As part of FreightWaves’ overall coverage of freight markets, it publishes a summary of the changes in the economy over the past month, both in terms of the data releases and developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide to trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Monday, June 3.

Overview:

Developments over the past month continue to point towards an economy that lost considerable momentum. Data releases in April (mostly covering March activity) were fairly encouraging and suggest that many of the areas of the economy that drive freight demand should improve going forward. Employment, retail and new orders all surprised on the upside during the month, signaling that better times may be ahead for the freight economy.

It is worth remembering that the government shutdown, polar vortex and Midwest flooding all hit the economy in the early parts of 2019 and likely hamstrung growth during the quarter, particularly on the goods side of the economy. As the freight economy normalizes following these events, growth should improve in the second quarter and beyond. FreightWaves still expects that the pace of growth will be slower than in 2018, but freight demand should regain some momentum after a poor first quarter.

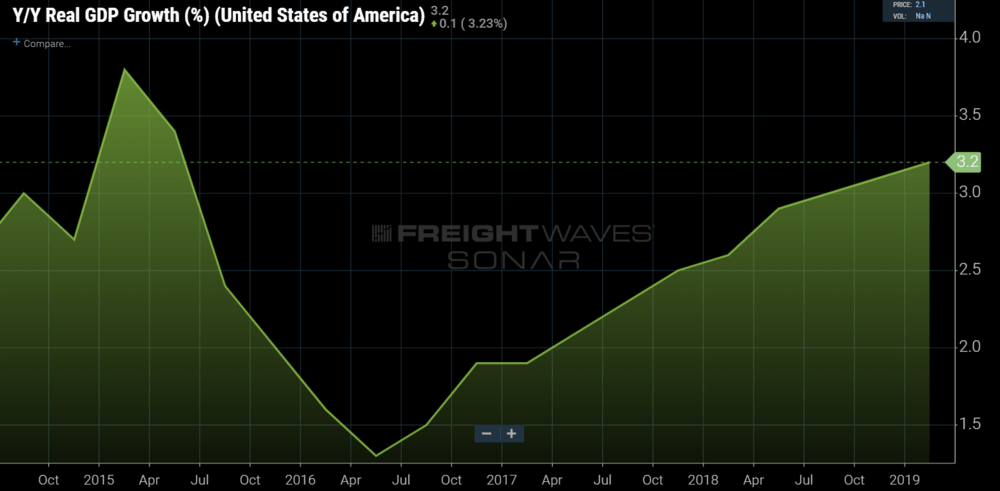

GDP

Initial estimates of first quarter U.S. gross domestic product (GDP) showed that the economy grew at a 3.2 percent pace of growth, up from the 2.2 percent pace in the previous quarter. This crushed consensus estimates of 2.1 percent and put year-over-year growth at a near four-year high of 3.2 percent.

While this was good news for the economy overall, the details in the GDP results were less favorable for freight performance. Key components of GDP that drive freight demand such as consumer spending on goods, business investment on equipment, housing investment and trade volume were all either flat or negative during the first quarter.

Trend to watch: Temporary factors such as poor weather and tariff-related trade fluctuations likely played a role in the poor performance during the first quarter. Signs are already emerging that suggest that conditions on the goods side of the economy are beginning to improve, so freight conditions should improve in upcoming quarters

Industrial production and manufacturing

Industrial output disappointed again in March, dropping 0.1 percent from February’s levels. Manufacturing production, which excludes mining and utilities from the total, was flat during the month after back-to-back declines at the start of 2019. For the quarter, manufacturing production fell at a 1.1 percent annualized pace, marking the largest quarterly decline since the end of 2015. Year-over-year-growth in manufacturing is now hovering around 1.0 percent, down sharply from the multi-year highs seen in the third quarter of 2018.

The good news is that there are some positive signs emerging from the manufacturing sector. Durable goods orders surged during the month, and a jump in orders for capital goods suggests that the appetite for business investment spending may be improving. Survey data from the Institute of Supply Management (ISM) also made positive strides in March, giving additional optimism for the manufacturing sector

Trend to watch: ISM data has consistently been in expansionary territory even as manufacturing has stalled over the past several months. Updates on April industrial production will be released in mid-May, and we will be watching to see whether the actual production data will catch up to survey results.

