As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Monday, October 1st.

Overview:

Economic conditions as they relate to freight demand continued to push ahead at a solid pace in the 3rd quarter. Strong growth in consumer and business spending in the economy continue to drive demand for freight, keeping capacity tight in the market and granting carriers with significant pricing power. All is not perfect, however, as construction and housing activity continue to lag behind the rest of the economy. In addition, export growth has stumbled after robust growth in the previous several quarters.

On the supply side, trucking capacity continues to expand gradually. Carriers have been taking steps to increase driver pay to attract workers through higher wages and larger sign-on bonuses. For the most part, this appears to be gaining some traction, as hiring within trucking has expanded consistently over the past three quarters. The number of trucking employees increased again in July and the pace of hiring within the industry is outpacing job growth in the economy overall. Of course, the goods side of the economy is also growing at a faster pace than the economy overall, and this should keep capacity tight in upcoming months.

GDP

US GDP grew at a revised 4.2% pace during the second quarter as a rebound in consumer spending and continued strength in business investment helped drive activity. The details of the quarter were little changed in the revised estimate, with the economy receiving a big boost from international trade and consumer spending, which helped offset a decline in inventories during the quarter.

Trend to watch: The 2nd quarter was one of the strongest quarters of this current expansion, but don’t expect this growth to continue. Many of the big contributors to growth during the 2nd quarter should slow down, and in the case of international trade, may be negative in the 3rd quarter. On the other hand, inventories will likely be a contributor to growth during the 3rd quarter, so look for GDP growth to settle in the 3% range.

Manufacturing and industrial production

Industrial output slowed slightly at the start of the 3rd quarter as total industrial production grew just 0.1% during the month. However, the softness in July was offset by some positive revisions to previous months. Year-over-year growth has jumped above 4% in the third quarter and is now at the highest point in nearly seven years.

Declines in mining activity and utility production helped hold back the overall production results during the month. Outside of these sectors, manufacturing activity performed better. Manufacturing industrial production posted a 0.3% gain in July on the heels of a big, upwardly-revised gain in the previous month. Year over-year growth in manufacturing climbed to 2.8% which, like the total, marks the fastest pace of manufacturing production growth in over 6 years.

Survey data has cooled a bit from the elevated levels in May and June, but continues to point to strength in the manufacturing sector. This bodes well for freight demand, as the transportation of supplies to manufacturers and finished products from producers serves as one of the large sources of transportation demand in the economy

Trend to watch: Survey respondents overwhelmingly cited tariffs and labor shortages as the primary concerns for activity going forward. Most said that tariffs were more a threat than an actual problem at the moment, but labor shortages are currently keeping them from meeting available demand. This is likely to remain an issue going forward, and manufacturing may be restrained going forward by capacity issues, much like the trucking industry is.

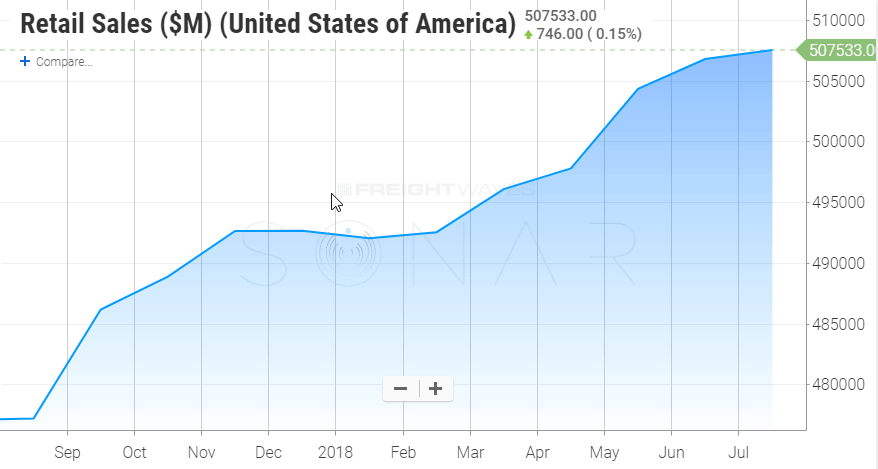

Retail and inventories

Retail performance kept moving forward in the 3rd quarter, as the sector some more impressive gains in July. This marks the sixth consecutive monthly increase in total retail spending. Sales are now 6.4% higher than at this point last year, and year-over-year growth has exceeded 6% in each of the last three months. Solid job, income, and wealth growth have underpinned consumer sentiment and helped sustain consumer spending over the past several months, and as long as this is the case, retail spending should remain strong.

