As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Wednesday, August 1st.

Overview:

Economic conditions as they relate to freight remained generally solid throughout the month, as health in consumer spending and business investment continue to drive demand for freight in the 2nd quarter. Most of the data released in June (predominantly coving May activity) suggest that the economy is growing at a rapid pace during the quarter.

With growth fundamentals remaining intact, much of the focus in the economy shifted towards policy in June, as the Trump administration has taken an increasingly hard line in its stance towards trade with other nations. Beginning with import quotas on steel and aluminum from Brazil and South Korea, and ending with a threat to remove the US from the World Trade Organization, this month saw an escalation of trade threats between the US and many key trade partners.

Reports are beginning to filter in within the US economy which suggest that these tougher trade policies are affecting domestic businesses. Survey data within the manufacturing sector has highlighter the surge in steel and aluminum prices in the aftermath of the tariff announcements. US manufacturer Harley Davidson made headlines last week by announcing that they would move some of their production over to Europe to avoid potential tariffs. Moreover, even when plans have yet to be finalized for tariffs, and move have yet to be implemented, there is a growing cloud of uncertainty for businesses engaged in international trade in some of these affected areas and industries.

By itself, a global escalation of tariffs and other protectionist policies is likely not enough to throw the US economy into recession. However, much of the growth throughout the course of the past 18 months has been driven by increased business investment and soaring confidence among consumers and businesses. As tariffs affect trade and earnings of US businesses, there is potential for a severe shock to business and consumer sentiment, which could cause additional damage to the economy overall. As a result, there exists a decent amount of risk in the US economy despite the fact that most major sectors have been performing well.

Manufacturing and industrial production

Results from the manufacturing sector faltered a bit during the month, despite generally strong fundamentals. Industrial production slipped 0.1% in May, interrupting a string of solid performance in the industrial sector. Weakness in the auto industry was one of the primary drivers in May, as a fire at one of Ford’s key suppliers disrupted production of the company’s F150 truck. Still, excluding auto’s performance, manufacturing production was down during the month. Factory orders for durable goods also softened in May, suggesting that the sector may be losing some momentum. Mining and energy activity remains quite strong in the economy, which continues to help the overall industrial production results.

Survey data continues to point towards strength in manufacturing, however, as healthy consumer spending and solid gains in business investment and inventories have kept demand for factory output strong. It is clear that US producers have been feeling the sting of rising prices as a result of recent tariff changes, as responses from both ISM index and regional Fed surveys have highlighted the surge in commodity and raw material prices since the start of tariff announcements in late February.

Trend to watch: Survey data has been suggesting that demand has been present for US manufactured goods, but companies have struggled to keep up with orders. Labor shortages, rising prices, and scarcity of freight demand are all likely playing a role here, and it will be interesting to see whether these issues will curb a further acceleration in manufacturing in the economy.