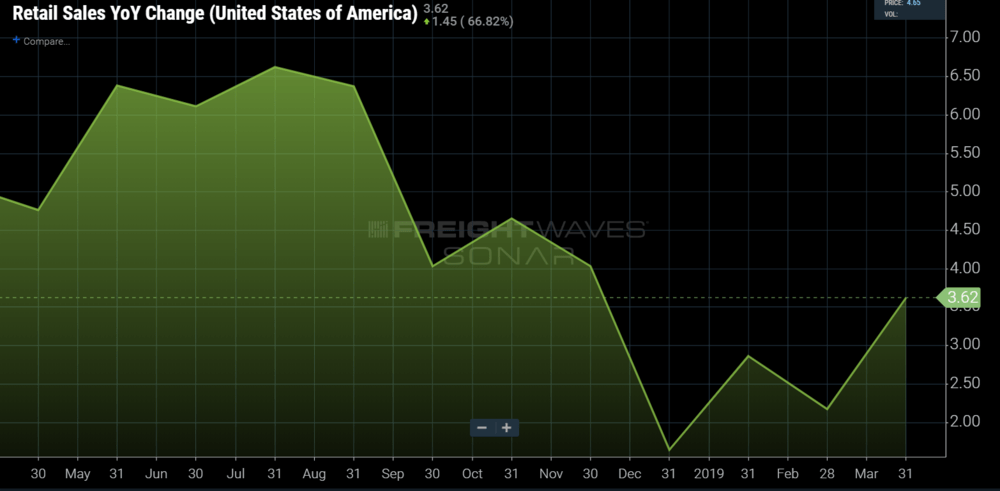

Retail and inventories

Retail sales activity surged in March, rising 1.6 percent during the month for the largest monthly gain in over a year. Growth during the month was boosted by surging sales at auto dealerships and gasoline stations, but core sales excluding these categories still expanded by a healthy 0.9 percent. Year-over- year growth in retail sales jumped back up to 3.6 percent as a result, and looks to be on solid footing in the second quarter.

On the inventory side, the total inventory/sales ratio edged up to 1.39 in February, continuing a general upward trend for inventories that began in the third quarter of 2018. While much of the buildup in inventories in the fourth quarter was driven by tariff-related imports, poor sales is likely behind the continued buildup in inventories in the economy. As activity in retail and manufacturing begins to gain momentum, inventory/sales ratios are likely to come back down.

Trend to watch: Retail sales are set to be released in the middle of the month, and a second consecutive strong performance should be enough to erase any lingering concerns about the health of consumer spending in the second quarter.

Labor markets

Job growth rebounded nicely in March after February’s disastrous results, as the economy added an impressive 196,000 workers to payrolls. The strong pace of hiring was enough to keep the unemployment rate close to a near 50-year low at 3.8 percent. Wage growth fell a bit short of expectations during the month, but remains on a solid upward trend.

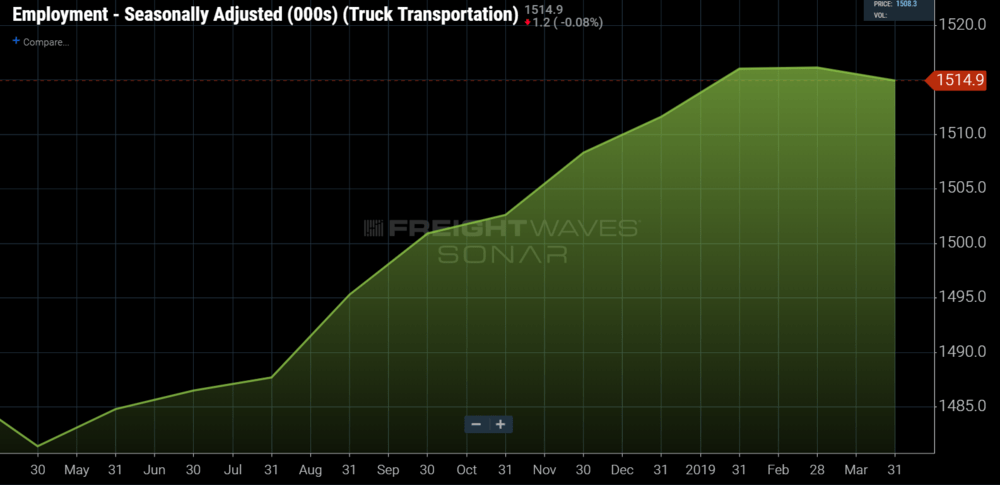

Trucking hires declined for the first time in nearly a year in March, as employers in the industry reduced payrolls by 1,200 during the month. Trucking employment is now 1.9 percent higher than at this point last year, which is still faster than the 1.6 percent pace of employment growth in the overall economy, but slower than the pace of growth in the industry throughout most of 2018. Job openings within the transportation and logistics industry have also cooled in recent months, however, which suggests that the labor market in the industry is no longer much tighter than it is for the economy overall.

