Forward Air Corp. (NASDAQ: FWRD) reported its third-quarter financial results after markets closed Oct. 24.

The Greeneville, Tennessee-based trucking company reported diluted earnings per share of $0.78 compared to $0.76 in the third quarter of 2018. Top-line revenue grew 9.1% year-over-year to $361.7 million, but net income fell slightly to $22.2 million from $22.3 million a year ago.

Forward Air has a business mix of truckload, expedited less-than-truckload, intermodal and consolidation/warehousing logistics services.

The company offered guidance for the fourth quarter.

“We expect fourth quarter year-on-year revenue growth to be 6% to 10% and net income per diluted share to be between $0.90 and $0.94 in the fourth quarter of 2019,” Chief Financial Officer Michael Morris said in a statement. “This compares to $0.95 in the fourth quarter of 2018, which benefited from a low book tax rate of 20.0%.”

Third-quarter earnings before interest, taxes, depreciation and amortization (EBITDA) grew to $41.2 million, compared to $40.2 million for the third quarter of 2018, and free cash flow grew to $36.3 million from $31.3 million a year ago.

“Our growth strategies drove our record third-quarter results,” said Tom Schmitt, president and chief executive officer. “Consolidated revenues grew 9.1% while consolidated operating income grew 10.1% before considering the net impact of a $2.5 million increased vehicle reserve recorded during the quarter.”

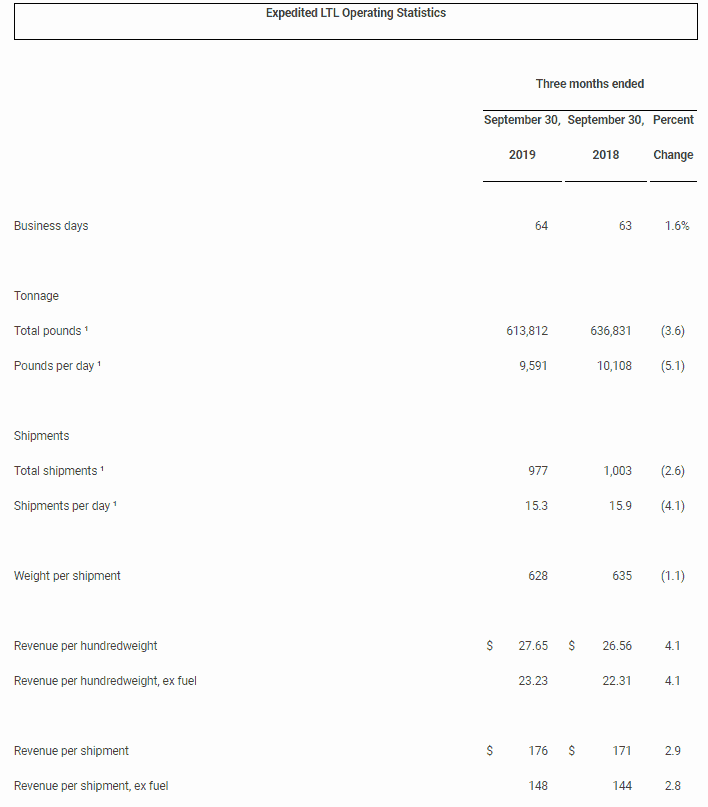

The four business units broken out in Forward Air’s financial reporting are: Expedited LTL (providing expedited regional, inter-regional and national LTL services, including local pickup and delivery, shipment consolidation/deconsolidation, warehousing, final-mile solutions and customs brokerage by utilizing a comprehensive national network of terminals); Intermodal (providing first- and last-mile high-value drayage services to and from seaports and railheads, dedicated contract and container freight station warehouse and handling services); Truckload Premium Services (providing expedited truckload brokerage, dedicated fleet services, as well as high-security and temperature-controlled logistics services); and Pool Distribution (providing high-frequency handling and distribution of time-sensitive products to numerous destinations within a specific geographic region).

Truckload Premium Services was the worst performer, as revenues declined 5.2% year-over-year to $45.4 million, but it’s a relatively small part of the business. Expedited LTL grew revenue 11.4% to $210 million on a year-over-year-basis, Intermodal grew revenue 15.4% to $58.3 million compared to a year ago, and Pool Distribution grew revenue 7.7% year-over-year to $50.9 million.

Part of Truckload Premium Services’ weak performance can be attributed to a larger number of tractors, up 34.4% year-over-year to 391 power units, which drove 13.4% fewer miles per week and took in 6.8% less revenue per mile. That resulted in 20.2% less revenue per tractor per week.

In the Intermodal division, both the total number of drayage shipments and revenue per shipment were up.

Expedited LTL saw fewer shipments, less overall tonnage and lower shipment weights, but higher revenue per hundredweight.