Flatbed truckload carrier Daseke pointed to a lack of a seasonal uplift as the basis for lowering its full-year outlook on Tuesday.

The company reported first-quarter adjusted earnings per share of 12 cents before the market opened, which was double the consensus estimate but half the year-ago mark. Following the quarter end, the company repaid $50 million in debt and redeemed $20 million in preferred shares. Those actions are expected to contribute 11 cents in adjusted EPS annually.

Net interest expense was up a little more than $4 million year over year (y/y) in the period even though debt was largely flat. The result was approximately a 7 cent headwind to EPS.

Daseke (NASDAQ: DSKE) reeled in guidance as there is no “clear visibility” into a recovery and as it no longer expects a seasonal lift in freight volumes in the spring-summer time frame. Revenue is forecast to decline 5% y/y during 2023 as rates experience another 1% to 2% decline.

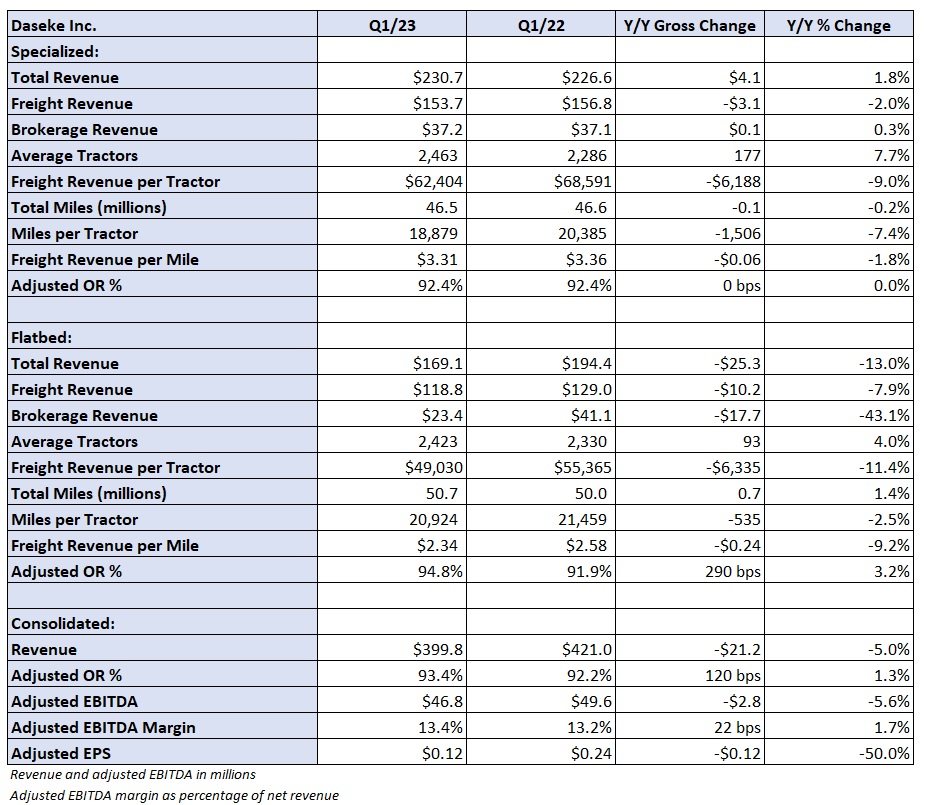

Adjusted earnings before interest, taxes, depreciation and amortization is now forecast in a range of $210 million to $220 million versus the quarter-ago guide of flat y/y at $235 million. Adjusted EBITDA was down 6% y/y in the first quarter to $47 million.

“There’s a lot of data points out there that we’re looking at. … We’re just not really seeing the seasonal uplift,” CEO Jonathan Shepko told analysts on a call.

He said rates normally move 10% to 15% higher from March to April but that isn’t the case this year as the industry is still establishing a bottom for pricing.

Consolidated revenue declined 5% y/y to $400 million. Daseke is using the looser market to move more freight on company-owned equipment, which produces a better margin profile compared to loads moved by owner-operators. Across both of its fleets, loads hauled on company trucks increased 4%.

The company’s specialized unit reported a 2% y/y increase in revenue to $231 million. Average tractors in use increased 8% but freight revenue per tractor was off 9%. Owner-operators made up less than 18% of the fleet in the quarter, which was 360 basis points lower y/y.

Miles per tractor were down 7% y/y as the company saw good demand in the agricultural and energy markets, which was offset by weaker construction and manufacturing activity. Freight revenue per mile declined 2% to $3.31.

The company’s general flatbed unit recorded a 13% y/y decline in revenue to $169 million. Freight revenue was down just 8% but brokerage revenue fell 43% as the company took higher-paying loads from its brokerage business and moved them on company equipment.

Freight revenue per tractor was down 11% y/y as rate per mile fell 9% to $2.34 and miles per tractor declined 2.5%. The percentage of owner-operators was reduced by 480 bps in the quarter.

On a consolidated basis, Daseke posted a 93.4% adjusted operating ratio, 120 bps worse y/y. Salaries, wages and benefits increased 320 bps as a percentage of revenue. Stock-based compensation was a headwind. Purchased transportation was down 460 bps due to the lower brokerage volumes and higher usage of company trucks.

The company has several operational initiatives in place to improve operating income by more than $25 million. The full realized run rate on these process changes and cost programs should be in place by the middle of next year and potentially as high as $30 million by the end of 2024.

Daseke reported liquidity of $196 million following the debt repayment and share redemptions. It generated cash flow from operations of $31 million in the quarter. Total debt of $619 million was 2.7x adjusted EBITDA, down slightly from year end. The company reiterated a long-term leverage target of 1.5x to 2x.

Net capital expenditures guidance for 2023 was lowered by $10 million at each end of the new range of $135 million to $145 million.

Shares of DSKE were off 13% at 1:41 p.m. Tuesday compared to the S&P 500, which was down 0.3%.

More FreightWaves articles by Todd Maiden

- XPO beats Q1 expectations, eyes $50M in labor cost savings

- Yellow posts Q1 loss as it negotiates operational changes, labor deal

- Forward Air dials down 2023 outlook but sees ‘real improvements