Freight shipments and expenditures dipped further in November, according to data compiled in the Cass Freight Index.

Shipments were down 8.9% year over year (y/y) in the month and off 1.3% from October (up 0.3% on a seasonally adjusted basis). The latest reading puts Cass’ shipments index at its lowest level since January 2022. However, the report said the declines are flattening, with December also likely to produce a 9% y/y decline.

“The acceleration in real disposable incomes, supported by a surprisingly sharp disinflation, and the ongoing strong labor market suggest demand fundamentals will improve in 2024,” said ACT Research’s Tim Denoyer in a Thursday report.

| November 2023 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -8.9% | -9.3% | -1.3% | 0.3% |

| Expenditures | -25.6% | -22.1% | -1.3% | 0.9% |

| TL Linehaul Index | -7.5% | -5.9% | -0.3% | NM |

Expenditures were off 25.6% y/y and down 1.3% from October (up 0.9% seasonally adjusted). The November reading was the lowest since February 2021. However, backing out the change in shipments, actual rates were roughly flat with October (up 0.6% seasonally adjusted).

The expenditures index measures the total amount spent on freight and accounts for changes in fuel surcharges, accessorials and modal mix. After rising 38% in 2021 and 23% in 2022, the index is likely to be off 18% this year. Denoyer said if traditional seasonal patterns hold, the data set will likely be off again by 14% in the first half of 2024.

“We continue to expect modest y/y growth in consumer spending this holiday season, driven by the acceleration in real disposable incomes and the ongoing strong labor market,” Denoyer said. “The recent easing in fuel prices improves our confidence that peak season will end on a higher note.”

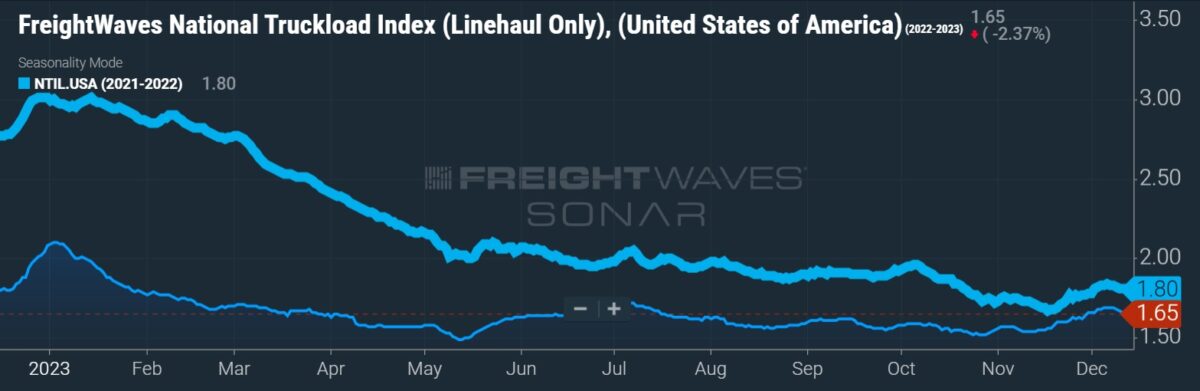

Cass’ truckload linehaul index, which excludes fuel and accessorials, fell to a cycle low, down 0.3% sequentially and 7.5% y/y. The index was at its lowest level since February 2021 during the month, but the y/y declines continued to narrow. Compared to two years ago, the index was down 5.9%.

“With spot rates stabilizing over the past several months, downward pressure on the larger contract market is lessening, with a few instances of contract rate increases bucking the downtrend of late,” Denoyer said.

The TL linehaul index includes both spot and contract freight.

Denoyer noted that recent private fleet expansions have pulled some freight out of the for-hire trucking market, but that overall, softer rates are pushing “net revocations of operating authorities to a record net pace.”

“The surprising strength in the economy in 2023 may provide less support for freight in 2024, but supply contraction should propel the cycle forward in 2024, causing the trajectory of rate trends to change, even if the broad economy slows,” Denoyer concluded.

Data used in the Cass indexes is derived from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $44 billion in freight payables annually on behalf of customers.

More FreightWaves articles by Todd Maiden

- XPO ready to deploy 28 new service centers

- ‘Tremendous outcome,’ judge says in approval of Yellow terminal sales

- Yellow shoots down going concern bid to revive company