Retail and inventories

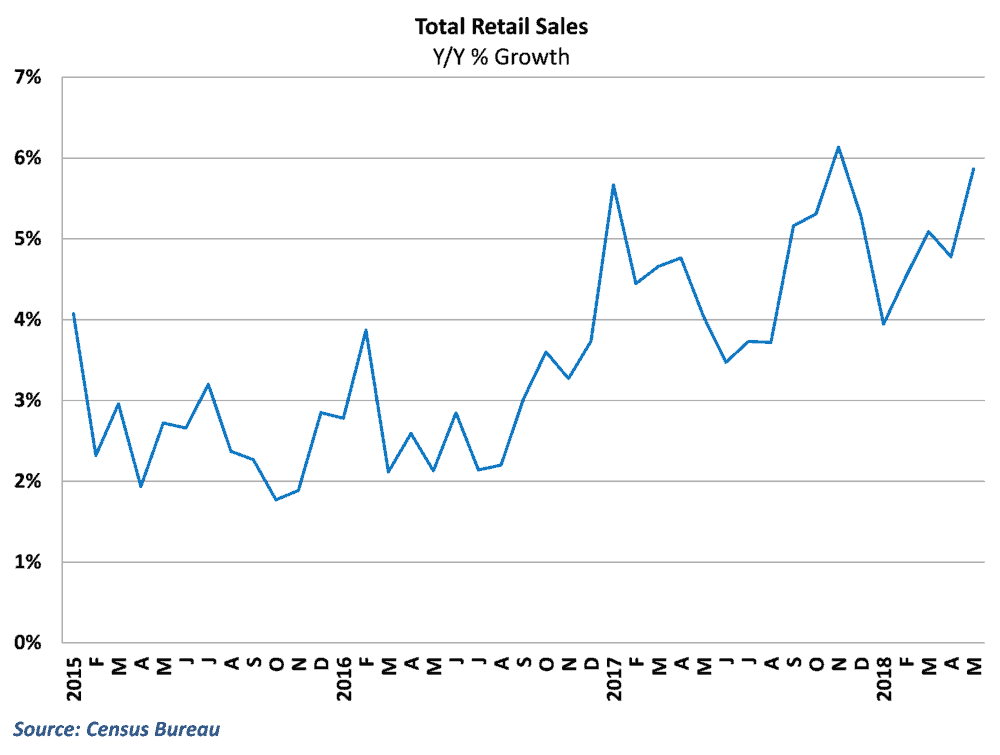

Retail performance continued to push ahead with another solid month of growth in May. Similar to last month, the gains in retail sales during in May were broad-based, with only sporting goods stores and restaurants registering declines during the month. This is a positive sign for overall growth during the 2nd quarter, and is a signal that the recent tax cuts, high consumer confidence, and rising household net worth are outweighing any concerns from rising inflation.

Inventories also posted solid gains during the month among wholesalers and retailers, although much of the gain was driven by a buildup of inventories in the auto industry. Nonauto inventories remain fairly lean in the economy, particularly in the retail sector, which will continue to put pressure on carriers to meet tight inventory replenishment schedules.

Trend to watch: It appears as though all the positives that have been behind the US consumer since the start of the year are finally beginning to translate into purchases in the real economy. The retail numbers are nominal, so rising prices are playing some role in the strong retail reports lately, but the underlying activity looks to be strong in the 2nd quarter.

Labor markets

Labor market news was overwhelmingly positive during the month as job growth beat expectations with 223,000 jobs added in May. This helped push unemployment down to a near 50-year low of 3.8%. Wage growth also surprised on the upside during the month, as earnings look to accelerate throughout the remainder of the year

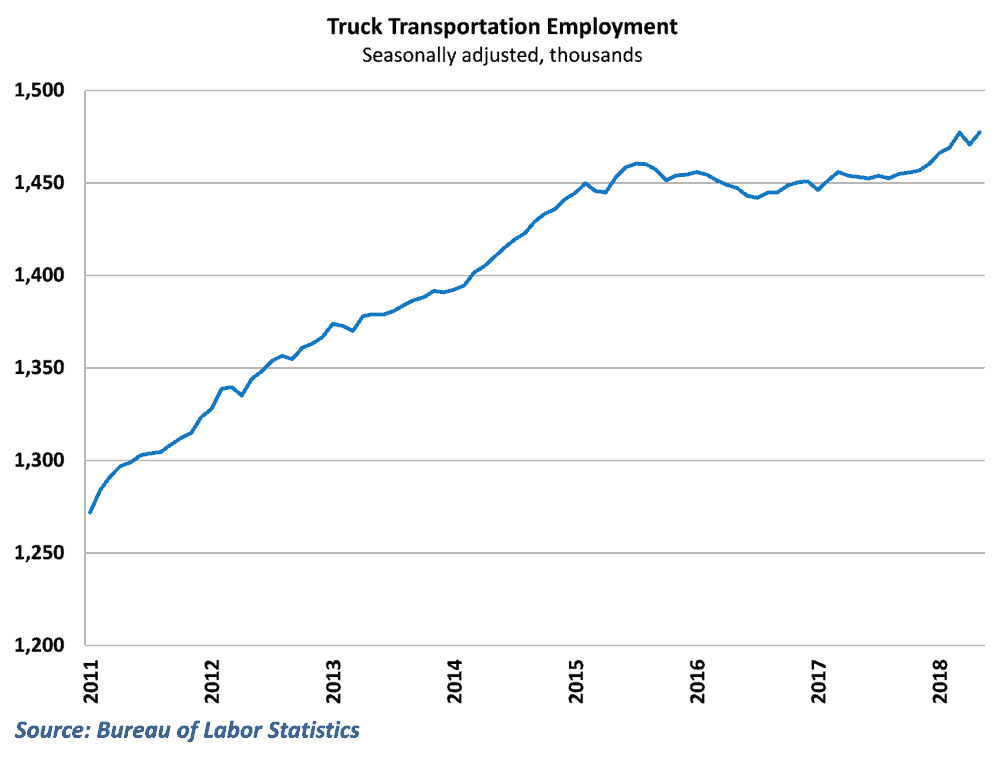

Trucking hires rebounded nicely in May after April’s unexpected decline, with 6,600 jobs added in truck transportation during the month. The trucking industry has now added jobs in eight out of the past nine months and has increased payrolls by 25,000 since the 3rd quarter of last year. This is a positive sign, as more jobs means that capacity is expanding in a very tight trucking market. Still, even with the improved shown in recent months, trucking employment is only 1.7% higher than it was at this point last year. This is roughly the same pace as the economy overall, but lagging behind growth in other industries such as manufacturing and construction.

