Last night, ACT Research released its preliminary estimate for September 2018 net trailer orders: an astounding 58,200 units, which Frank Maly, ACT’s Director of CV Transportation Analysis & Research characterized as “a never-before-seen trailer order level.” The September numbers smashed the previous monthly record set in October 2014 by about 23%. Year over year, trailer orders increased last month by 135%.

One would think that Wabash National (NYSE: WNC), the United States’ only publicly-traded manufacturer of semi trailers, would be having a stellar year. Unfortunately, that is not the case. Before trading last Friday, Wabash released preliminary guidance for the third quarter, and the numbers seem to have disappointed the market: Wabash said it expected operating income between $15.5-17.5M for the quarter, compared to $26.6M year-over-year. WNC shares plunged 22% when the market opened; today Wabash’s stock has settled at around $14.70, representing a 24% decline since September 21.

In a research note on the company, Stifel (NYSE: SF) analyst Michael Baudendistel wrote that “building trailers is harder than it looks.” Baudendistel went on to explain how the Trump administration’s tariffs on aluminum (10%) and steel (25%) have driven up Wabash’s input costs for both raw materials and components, compressing margins at a time when the company is being asked to manufacture more trailers than ever.

“Our understanding is that the company hedges about 70% of the cost of a trailer,” Baudendistel wrote. “For the other 30%, Wabash updates their pricing monthly for changes in input costs using current and forecasted prices so there can be some delay between rising input costs and recovering that cost from customers. Therefore, the input costs issues should get progressively less impactful if input costs stabilize, but headwinds could persist or intensify if input costs get progressively worse.”

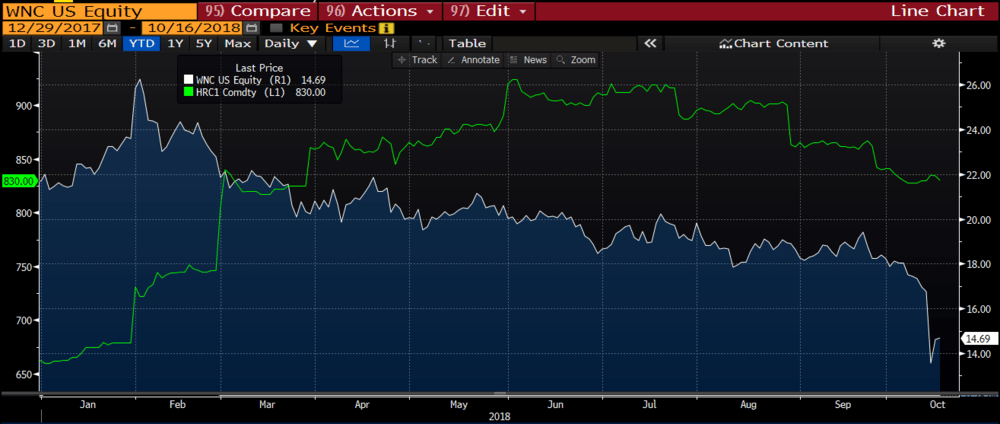

Since the beginning of the year, October 2018 futures contracts for US Coil Steel have climbed 27%, to $834 per short ton. The chart below, from our Bloomberg Terminal, compares the rising price of US Coil Steel (green line) to the falling value of Wabash National stock (white line):

“The third quarter was a challenging and difficult quarter for the Company as a whole,” said Brent Yeagy, president and chief executive officer of Wabash National in a statement. “On the cost side of the business, higher commodity and component costs impacted the quarterly results as raw material costs continued to escalate.”

Stifel and Wabash also both pointed to the difficulties the company has had in realizing revenue from trailers it has built: due to a chassis shortage and strong freight demand, Wabash’s customers are having a hard time sourcing the trucks to pick up the trailers. If customers can’t take possession of the trailers they’ve ordered, Wabash’s cash flows are strained. Yeagy, in his statement, also blamed labor shortages for the company’s lackluster performance despite strong demand for its products: Wabash said higher levels of overtime and lower productivity created unforeseen operating cost pressures at its plants.

“Despite the tough operating environment and preliminary results reflecting a very challenging third quarter,” Yeagy said, “we continue to see strong overall market demand for our products and we are taking proactive steps to reduce the margin impact of U.S. tariff policy, raw material inflation, supply base disruptions and a very tight labor market for the remainder of 2018 and 2019.”

Stifel lowered its price target for WNC to $16 from $19, 9x Stifel’s estimated 2019 EPS.

“Normally, this would provide enough upside to the current market price to justify a Buy,” Baudendistel wrote, “but we believe more than the typical 20% is necessary given the uncertainty of how impactful the input costs, chassis shortages, etc. are expected to be next year.”