Domestic freight demand is not only strong, it is growing stronger.

Yet this statement, supported by data from SONAR, U.S. trade agencies and numerous industry observers, rings false to many carriers operating in the market today.

It might even call to mind the recent brow-beating and haranguing that sought to convince Americans — for whom, in the two years since 2021, the price of groceries had risen 20% — that their economic fears were unjustified, that they were simply trapped in a “vibecession” of their own making.

This article makes no such claims about the state of the trucking industry. Rather, it examines the ways that freight markets might be shaped by the controversial tariff proposals of President-elect Donald Trump, both in the short term and over a longer period of time.

For months now, it has been clear that shippers have frontloaded record imports to the country, largely to avoid expected tariffs. This has spurred the U.S. trade deficit to its highest level since April 2022, flooding markets with a wave of unseasonal freight.

But — if there is so much freight reaching the U.S. — why hasn’t carrier sentiment improved?

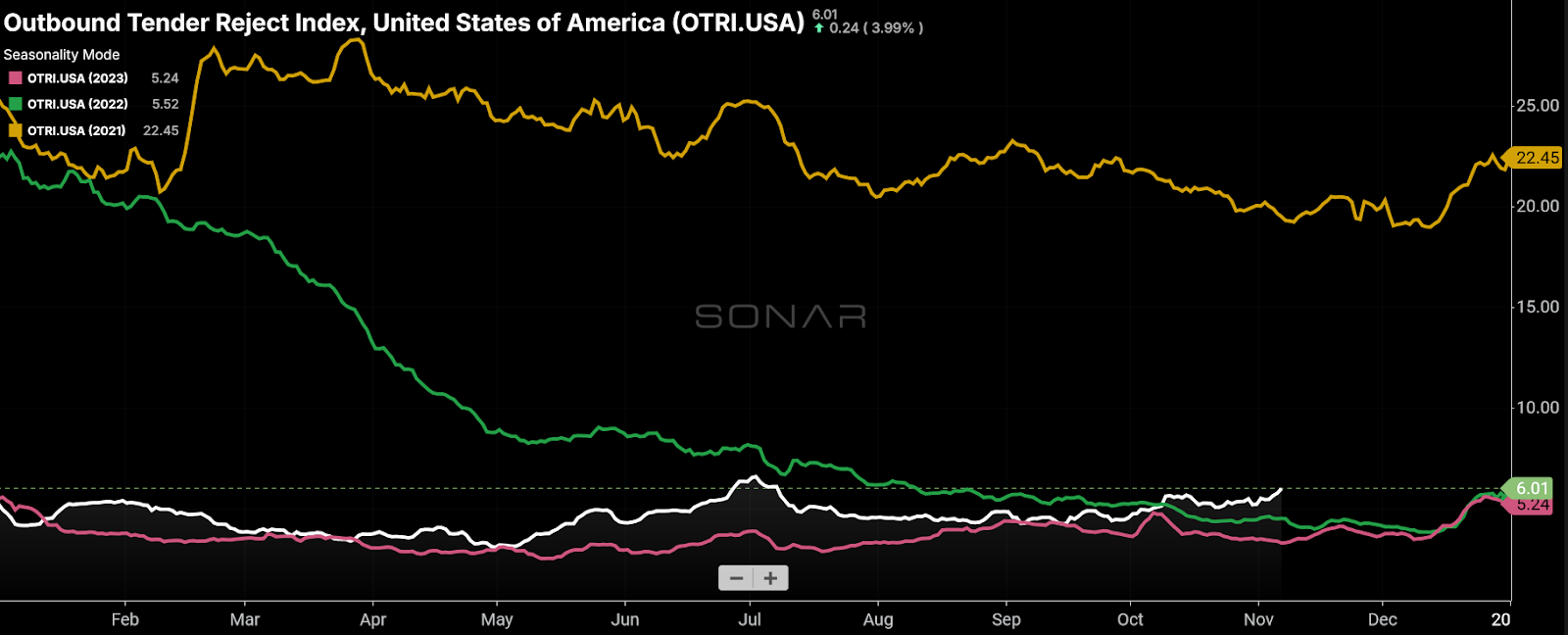

There are two sides to every market: supply and demand. While freight demand is outpacing many of the bearish forecasts from the past few years, its growth is yet unable to satisfy the tremendous glut of capacity that has survived in the market beyond all expectations. This imbalance has depressed carrier rates for more than two years; it is lower rates, not scarce demand, that have spread pessimism throughout the industry.