Trend to watch: Wage growth improved in May, but hourly earnings have generally hovered around 2.5% more than a year now. This was not a serious concern when inflation was low, but price increases have picked up in recent months. If wage growth doesn’t start to show some sustained acceleration, much of the gains in earnings will be eaten away by rising inflation in the economy.

Housing and construction

Housing data generally improved during the month, as home starts, new home sales, and total construction beat expectations. Housing inventory remains historically tight in the economy right now, and continued demand for homes should help propel freight demand for construction materials and lumber.

Part of the consequence for the lack of available inventory in housing has been continued disappointment in existing home sales, which declined in May. Existing homes sales are a vital driver of demand for large items such as furniture and appliances, as well as construction materials for remodeling, and weakness in existing sales has restrained growth in some of these associated purchases

Trend to watch: Existing housing supply is facing severe constraints, which has pushed up the prices for existing homes even as new home prices fall in the economy. With mortgage rates also on the rise, the affordability of existing homes is becoming an issue.

International Trade

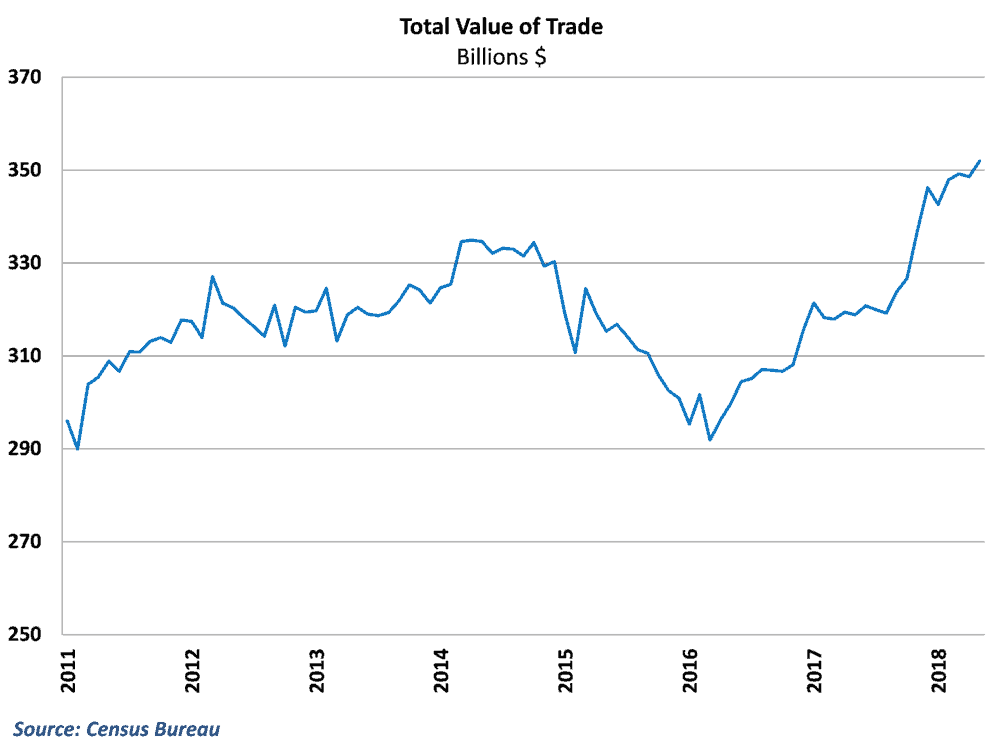

In international trade, the goods deficit declined for the third straight month in May. Unlike last month however, the decline in the deficit came with both exports and imports growing during the month. Consensus forecasts called for a significant widening of the deficit during the month, and the May results suggest that international trade will be a significant contributor to GDP growth in the 2nd quarter when results are released at the end of this month.

A surge in agricultural exports helped mask some of the other issues in trade, however. There was some evidence in the May results that recent tariffs have begun to take hold, as targeted industries such as automobiles and industrial supplies saw a decline in both imports and exports during the month.

Trend to watch: Tariffs and trade policy are likely going to play a larger role going forward. The Trump administration took a significantly harder stance on trade throughout the month of June, rescinding exemptions on many of the US’ key trade partners and issuing fresh threats on China, the European Union, and the World Trade Organization. May’s impressive export performance was likely to be reversed in upcoming months anyway, but tougher trade policy is only going to exacerbate things going forward.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.