There are usually more bulk ships on the high seas than cargoes for them to carry, ergo weak long-term returns for vessel owners. Every once in a while, though, the balance tightens and an unexpected chain of events sends moribund freight rates crashing upwards through the roof.

That’s what just happened with very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude oil), and conditions are still ripe for more VLCC rate spikes in the months ahead due to constraints on tanker capacity that could extend well into 2020.

Executives of crude-tanker owner Euronav (NYSE: EURN) outlined three rising capacity constraints during their quarterly call with analysts on Oct. 29: heightened floating storage, delays for exhaust-gas scrubber installations, and uncertainty over newbuilding designs.

Floating storage is up

On Jan. 1, the IMO 2020 rule goes into effect, requiring the use of fuel with sulfur content of 0.5% or less aboard all ships not equipped with exhaust-gas scrubbers. This will split the market into those using scrubbers and staying with 3.5% sulfur heavy fuel oil (HFO) on one hand and those switching to blended 0.5% sulfur low-sulfur fuel oil (LSFO) or 0.1% marine gas oil (MGO) on the other.

There is considerable uncertainty on how much of each type of fuel will need to be in which location, and this is prompting a move to store various fuel types at sea aboard VLCCs. The more VLCCs that are pulled from service for storage employment, the fewer that compete for spot contracts and the higher the spot rate.

Euronav investor relations head Brian Gallagher estimated that 30 VLCCs are “leaving the global fleet to store various grades of fuel oil” and he further predicted that “some of the vessels storing oil will not return to the trading fleet.”

According to Euronav CEO Hugo de Stoop, “The first candidates to do storage are the older ships, which is good news, because once ships perform storage contracts that are at least several months long, it is more difficult to bring the ships back to the trading fleet. There is more vetting and they are not as easily accepted [by charterers].” In other words, more storage deals should accelerate the scrapping pace and lower capacity.

Scrubber installations postponed

Many of the scrubber installation jobs for VLCCs were scheduled for the fourth quarter, so that these ships could burn cheaper HFO after the Jan. 1 deadline. However, this schedule has coincided with a spike in spot rates. Many VLCC owners would prefer to push back the installations to some time in 2020 and reap the immediate benefits of spot rates, which are currently in the range of $65,000-75,000 per day.

According to Gallagher, “Retrofits are now likely to persist long into 2020 as owners avoid retrofitting during the anticipated strong winter freight season.” This should extend the rate tailwind from capacity reductions for a longer period than previously thought, and it should also increase demand for LSFO in early 2020 more so than originally predicted.

During the recent quarterly conference call of DHT Holdings (NYSE: DHT), executives of that company confirmed that they were delaying scrubber installations for six of their VLCCs. They noted that yards were very flexible in allowing such delays, because they were already overloaded with installation work and could focus on placating clients in other sectors, such as dry bulk and container shipping, in which current spot rates are not as high.

Newbuilding quandary

The floating-storage and scrubber-scheduling issues represent near-term capacity constraints. The newbuilding issue is longer term.

The value of a typical tanker is depreciated over a 25-year time period. Beyond IMO 2020, additional regulations focused on carbon emissions are looming – but their nature remains uncertain. If a newbuilding is ordered today for delivery in 2022, owners (and their banks) are concerned that the upcoming carbon regulations could make the asset obsolete well before it depreciates.

This quandary has kept newbuilding orders unusually now – VLCCs on order now represent just 9% of the on-the-water fleet.

De Stoop explained, “Everybody believes that LNG [liquefied natural gas] will be the transition fuel. The biggest problem is that a newbuilding that uses LNG is at a $15 million premium. So, if your conventional VLCC newbuilding is $90-92 million and you have to add $15 million, that’s significant.

“The only way to justify that is to either be sure that LNG is going to be at such a big discount to LSFO [that it will pay back the premium] or to have a time-charter contract [that compensates for the premium]. We are pretty confident that until there is more clarity [on future regulations], a lot of people will refrain from ordering conventional vessels, and until it is cheaper [to install an LNG system], it will restrain a lot of people from ordering those vessels.”

Euronav’s quarterly losses

Given all the recent headlines on astronomical spot rates, quarterly announcements by listed crude-tanker owners are bound to be a letdown. There is a significant lag – at least one reporting period – between spot rates and quarterly results. What is being reported now is the third quarter, which preceded the rate spike. In addition, many of the fourth-quarter VLCC bookings were made prior to the rate rise, which reached its apex on Oct. 11.

On Oct. 29, Euronav reported a net loss of $22.9 million for the third quarter of 2019 versus a net loss of $58.7 million in the same period last year. The adjusted net loss per share of $0.17 was in line with analyst consensus expectations for a net loss of $0.16 per share.

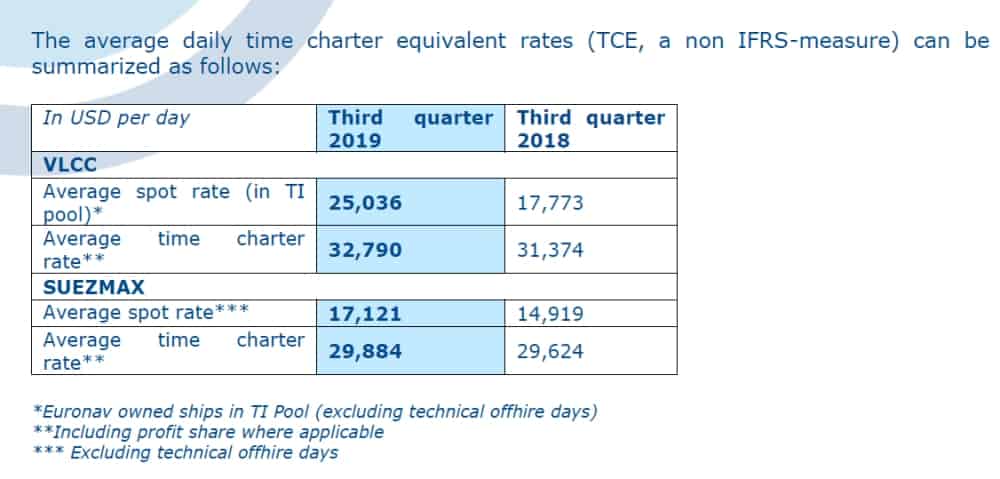

During the third quarter, Euronav’s VLCCs trading in the spot market earned an average of $25,036 per day, up 41% year-on-year. Its Suezmaxes (tankers that can carry 1 million barrels of crude each) in the spot market earned $17,121 per day, up 15% year-on-year.

The company has booked 60% of its available spot VLCC days for the fourth quarter at $60,900 per day and 48% of its available Suezmax spot days at $27,300 per day. More FreightWaves/American Shipper articles by Greg Miller