Recent results show that retail activity continued to expand in November, in a sign that one of the key components of freight demand remains healthy at the end of the year. Results from the manufacturing sector were far less encouraging however, as activity stalled during the month.

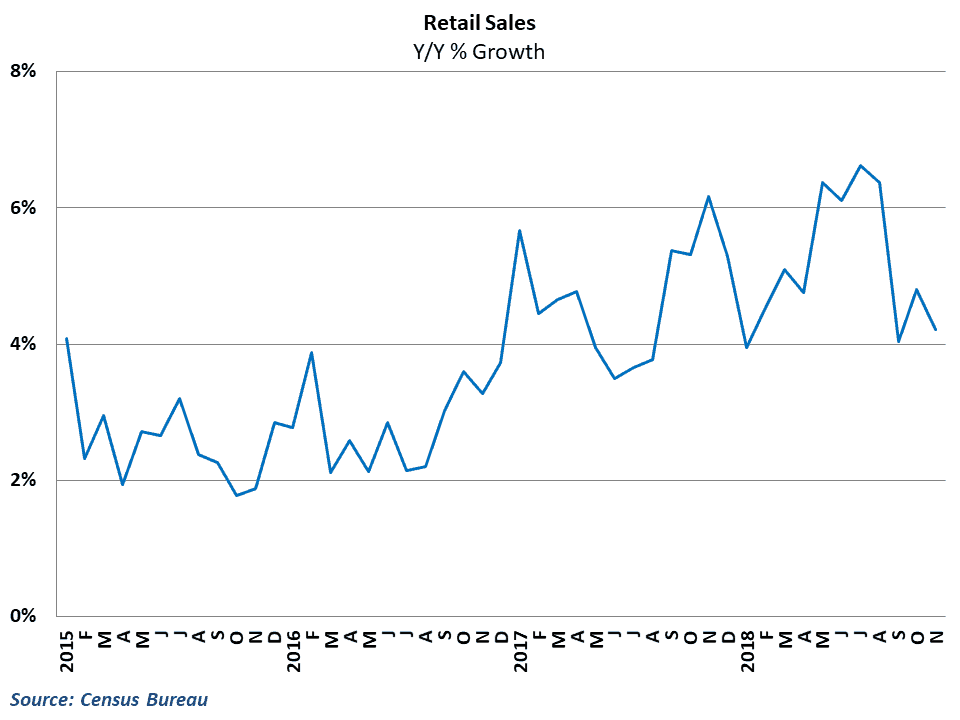

The Census Bureau reported this morning that retail sales in the economy rose 0.2% in November from October’s levels. This beat out consensus estimates of a gain of 0.1%, and comes on the heels of an upwardly-revised 1.1% gain in the previous month. Year-over-year growth moderated slightly to 4.2%, but remains generally solid as we near the end of the year.

The details of this morning’s report were even more encouraging, as the gain in retail spending came despite a 2.3% drop in gasoline sales during the month. Retail figures are not adjusted for inflation, so the tumble in gasoline prices that began in the latter part of October weighed down sales figures throughout November. Core retail sales, which exclude motor vehicles and gas, rose 0.5% in November and are now up 4.6% from this point last year.

Gains during the month were generally broad-based with every other major industry category except for building materials, apparel, and restaurants expanding during the month. Electronics stores, furniture stores, and nonstore (mostly online) retailers led the way in November, with each industry seeing stronger than 1% monthly growth.

Cold weather boosts industrial output, manufacturing outlook softens

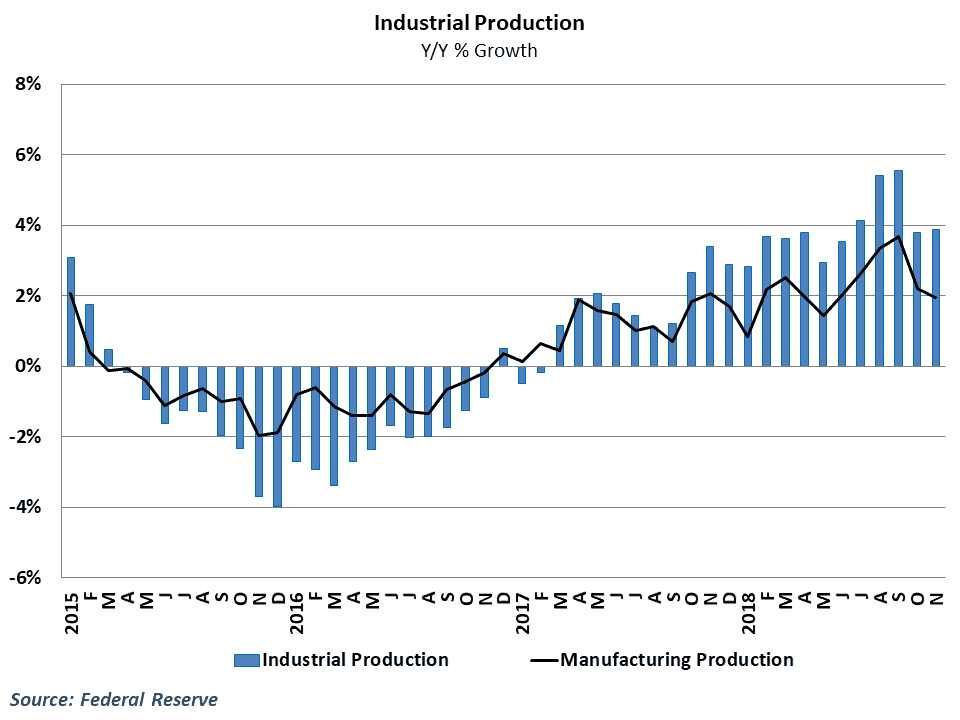

The Federal Reserve also released results from the industrial sector earlier today, showing that total industrial production rose by 0.6% in November. This exceeded consensus expectations of a 0.4% gain, though this was offset by a sizeable downward revision to October’s results. Yearly growth improved slightly to 3.9% in November, but remains well below the multi-year highs seen earlier in the year.

Unlike retail sales, the details with the industrial production report were far less favorable. Growth during the month was boosted by significant gains in mining and utilities production, which jumped 1.7% and 3.3%, respectively. The gain in utility production was likely aided by unseasonably cold weather in much of the country during the month, with households and businesses needing additional energy for heating. Manufacturing industrial production, which excludes mining and utilities, was flat in November after a revised, -0.2% showing in October. Year-over-year growth in manufacturing has now fallen to 2.0% and appears to have lost significant momentum as we near the end of the year.

Behind the Numbers:

On the retail side, the data from November suggest that consumers have shrugged off the recent decline in equity values and continue to support growth in the overall economy. This is good news for overall holiday season results, as core sales excluding autos and gas performed better than expected. We still expect holiday sales, which exclude autos, gas, and restaurants, to end up approximately 4.5% higher than they were last year. The huge gain in nonstore retail spending in November helps to underscore the importance that e-commerce has played in the early part of the peak holiday shopping season, as online shopping continues to snatch additional share of the consumers wallet.

The headline industrial production number was certainly strong, but weather-related boosts are typically reversed once weather returns to normal. The manufacturing results were not good for the month, and the revisions to September and October suggest the sector is barely expanding towards the end of the year. This is particularly true on the nondurable side of manufacturing, which has outright declined in each of the last four months and is less than a percentage point higher than it was a year ago. There was plenty of weakness to go around in this morning’s report, including big declines in petroleum products and clothing production, and it now looks like the manufacturing sector is quite a bit weaker than previously thought.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.