Inventories also posted some solid gains during the month, and will likely grow throughout the 3rd quarter after declining in real terms during the 2nd quarter. Concerns over tariffs are likely boosting imported inventories also, as many businesses may decide to import goods earlier than normal in case the trade environment worsens.

Trend to watch: Retail growth is solid, but inflation is putting some pressure on US households as we enter the second half of the year. Consumer inflation is now faster than wage growth in the economy and is beginning to eat away at some of the other positives that consumers are enjoying.

Labor markets

Labor market conditions were also generally solid during the month. Job growth declined to 157,000 jobs added in July, which is the smallest gain in four months but still a healthy headline number. Unemployment continues to hover near multi-decade lows, declining to 3.9% as labor market conditions remain tight.

Trucking hires continued to make strides in July, with 4,400 workers added to payrolls during the month. This is the 10th positive number in 11 months for the capacity-strapped industry, and serves as a positive sign that many of the steps that carriers are taking to recruit and retain are starting to take hold. Trucking employment is now 1.8% higher than at this point last year, which outpaces the 1.6% growth in overall employment in the economy.

Trend to watch: Much of the gains in employment in recent months has come from enticing some of the marginally attached workers to rejoin the labor force. Broader measures of employment have consistently fallen over the past year even as the headline unemployment number has generally hovered around 4%. These broader measures are also reaching “normal” levels, so it is unclear where the additional workers are going to come from.

Housing and construction

Housing has been perhaps the most consistently disappointment in terms of freight demand since the start of the year. Housing and home building data continued to underwhelm at the start of the 3rd quarter as both starts and sales data fell well short of expectations.

On the sales side, purchases of both new and existing home sales declined again in July. Existing home sales, which make up the majority of home purchases, are now well on their way to declining for the entirety of 2018 despite solid consumer fundamentals in the economy. Affordability has become an issue for home sales, as rising prices and higher mortgage rates have made it more difficult for buyers to find homes within their price range.

On the supply side, home starts rebounded slightly, but well below what most expected given the large decline in the previous month. Home builders have been faced with labor shortages and a general lack of developed lots to build upon, and these factors have pushed up the costs for building. Fortunately, the prices for many materials used in home building have retreated after surging earlier in the year, but the sector is likely to remain challenged for the remainder of the year.

Trend to watch: Home buying typically doesn’t affect freight demand directly, as much of the actual transaction doesn’t involve the movement of goods. However, demand for furniture and appliances is heavily influenced by home purchases and remodeling efforts. These portions of retail have already shown some signs of weakness in recent months, and look for this trend to continue if housing remains weak.

International Trade

In international trade, the goods deficit widened for the second consecutive month in July after narrowing throughout most of the 2nd quarter. Much of this was driven by a decline in exports during the month, as a big decline in agricultural shipments to the rest of the world contributed to a weak overall number.

This weakness is likely payback for tariff-influenced boosts in previous months. Prior to the implementation of Chinese tariffs on US agricultural imports, many Chinese importers brought in goods earlier than they normally would. This provided a big boost to US agricultural exports in the 2nd quarter, which is being reversed now in the economy.

By a similar token, many US importers likely brought in additional goods in July in advance of US tariffs on Chinese imports which were implemented in July and August. This has boosted import numbers recently, and contributed to the surging trade deficit.

Trend to watch: Tariff-induced volatility has made it difficult to determine the underlying trend in trade growth in recent months. Will threats and trade negotiations continuing to loom over the sector, it is likely that fundamental changes will be tough to identify through the rest of the year.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.