Forward Air said it remains focused on the integration of Omni Logistics and the revenue synergies it can achieve as it is now operating a platform that includes freight forwarding and contract logistics along with its legacy expedited less-than-truckload and intermodal offerings.

The Greeneville, Tennessee-based company closed on the merger with Omni in January following a lengthy courtship as the deal was contested by shareholders and Forward itself searched for an exit path.

On its second-quarter call Wednesday, management said it was focused on a “holistic” approach to its service offerings and the way it approaches the market. It vowed to keep its ground LTL network out of the integration, saying it will continue to interact with shippers through third parties (forwarders) and not through direct selling as some of its customers had feared.

Forward’s forwarding customers initially had concerns that the acquisition would cut them out of the equation as Omni is a freight forwarder and their direct competitor. Management said it has begun implementing nondisclosure agreements with its forwarding customers to ensure it doesn’t impose on their shipper relationships.

Forward (NASDAQ: FWRD) reported a headline net loss from continuing operations of $966 million for the 2024 second quarter. However, the number included a $1.1 billion noncash goodwill impairment tied to the acquisition of Omni as those assets no longer garner the premium paid for them. The headline result also included transaction, integration and severance charges.

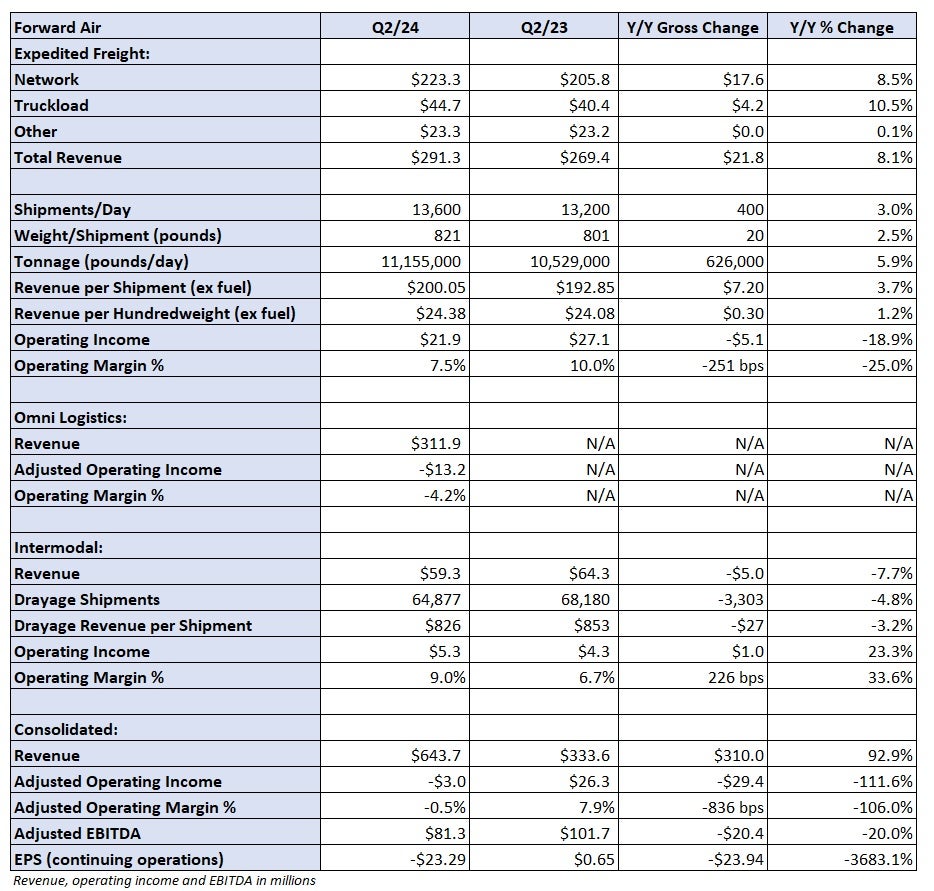

Excluding the items, the company booked an adjusted operating loss of $3 million compared to operating income of $26 million in the year-ago quarter.

“Operationally, we have two very good companies who just got distracted during a fairly tumultuous period of time and 7,000 very hard-working employees that have recently joined forces as one,” Chief Financial Officer Jamie Pierson told analysts on the call.

Adjusted earnings before interest, taxes, depreciation and amortization of $81.3 million was 20% lower year over year but well north of the $29.4 million it recorded in the first quarter. The second quarter included the benefit of an additional $14.6 million in cost savings as well as annualized pro forma adjustments from recent head count reductions, which amplified the benefit.

Forward Air expects to generate $310 million to $325 million in adjusted EBITDA for full-year 2024, which compares to the $325 million in adjusted EBITDA it recorded in the past 12 months. It said it is on track to achieve roughly $75 million in merger-related cost synergies by the first quarter of next year. It has also already realized an incremental $20 million in cost savings from the layoffs.

The company closed the quarter with net debt of $1.7 billion, 5.2 times adjusted EBITDA. The leverage ratio increased from 5 times in the first quarter but remained below the company’s debt covenant of 6 times.

It ended the quarter with $445 million in total liquidity, which included $105 million in cash. Total liquidity declined $67 million from the first quarter, but the company expects to be cash flow-positive at some point in the back half of this year.

The expedited segment, which includes LTL operations, reported revenue of $291 million, an 8% y/y increase as tonnage increased 6% and revenue per hundredweight, or yield, was up 2% (1% higher excluding fuel surcharges). The tonnage increase was the combination of a 3% increase in shipments along with a similar increase in weight per shipment.

The increase in weight per shipment was a drag on the yield calculation. Revenue per shipment was 4% higher y/y excluding fuel.

The expedited unit recorded a 92.5% operating ratio, which was 250 basis points worse y/y. Purchased transportation expense as a percentage of revenue jumped 290 bps y/y.

Omni reported $312 million in revenue, a 39% increase from the first quarter. (Prior-year results were not provided.) Through the first half of 2024, the segment has generated $537 million in revenue, which is well below the $1.6 billion annual top line it had when the merger was first announced.

Management said rumors of customer attrition have been overstated and that both Omni’s pipeline and pipeline conversion rates are increasing. It also said there has been no meaningful attrition within Omni’s sales force.

Shares of FWRD were up 17.8% in after-hours trading on Wednesday.