Trend to watch: Solid overall job growth is expected when April data is released on May 3, but the performance in the trucking industry is worth keeping an eye on. Given the overall softness in freight demand in recent months, March’s poor showing could be an inflection point for hiring in the industry and a second consecutive decline could be the start of a downward trend in hiring.

Housing and construction

The first quarter was underwhelming on the supply side of residential construction as total housing starts ended March at 1,139,000 units for the month. Housing starts have been hampered by weather events in recent months, which should lead to some pent-up activity, but also face significant structural challenges that limit the amount of construction that can take place. The construction industry has struggled with limited labor supply and a shortage of developed lots for much of the past year

On the demand side, the results were better as new home sales increased for the third consecutive month. However, this was offset by a decline in existing home sales, as a lack of inventory of homes for sale continues to restrain home-buying activity. Solid job and income growth combined with easing mortgages rates should keep demand fairly solid in upcoming months, though limited housing inventory will continue to be a factor.

Trend to watch: Trends in housing starts have clearly turned negative since the third quarter of 2018, but weather events have likely played a role in some of the recent softness. Flooding in the Midwest likely also played a role in March’s poor showing, but there is significant building and repair work that will take place in upcoming months that should give a boost to the construction sector.

International Trade

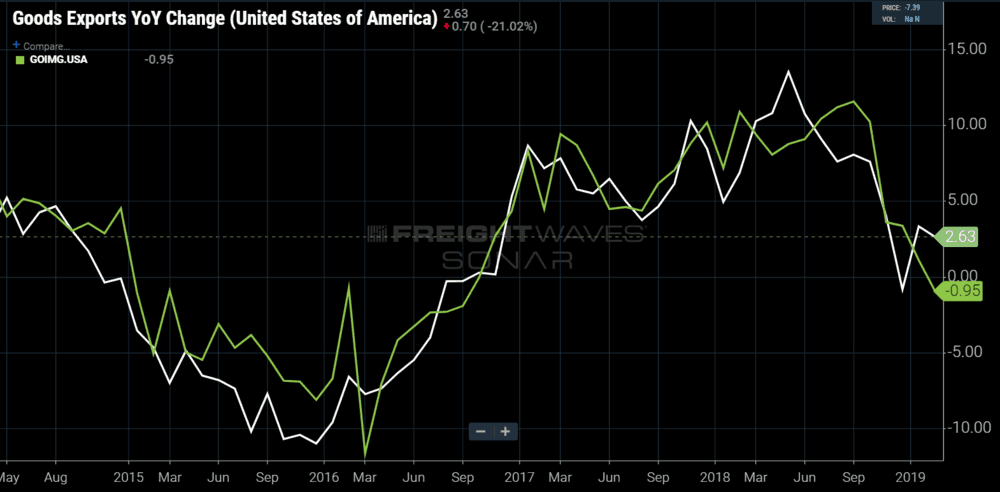

The goods trade deficit narrowed to -$72.0 billion in February, down from -$73.2 billion in the previous month. This was the second consecutive month of narrowing deficits, and marks the smallest trade deficit on the goods side of the economy since June 2018.

Goods exports performed well during the month, rising 1.5 percent from January’s levels as year-over-year growth remained fairly solid at 2.9 percent. Most of the gain was driven by a surge in commercial aircraft exports, however, while other exports were essentially flat during the month. Goods imports rose by a more modest 0.4 percent, and tougher comparisons to last year pushed year-over-year growth into negative territory at -0.9 percent.

Trend to watch: Tariff-related fluctuations have increased the volatility in the monthly numbers, but trade volumes have clearly decelerated in recent months. U.S. growth appears poised to improve which should boost import volume, but exports are not likely to improve significantly until global growth strengthens.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.