To learn more about FreightWaves SONAR, click here.

In other words, there’s been a bountiful harvest, but there are still too many mouths to feed. There are good reasons to believe that this excess capacity will not be able to hold out much longer, but such predictions have been frustrated before.

Regardless, it’s not just overcapacity that’s weighing on sentiment in the trucking industry. Compared with the pre-pandemic era of 2017 to 2019 (a period also host to a freight recession), yearly growth in inflation-adjusted consumer spending on goods has fallen from an average of 3.7% to nearly 2% in 2024 thus far. Consumer spending on durable goods — a valuable source of truckload volumes that includes furniture and home appliances — has fared even worse, with yearly growth more than halving from an average of 5.6% to 2.5%.

The rapid and unsustainable growth in consumer spending that did occur in 2020-21, the growth that led to the current overcapacity crisis, was an ill-timed prelude to the surge in inflation set off by Russia’s invasion of Ukraine in 2022. Left with little savings after a historic spending spree, consumers began to rely on credit to cover the rising costs of living. Accordingly, consumers have pulled back on discretionary purchases.

A slowdown in consumer spending was the outcome desired by the Federal Reserve, which raised interest rates at the fastest pace in four decades to combat inflation. A less desired, though still intended, effect was that businesses found it more difficult to borrow money for capital investments.

