FreightWaves’ initial coverage of Marten earnings can be found here.

With Marten Transport’s earnings taking the role of first out of the box this quarter, the numbers show a quarter with some strength but one that overall didn’t significantly exceed what happened last year, despite all the talk about how strong the freight market is.

Investors didn’t like what they heard. At approximately 5:30 p.m. EDT, Marten’s stock was down 7.88% from Thursday’s close to $16.60.

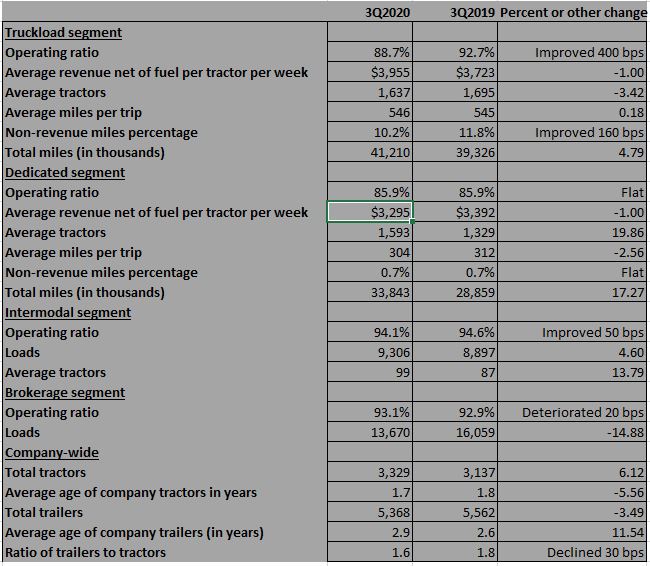

Marten did keep its costs well under control, down about $3.3 million from the third quarter of 2019, and it had better numbers in certain key metrics. The end result was improvement in operating ratio in its operating units. Operating ratio for the truckload segment improved 400 points to 88.7% despite revenue declining from last year. The intermodal segment jumped 50 bps to 94.1%. But brokerage was down 20 bps to 93.1% and the growing dedicated segment at Marten was flat at 85.9%.

Operating revenue for Marten was up only 0.5% from the third quarter of 2019, but that includes lower fuel surcharges. Net of fuel surcharges, operating revenue rose 3.8% from the corresponding quarter of 2019.

Total revenue was up just 0.4%, to $216 million from $214.9 million. That was significantly below consensus forecasts that revenue would hit $223 million, according to SeekingAlpha.

But with improvements in cost control and other efficiencies, operating income was up 21.8%. Net income was $18 million, up 8.8%. At 22 cents per share, it beat consensus by 2 cents, according to Seeking Alpha.

The sluggish increase in revenue was driven in part by a drop in truckload revenue to $93.6 million from $94.9 million. Intermodal revenue declined slightly, to $21.97 million from $22.29 million. Brokerage revenue took an even bigger hit, down to $22 million from $27.3 million in the third quarter of 2019.

The one segment that showed a significant increase was the dedicated group, which has been driving Marten’s growth in recent quarters. Dedicated revenue was $78.3 million, up 11.4% from $70.3 million.

Although truckload’s revenue was down slightly, its operating income climbed 51.6% to $10.5 million, up from $6.95 million.

Although Marten does not break out costs, there are certain corporatewide costs that can be viewed as likely to have contributed to the improvement in truckload operating income. Although companies try to make fuel just a pass-through, that never happens perfectly and fuel can be a benefit or a headwind.

For Marten as a whole, fuel costs were down to $24.3 million from $31.27 million in the third quarter of last year. Purchased transportation, which can be assumed to be more of a cost center for truckload than dedicated, dropped about $3.4 million to $37 million.

The drop in overall operating expenses to $191.6 million from $194.9 million, about $3.3 million, comes in just about the same as the improvement in truckload operating income of a little bit more than $3.5 million.

That is not an apples-to-apples comparison. But with dedicated reporting a flat OR despite an increase in revenue, and truckload reporting a strengthening OR despite a decline in revenue, it signals that costs at the truckload segment were kept well under control.

The truckload segment recorded significant improvements in three metrics. Average revenue per tractor per week rose to $3,955, up from $3,723, an increase of 6.2%. Nonrevenue passenger miles dropped to 10.2% from 11.8%, and total miles rose to 41,210 from 39,326.

The dedicated segment’s improvement came from conducting a lot more business. Revenue rose to $78.3 million from $70.3 million, an increase of 11.3%. Total miles rose to 33,843 from 28,859. Total tractors in the dedicated segment rose to 1,592 from 1,329. But average revenue per tractor per week dropped to $3,295 from $3,392 and the average miles per trip declined slightly to 304 from 312.

One notable number in the earnings: Marten’s cash balance. It is up to $88.2 million, up from $31.4 million at the end of 2019’s third quarter. Put another way, Marten’s cash holdings at the end of the third quarter were 40% of its revenue for the three months. A year ago, that figure was 14.6%.

Marten does not hold an earnings call with analysts. In prepared remarks released with the company’s earnings, Chairman and CEO Randolph Marten focused to a large degree on the company’s nine-month performance, in which several metrics are better than those for the third quarter.

Marten noted that nine-month operating income was the highest in the company’s history and was up 17.3% from the first nine months of 2019. Operating ratios for the nine months also were the best in company history, Marten said in his prepared remarks.

He also hinted at higher pay levels for at least some Marten employees, noting that the company has been “increasing and will continue to increase the compensation for our premium services within the tightening freight market.”

More articles by John Kingston

Marten rides dedicated division to a strong quarter

Marten, Heartland stock prices get boost after strong quarters