Will 2024 bring a definitive end to the current freight recession?

That’s certainly the hope of the freight market writ large. Many carriers and brokers hobbled through 2023, and those still operating are anxiously awaiting any sign that pricing power is swinging back in their favor.

There are some indications that’s starting but not yet on a widespread or dramatic basis. The first quarter, after all, is historically a difficult one for freight. Adding to that is the fact that the final months of 2023 continued the tumult for the trucking and brokerage sectors, highlighted by a number of bankruptcies in both.

These factors have led to a present environment in which shippers continue to stand out as the vanguard of positivity. The Q1 2024 Freight Sentiment Indexes reveal a surge in shipper confidence, climbing to a record-high 13.58 from 9.79 in the preceding quarter. (Note that data only go back to Q4 2022.)

But this swell in shipper confidence poses a question, too: Will the optimism continue into the market recovery, or could shippers be caught off guard?

It should be mentioned that carriers are experiencing a cautiously optimistic recovery. Their sentiment has modestly ascended to 5.66 from 4.41 in Q4 of 2023. The group is far from out of the woods, however, with excess capacity still hanging over it like a dark cloud.

The mood of brokers, too, is showing signs of improvement in Q1, advancing to 9.96 from 8.78, in spite of the issues with fraud that the Transportation Intermediaries Association (TIA) is working to call attention to on a national level.

These freight sentiment indexes are represented on a scale between negative 100 and positive 100, where higher numbers suggest positive sentiment or growth and lower numbers suggest pessimism or contraction. FreightWaves sends the same survey questions to shippers, brokers and carriers. The results offer aggregated insights from hundreds of respondents into the industry’s health and expectations for the future.

Ultimately, the freight market experienced a lot of recalibrating in 2023. But it does seem to be well positioned to bounce back as 2024 progresses. Demand remained strong last year, even as consumers turned gloomy. Now, with inflation receding and moods lifting, there’s little reason to think that will change for domestic freight, even with tensions rising internationally.

RELATED: Container spot rates rocket even higher as Red Sea crisis drags on

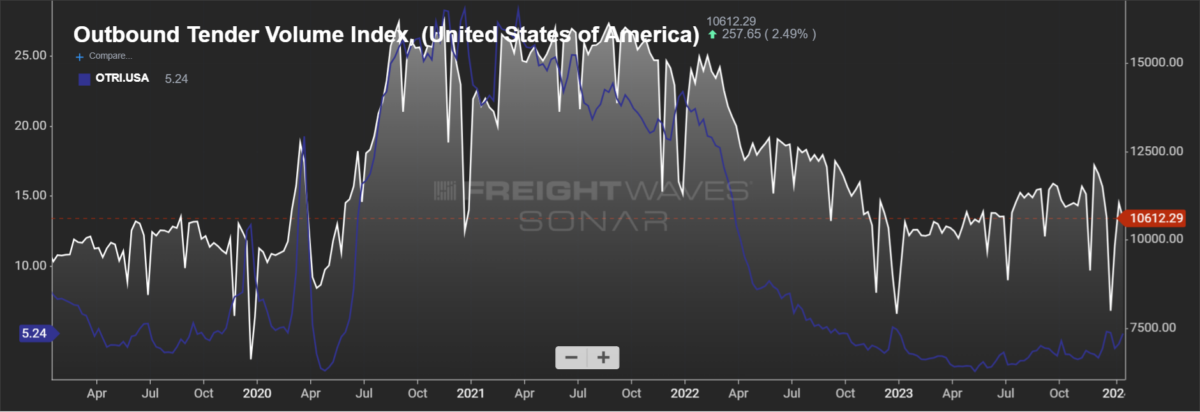

Of course, it’s not all positive. Optimism is tempered by those persistently low tender rejections in the U.S. truckload space. Logic holds that this year will see upward movement on that front, but it’s difficult to predict when exactly capacity will right-size with demand. Furthermore, regulatory shifts impacting owner-operators inject additional unpredictability into the industry’s trajectory.

This quarter’s Freight Sentiment Indexes sketch a portrait of an industry near the turn. Shippers are riding a wave of optimism that — if they’re not careful — could leave some flat-footed when their logistics service providers inevitably start asking for more.

Note: Survey data was fielded during the first two weeks of January.

Carrier sentiment: Gradual recovery as market shift nears

For Q1 2024, carriers exhibited a mixed sentiment. The sector continues to grapple with the excess capacity that has dampened margins for some 18 months now.

The near-term profitability index showed a slight improvement to -1.91 from -3.34 in the previous quarter, indicating a somewhat less pessimistic outlook. This change represents both quarterly and yearly improvement but still suggests carriers expect to be less profitable than in Q4 2023. That’s now been the case for six consecutive quarters, dating back to the first reading in Q4 2022.

Longer-term profitability, however, continued its upward trajectory, reaching 19.23 in Q1 2024 from 16.18 in Q4 2023, and significantly up from 11.16 in Q1 2023. This suggests a growing confidence in future conditions.

The near-term workforce sentiment shifted positively to 0.69 in Q1 2024 from -0.28 in Q4 2023, indicating a modest turnaround in workforce expansion plans, though this figure is lower than the 6.92 recorded in Q1 2023. Longer-term workforce sentiment also improved, moving to 7.88 in Q1 2024 from 6.74 in the previous quarter but again lower than Q1 2023’s 11.73.

Business investment sentiment slightly declined to 2.39 in Q1 2024 from 2.77 in Q4 2023, and that’s also a decrease from 8.69 in Q1 2023, reflecting a cautious approach to investment.