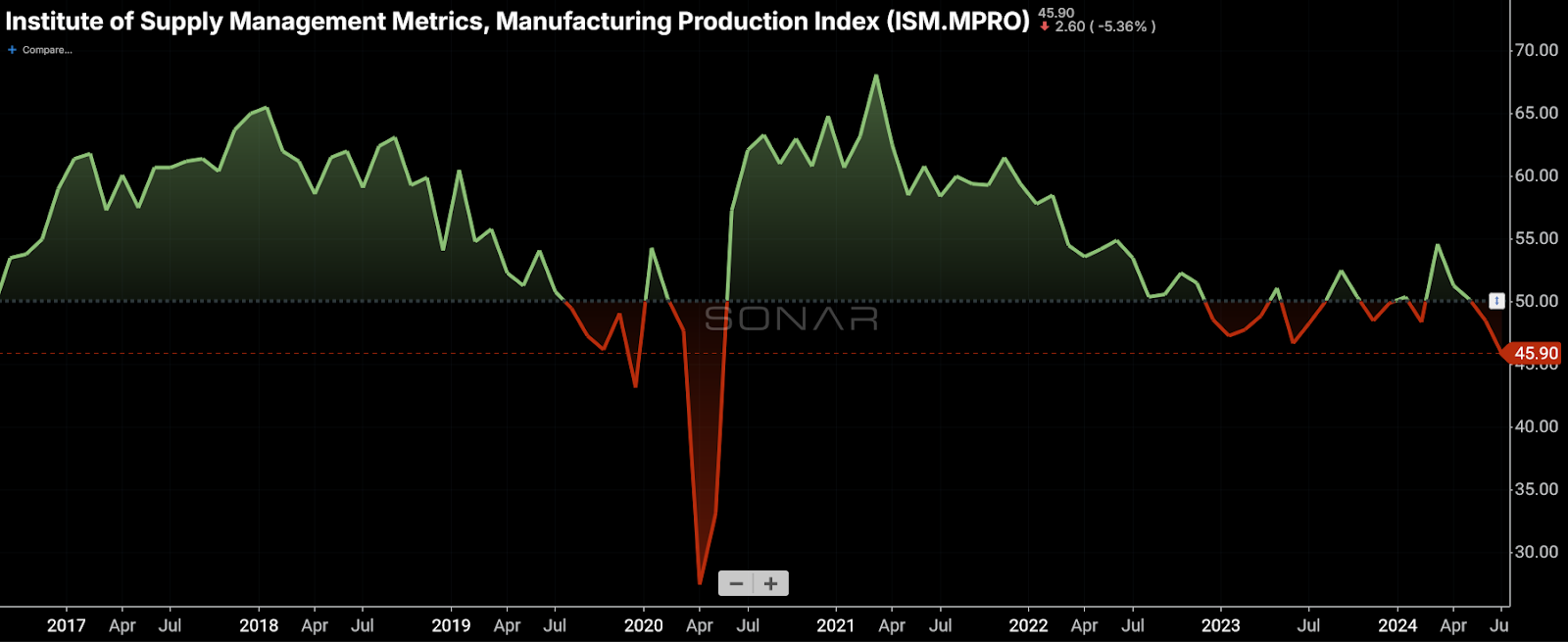

The industrial economy, but particularly the manufacturing and construction sectors, is highly vulnerable to sustained quantitative tightening. The industrial economy also happens to be the largest supplier of freight to trucking markets. Despite the Fed’s cutting rates on Thursday for the second time this cycle, interest rates are still high and manufacturers are still pessimistic, putting out fewer shipments over the road.

Surfing the wave of imports

Yet any softness in manufacturing volumes is more than offset by 2024’s incredible growth in U.S. imports.

