A weekly look at what occurred in the oil markets of the U.S. and the world this past week and what’s ahead.

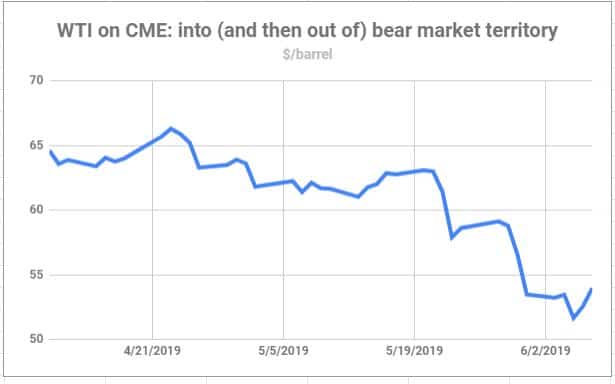

The first half of the year is not complete and already we’ve had both a bull market and a bear market in crude oil.

That we had a bull market wasn’t that surprising or a big deal at the time. With West Texas Intermediate (WTI) having dropped close to $42/barrel on Christmas Eve, it was only going to take about an $8 to $9 increase to meet the definition of a bull market, which is a 20 percent increase in the price of an asset.

The bear market… that was a bit more surprising. When WTI settled April 23 at $66.30/barrel, and Brent was up around $74.50 at that time, the rumblings of a $100 Brent barrel began anew. The rise to that level in April was fueled by a now familiar litany of reasons – OPEC cuts that exceeded the group’s targets, the U.S. ending waivers on its Iranian sanctions that had allowed several countries to keep buying Iranian crude, the collapsing output from Venezuela and fears of a collapse in Libya as well (which so far has not come).

But since the high water mark of late April, it’s been all downhill. When WTI moved below $53.70 this past week, it was 20 percent less than its recent high and a bear market was declared. That 20 percent decline has not been seen in the Brent market or any of the products markets.

But coming so soon after the post-Christmas run, and with the $100/barrel talk starting to stir, the speed of its decline was a shocker.

If there’s been one overriding reason, it’s been the unrelenting growth of supplies in the U.S., not so much coming out of the ground – though that amount continues to rise – but what’s held in inventories.

The OPEC cutbacks were supposed to flatten those inventories. And in one sense, the OPEC cuts have worked. From levels in October and November of last year near 33 million barrels per day (b/d), OPEC production fell to 30.26 million b/d in April, according to S&P Global Platts (though that number is artificially low compared to last fall because Qatar pulled out of OPEC at the end of last year with its 600,000 b/d production). Taking an October/November output level of 32.4 million b/d (after taking Qatar out of the mix), it still means OPEC reduced its output by more than 2 million b/d, far more than 800,000 b/d it planned to do so when it reached its most recent deal in December 2018.

And yet… the price has been falling. Global inventory numbers do not have a release of regular weekly numbers the way the U.S. Energy Information Administration (EIA) releases inventory figures, so those EIA numbers get a tremendous amount of interest. They’re viewed as something of a proxy for the entire world.

And they’ve got one direction – up. Total inventories of all types of petroleum, in the latest weekly report, were at levels not seen since the fall of 2017. Total distillate inventories, which include diesel, were at their highest mark since the beginning of the year after a sharp increase in the most recent report of more than 4.5 million barrels. U.S. crude inventories (not counting those in the Strategic Petroleum Reserve) are almost 40 million barrels more than at the start of the year.

But while everyone might be looking at the U.S., the most recent report of the International Energy Agency said that in March – the most recent month for which it has an inventory estimate – crude stocks fell globally during a period when they normally build, and product inventories fell globally as well.

The Brent crude oil market, considered the world’s benchmark, is in the commodities version of an inverted yield curve. But an inverted yield curve in interest rates is often a harbinger of a recession. In a commodity market, the inverted yield curve is known as a backwardation, with prices further out the curve priced less than the spot price. It’s the sign of a tight market. While it may seem counterintuitive that a tight market would have higher further-out prices than current levels, the fact is the most available barrel becomes the most valuable and a backwardation ensues.

But it’s clear that it’s the U.S. inventory numbers that are having a bigger impact on OPEC thinking than the shape of the Brent curve. At an industry meeting several weeks ago, Saudi oil minister Falih was quoted as saying, “(A)ll indications are that inventories are still rising. We saw the data from the U.S. week after week, and they are massive increases, so there is obviously supply abundance.”

The end result of all this is that the upcoming OPEC meeting is heading into controversy. But the controversy isn’t over what to do at it. It’s about when to have it. Some countries want it at the end of this month. Other countries want it in early July.

What doesn’t seem to be controversial is what the group will do when it meets, whenever that turns out to be. “I don’t think I’d be giving away a secret if I said that on the OPEC side, the rollover is almost in the bag,” Falih was reported by Platts to have said at a recent conference in Russia. “The question is to calibrate with non-OPEC if there needs to be an adjustment.”

Russia has been mixed on whether it would extend its cooperative agreement with OPEC. But it contributed in a backhanded way to the effort to reduce supplies by sending contaminated oil down the Druzbha pipeline, a calamity that has reduced its output by several hundred thousand barrels per day and raises questions about when full exports might be implemented. (The pipeline has resumed operations.)

The market ended the week on a higher note but for reasons that didn’t seem at all oil-related. Instead, it rose higher on the back of a stronger dollar and the increase in equity markets whose own increases have a variety of factors behind them.

Inventories are pushing the market one way; the Brent curve is pushing another. The WTI bear market shows that inventories most recently have won. That’s been good news for the trucking sector.