The overall sentiment improved to 5.66 in Q1 2024 from 4.41 in Q4 2023, showing a more optimistic outlook compared to the previous quarter. It is somewhat surprisingly a hair lower than at this time last year.

RELATED: Bankruptcies, fraud and a missing trucker: Key trucking stories in 2023

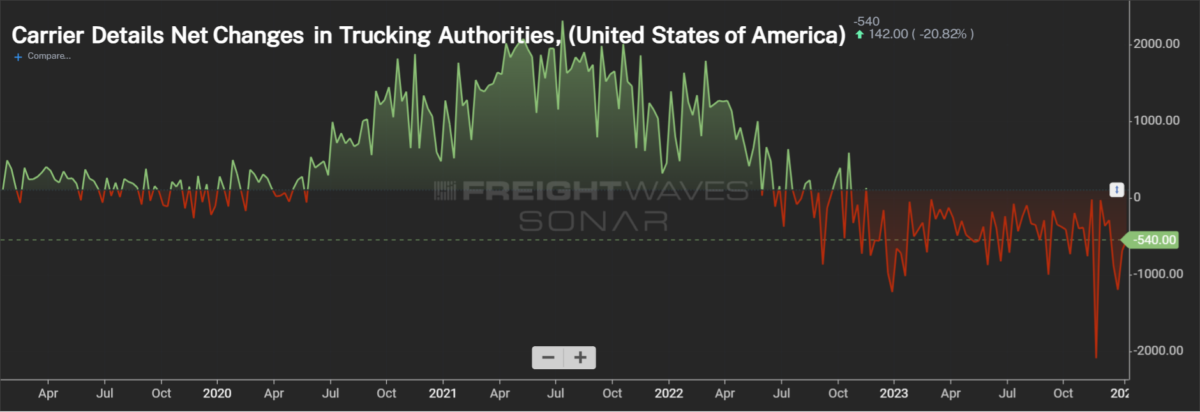

Industry analysts and leaders suggest that 2024 will likely feature a realignment of supply and demand, dependent of course on the continuation of current economic and carrier exit trends.

Broker sentiment: Progress amid pressures

Overall sentiment improved to 9.96 in Q1 2024 from 8.78 in the previous quarter, and it’s also higher than the 6.97 recorded in Q1 2023. It’s a positive sign, though tough times don’t seem to have ended yet.

RELATED: Chicago-based Coyote Logistics cuts sales, operations jobs

Brokers/3PLs showed a decline in near-term profitability, however, dropping to -2.01 from -1.03 in the previous quarter. While this represents a deterioration on a quarter-over-quarter (q/q) basis, the sector improved from -4.92 in Q1 2023. Longer-term profitability sentiment, meanwhile, increased to 28.49, up from 21.95 in Q4 2023 and significantly higher than 11.5 in Q1 2023, indicating a robust long-term outlook.

Near-term workforce sentiment showed a slight improvement to 0.45 in Q1 2024 from -1.17 in Q4 2023, but it is lower than 1.6 in Q1 2023. Longer-term workforce sentiment remained stable at 14.01, slightly down from 14.08 in the previous quarter but up from 11.88 in Q1 2023.

Business investment sentiment declined to 8.85 in Q1 2024 from 10.09 in Q4 2023, and down from 14.77 in Q1 2023, indicating a more cautious investment approach.

Confronting the escalating issue of fraud has become a paramount concern for the brokerage sector. TIA’s alert to Congress and the initiation of a quarterly white paper dedicated to fraud analysis highlight the trade group’s interest in addressing these risks head-on.

Shipper sentiment: Optimism that could come back to haunt

Shipper sentiment remains rosy. The sector’s overall metric improved to its highest level yet measured — 13.58 from 9.79 q/q, and from 10.64 in Q1 2023.

The sector exhibited an increase in near-term profitability sentiment to 11.92 in Q1 2024 from 9.8 in Q4 2023, and higher than 5.39 in Q1 2023, indicating a positive short-term outlook. Longer-term profitability sentiment also improved to 23.01 from 21.2 in Q4 2023 and from 22.17 in Q1 2023, showing continued confidence in future profitability.

Near-term workforce sentiment rose significantly to 4.86 in Q1 2024 from 0.53 in Q4 2023, and higher than 3.31 in Q1 2023, reflecting an optimistic approach toward workforce expansion. Longer-term workforce sentiment improved to 8.91 from 5.97 in the previous quarter, and up from 6.28 in Q1 2023. These glimmers of positivity likely have to do with macro data like improving consumer sentiment and the seemingly certain prospect of a soft landing for the U.S. economy.

Business investment sentiment likewise jumped to 19.2 in Q1 2024 from 11.47 in Q4 2023, and also up from 16.04 in Q1 2023, indicating a robust investment outlook. These readings are all very positive for freight demand in 2024.

Alternatively, this heightened optimism could have its pitfalls for shippers. The broader economic landscape remains fraught with uncertainties, and the shippers’ elevated confidence could lead to miscalculations or overextensions in a market still harboring volatility. And this year might be the last time shippers have the advantage in pricing power until 2026 or 2027, depending on how long the next cycle lasts.

Overall, Q1 2024 showed improvement in sentiment across most metrics for carriers, brokers/3PLs and shippers, with particular strength noted in the longer-term profitability and business investment segments.

This optimism is promising, but it could usher in its own set of challenges in an ever-shifting market. Right now, prudent shippers are fostering strong relationships with carrier partners and preparing their networks for a time likely not far away when they’ll be at the whim of provider demands.

Those that aren’t so proactive could soon find themselves left out in the cold.