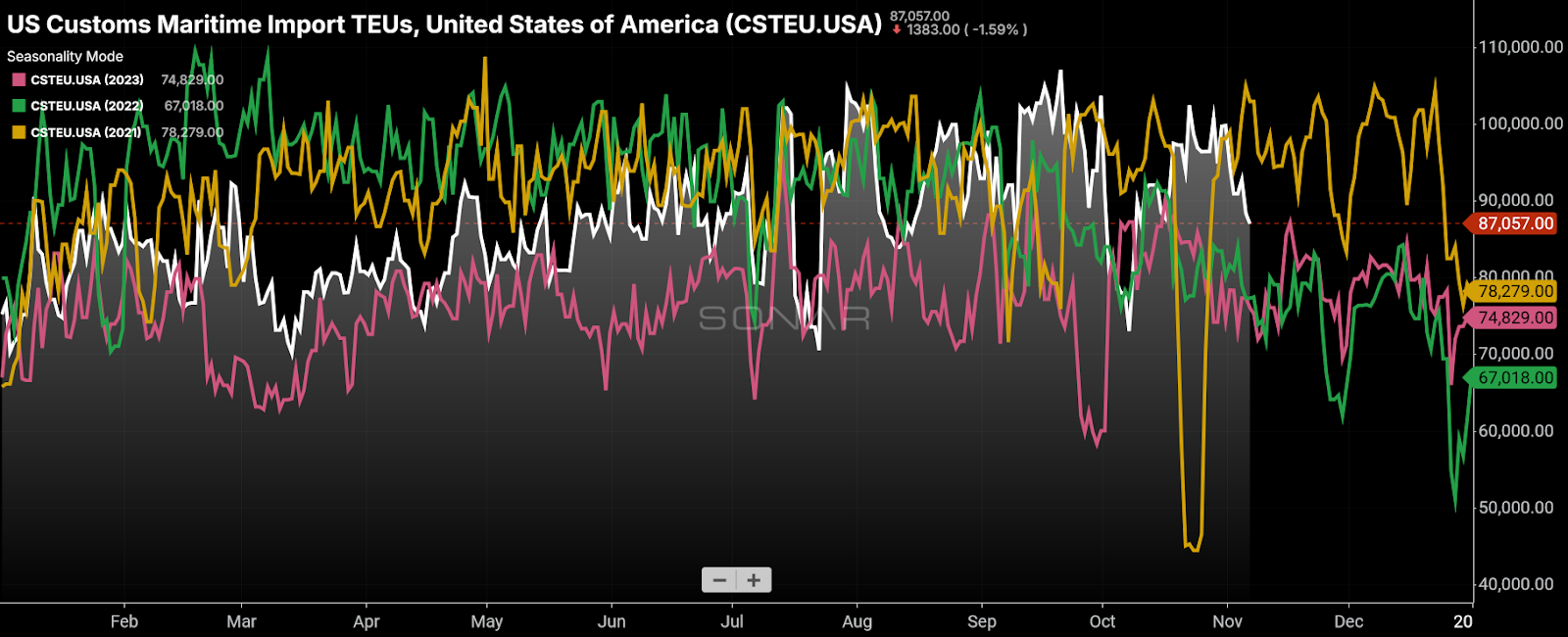

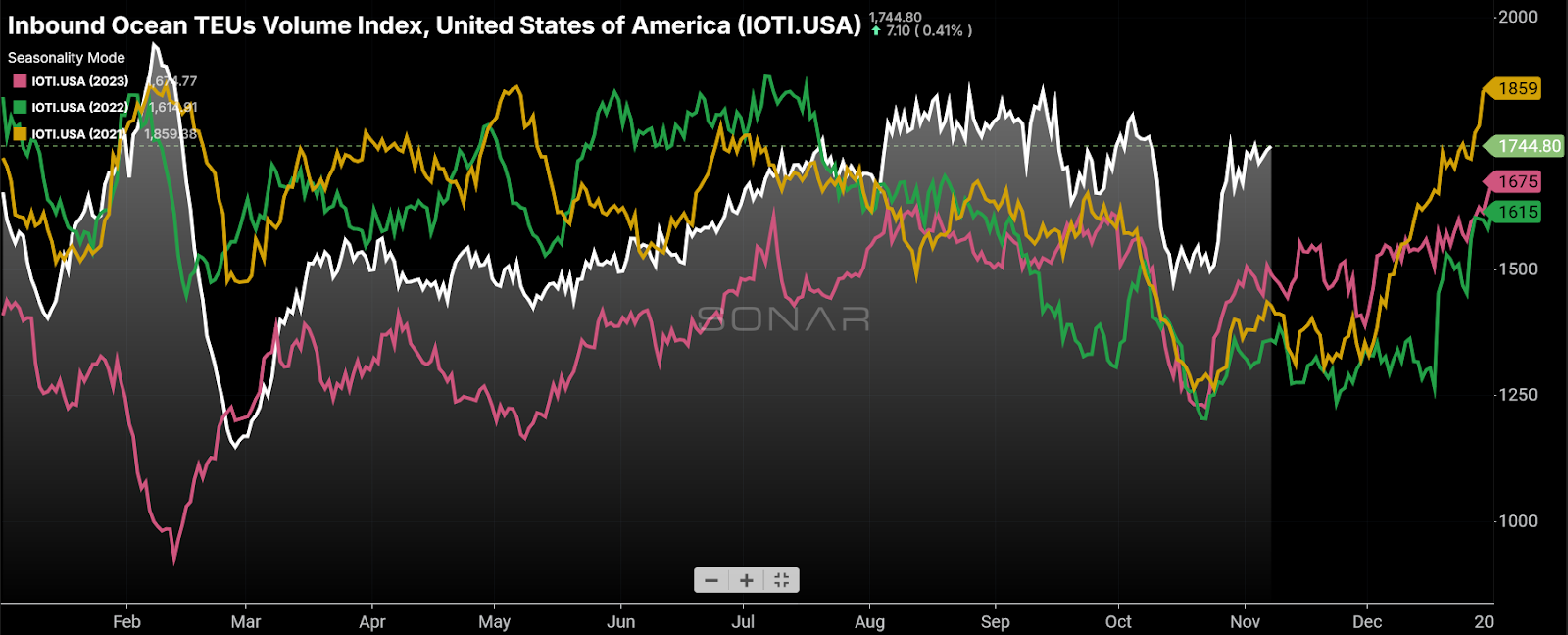

The above chart shows the shipment volumes cleared by U.S. Customs and Border Protection at all ports in the country. What is first apparent is that imports have grown this year over 2023; as 2023 was a relatively weak year for import volumes, this feat is not so impressive.

