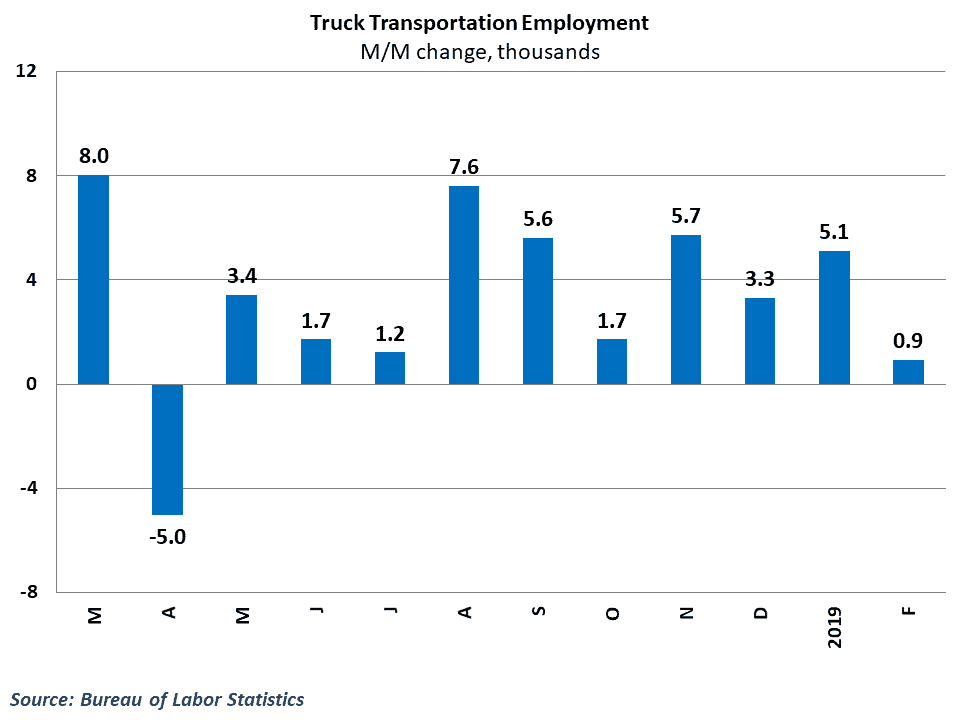

Hiring within trucking also managed to increase during the month, as payrolls rose by 900 in the industry. In addition, gains from December 2018 and January were revised upward, leaving the overall picture of employment in the industry fairly bright. Trucking employment is now 2.7 percent higher than at this point last year, outpacing the 1.7 percent growth in the overall economy.

Behind the numbers

The headline jobs number was dismal by any estimation, and a number of factors likely played a role in the disappointing results. For one, the previous three months were exceptionally strong, including the 300,000+ gain in January. Some of the February weakness is likely just some normalization after strong hiring over the previous three months. It is also worth remembering that exceptionally cold temperatures and snowstorms in late January and early February might have influenced some of the hiring during the month, particularly in the weather-sensitive construction industry.

Results from the month also serve as a useful reminder that the unemployment rate and the jobs number come from separate surveys, with the latter coming from a survey of businesses while the former comes from household responses. Over the long-term, these numbers move in line with each other, but February’s household results showed lower unemployment and over 250,000 more people reporting they were employed.

So, what is to be made of the labor market outlook after the February report? The jobs picture was already expected to shift to a high wage growth, slower job growth environment in 2019 as the supply of available workers gets increasingly smaller. In addition, FreightWaves has argued over the past couple of months that movements in the labor market typically lag behind growth in the economy overall. As the economy showed signs of slowing in late 2018 and early 2019, businesses were bound to begin easing the pace of hiring in the economy. February’s results were more exaggerated than would be expected, but both of these factors are likely at play here.

Going forward, there will be additional scrutiny on the March numbers when they become available. One month of poor data is not enough to change the outlook entirely, but it is enough to raise questions. Job and wage growth provide an important foundation for consumer spending, and data in upcoming months will reveal whether February results were just an anomaly, or the start of a legitimate change in the trend.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.