GDP growth slipped in the second quarter, and revisions reveal weaker 2018 growth

Growth in the U.S. economy slowed during the second quarter, as accelerating consumer spending could not offset a reversal in the inventory cycle and weaker business investment. In addition, annual data revisions revealed stronger growth in 2017, but weaker performance last year.

The Bureau of Economic Analysis (BEA) released results for second quarter gross domestic product (GDP), showing that overall growth in the economy slowed to a 2.1 percent annualized pace. This is down from the 3.1 percent pace of growth in the first quarter of 2019, but slightly exceeds consensus estimates of 1.9 percent growth. Year-over-year growth for the second quarter slipped to 2.3 percent, down from 2.7 percent in the first quarter.

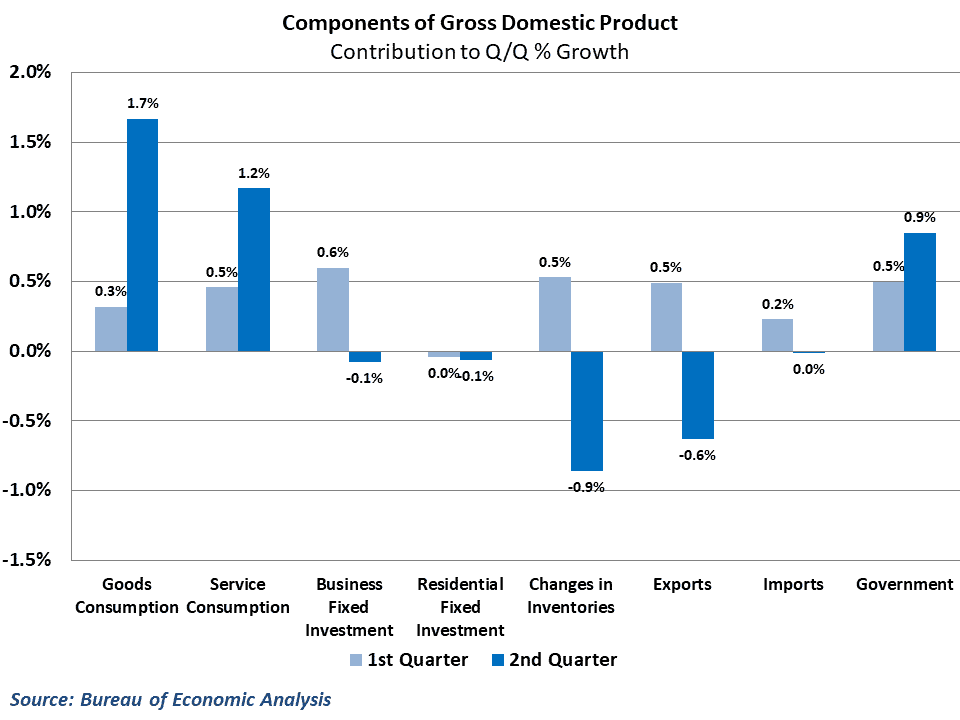

Consumer spending, which makes up approximately 70 percent of GDP, was the lone source of strength in the private economy, contributing a whopping 2.9 percent towards overall growth during the quarter. Government spending also made a sizeable contribution to economic growth, adding an additional 0.9 percent to the quarterly GDP results.

Other areas of the economy exhibited considerable weakness in the second quarter, signaling unbalanced growth in the overall economy. Business fixed investment declined during the quarter, led by a drop in spending on structures. Residential investment, which measures housing construction, fell for the sixth straight quarter and remains one of the consistently weak areas in the economy. International trade also weighed heavily on growth during the quarter, as a decline in exports essentially erased the positive contribution in first quarter results. Lastly, inventories declined outright in the second quarter after three straight quarters of an accelerating buildup. This reversal in the inventory cycle subtracted nearly a full percentage point from growth during the quarter.

Growth in the freight economy reaches 2016 pace

In any discussion of GDP, it is important to remember that there are a number of reasons why GDP is not the best metric for gauging the strength of the freight economy. GDP is comprised mostly of services and excludes goods that are imported into the country, and as a result it emphasizes areas that are less important for freight while ignoring activity that is important for the movement of goods throughout the economy.

A better metric to track is private final goods demand, which looks at all of the spending on goods in the private economy. From this perspective, the details in the GDP release also show an unbalanced goods economy. Real consumer spending on goods drove nearly all of the growth in goods demand in the second quarter, growing at the fastest pace in this current expansion. This was enough to offset weakness in business goods investment and declining trade volume during the quarter to keep growth in the goods sector positive overall.

Still, it is clear that the goods economy has slowed significantly in recent quarters. Year-over-year growth in goods demand, which topped 5 percent in the middle of last year, has since fallen all the way to 1.4 percent in the second quarter. For perspective, this pace of growth is similar to the pace seen in 2015-2016, which was another weak period for freight demand in the economy.

Annual revision shows weaker 2018 growth

Along with the initial estimate of second quarter GDP, the BEA also released its annual revisions to GDP history. Each year, the BEA uses results from various quarterly and annual surveys, as well as updated tax and farm statistics to revise a longer period of history for its GDP figures. This year’s revision covers the five years from 2014-2018. While first quarter GDP results were unaffected by the revision, the annual revision resulted in a significantly slower pace of growth for 2018, particularly in the fourth quarter. As a result, year-over-year growth in the economy ended last year more than half a percentage point lower than previously thought, while 2017 growth was revised upward. This suggests that the boost that the economy received from tax cuts last year was smaller than previously thought, though current momentum looks to be about the same.

Behind the numbers

The second quarter GDP results did not contain many surprises. The rebound in consumer spending was primarily driven by spending on goods, which has been evident in the retail resurgence over the past few months. Keep in mind though, that online sales figures have been particularly impressive this year, and traditional retail outlets are still experiencing mixed results.

The bigger surprise came from the annual revision. The general narrative for the economy overall hinged around the back-to-back impressive quarters in the middle of last year which put the economy in the strongest position it had been in years by the end of the year. Post-revision, the economy sputtered to end 2018, finishing the year at 2.5 percent GDP growth year-over-year. This does little to alter the outlook the quarterly figures going forward, though year-over-year growth looks like it will be around 2.4 percent by the end of this year.

Going forward, consumer spending will likely still be solid, though growth probably won’t be as fast as it was in the second quarter. There is still a bit of an overhang evident in inventory/sales ratios, so drawdowns are likely to continue, and trade volumes are not expected to rebound in any meaningful way given sluggish global growth conditions and continue trade policy uncertainty.

However, some of the recent data coming from durable goods orders suggests that business investment may pick up some. Growth is likely to remain in the 2-2.25 percent range in the third quarter, but could be more balanced if business spending returns.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.