But, for nearly two weeks in September, the import volumes flowing through U.S. ports outshone the historic growth of 2021 and 2022 — topping out at a level not seen in two-and-a-half years. If one has even the dimmest memory about ocean shipping in 2021, demand for which led to record congestion at ports and container rates that tripled virtually overnight, one realizes how incredible 2024’s growth is.

This growth came at a cost, however: The U.S. trade deficit also widened in September to its highest level in two-and-a-half years.

Although the U.S. trade deficit (particularly with China) is a politically charged issue relative to the broader economy, its growth is an unequivocal good for truckload markets — at least in the short term. A greater deficit implies a high degree of consumer spending on imported goods, which are then moved via the rails and on trucks.

Yet the greatest downside of a large trade deficit comes from the reliance on a foreign power for the domestic supply of freight-intensive goods. Most trade is mutually beneficial, which usually makes this risk a distant concern — unless, say, a trading partner has geopolitical designs contrary to one’s own.

Under the coming Trump administration, volatility in global trade is likely to be a constant. In addition to the tariffs enacted in his first term, many of which have been retained or even amplified by President Joe Biden, Trump campaigned for a 60% tariff on Chinese goods and proposed a 10% blanket tariff on all imports.

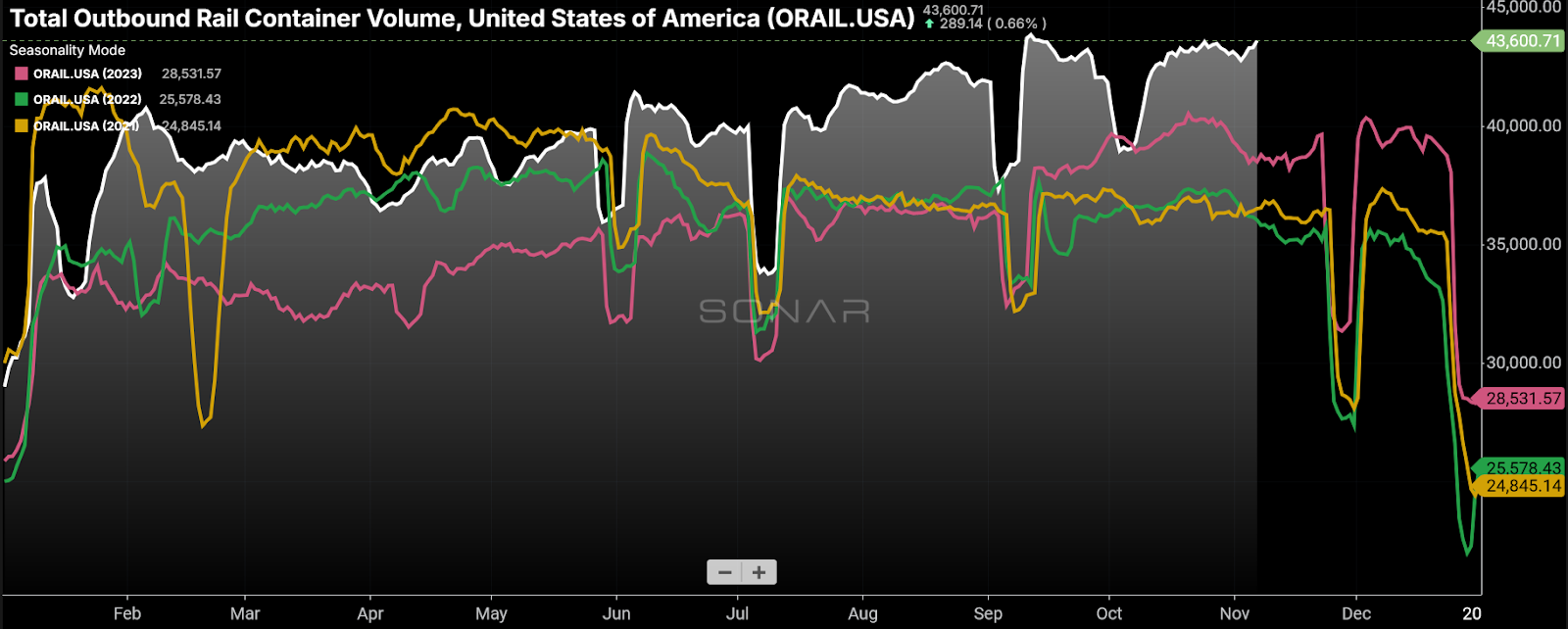

The short-term effects of this stance have been visible for months now. Import bookings, which precede the arrival and processing of shipments by several weeks, have continuously been at their highest levels since 2020. Containerized intermodal volumes have performed similarly since June.

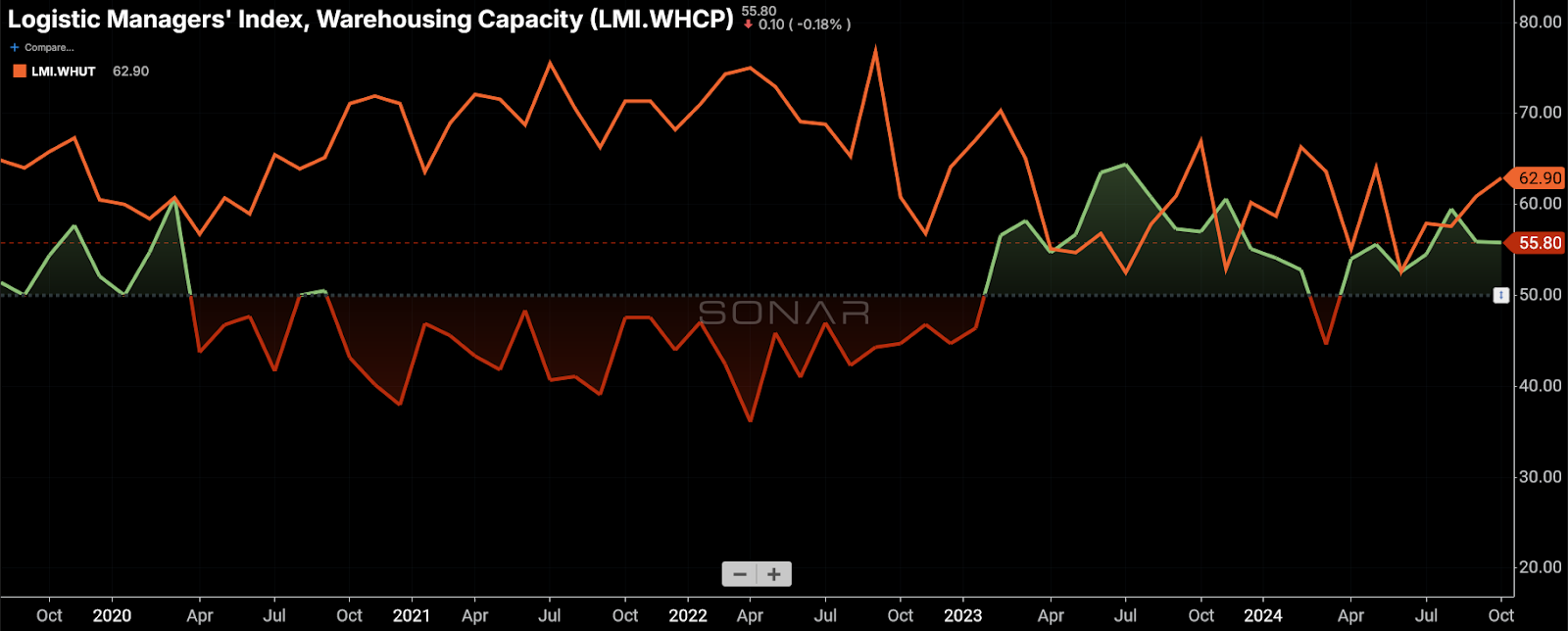

But the rails are not the only ones profiting from this boom: Survey data from the Logistics Managers’ Index (LMI) has seen a divergence in the growth of warehousing capacity and utilization, with the latter rising at a rapid clip since August.

And, not to be forgotten, the actual flow of truckload freight has seen yearly growth almost constantly throughout 2024 so far:

In short, shippers are so concerned about the impact of any potential tariff increases that they have broadly elected to pull forward their freight by months or even years. Yet, as discussed previously, the consumer is currently not in a great position to buy these goods.

So, shippers are stashing their freight at warehouses — hence the rise in utilization relative to capacity — or they are moving it over the rails at a leisurely pace, or they are pushing it inland via trucks. That the trucking industry has been only a modest beneficiary of the surge in imports implies that shippers are largely unconcerned about the speed at which their freight gets to its final destination.

Feast or famine?

While the short-term effects of Trump’s tariff proposals are immediately apparent, the long-term consequences are up for debate.

If this trade policy works as intended, the manufacturing sector will accelerate its ongoing process of reshoring operations. This process has been in motion to some degree since even before the financial crisis of 2008, but the trade war of 2018 and the COVID-19 pandemic were two of the prime catalysts that spurred companies to tighten their supply chains.

One such trend that was exacerbated by the pandemic was an increasing distrust of China as a base of operations. Companies that retained a significant manufacturing presence in China during this period found themselves frustrated by the country’s frequent and abrupt lockdowns, which halted the production and export of goods on an unpredictable basis.

After the sanctions imposed on Russia following its full-scale invasion of Ukraine in 2022, manufacturers are wary of housing operations in countries that could be exposed to international sanctions. The obvious flash points here are Taiwan and the South China Sea, as tensions around both have continued to escalate well into 2024.

But there are factors beyond China’s governance that are facilitating the return of manufacturers to North America. One of the key benefits of moving operations to China used to be its low wages. Yet, according to analysis from Bank of America, hourly wages in China’s manufacturing sector soared 700% from 2006 to 2021.

In Mexico, such wages have risen by only 5%.

To put it bluntly, if a 60% tariff on Chinese goods is introduced in Trump’s second term, it is likely to change only the speed — not the course — of manufacturers’ plans.

Yet critics argue that Trump’s tariff proposals, especially a 10% blanket tariff on all imports, would reignite inflation. In fact, bond yields surged after the Republicans’ sweep, meaning that financial markets fully expect the combination of tax cuts and tariffs to lead to a higher fiscal deficit and greater inflation.

Higher inflation would, in turn, compel the Federal Reserve to withhold future rate cuts — if it does not begin to raise interest rates altogether. Higher interest rates would further depress domestic manufacturing and consumer spending in a one-two blow for the trucking industry.

This scenario is not implausible and might well be likely. Tariffs have not been raised to this degree since World War II. The global economy has changed vastly since that time, leaving little guidance (and much speculation) on how tariffs would function in a far more interdependent world.

But even if these worst fears come to pass, they do not preclude the tariffs from also working as intended. For the trucking industry, domestic freight demand will get a boost in the coming months before the tariffs are implemented. Once they are in effect, demand is likely to slow, being driven primarily by domestically produced goods and imports still lingering in warehouses.

During this soft period, the final pockets of overcapacity will leave the marketplace. Meanwhile, manufacturers will continue to reshore operations as described, a process that is hardly reversible.

Finally, once manufacturers have settled into their bases and are ready to ramp up production, domestic freight markets would see another boom in demand that the industry is underprepared to accommodate — assuming that it sheds, as it usually does, too much capacity in the downturn.

This imbalance of supply and demand would once again drive up carrier rates, attracting more capacity to enter or return to the market, and the cycle would begin anew.