Supply chain improvement, leading to better on-shelf availability, drove positive variance relative to management’s prior guidance. Shares of General Mills rose 2.5% on Wednesday in a down market. The increase to the company’s full-year earnings guidance (earnings were previously expected to be 2% lower to 1% higher y/y and are now expected to be flat to 2% higher than last fiscal year) surprised the market since it came just one month after the Consumer Analyst Group of New York conference. There, management discussed constraints related to on-shelf availability of dough, pizza and hot snacks, which resulted in a more modest outlook than was described on Wednesday.

In the past month, on-shelf availability of those product categories improved from a nadir of 75% early in the company’s fiscal Q3 (December-February) before rebounding to 85%. However, the company does not expect service levels in those categories to get fully back to historic levels in the near term. For comparison, the on-shelf availability of the company’s other products has remained in the 95% range. What changed in the past month was a bigger push by General Mills to find the necessary ingredients to keep its manufacturing facilities running. Plus, General Mills made adjustments to freight lanes to get products to retailers on time.

Here are a few other takeaways from General Mills’ results, which I believe are also relevant for other CPGs:

Unsurprisingly, General Mills’ cost inflation and pricing will continue to trend higher in the upcoming quarters. The company’s input cost inflation is running in the 8%-9% range for its fiscal 2022. Meanwhile, the company’s prices were 7% higher in its fiscal Q3, on average, with a greater price increase forthcoming in the Q4. Input costs rising faster than prices led to General Mills’ adjusted margin contraction of 160 basis points in the most recent quarter. Most CPGs have experienced margin pressure in the past year, with packaged meat companies being a notable exception.

General Mills hedged about 50% of its costs for fiscal 2023 (May 2022-April 2023) and is pulling other levers to maintain profitability amid intense cost pressure. General Mills is working to secure alternative supply sources and boost inventory levels for certain raw materials in an effort to control costs. In addition to increasing list prices, General Mills is changing packaging sizes to charge more per ounce. General Mills has reduced SG&A expenses, which management describes as being primarily driven by lower administrative costs with only a slight reduction to its marketing budget. A number of other CPGs have cut their marketing budgets rather heavily during the pandemic, especially for products that had low on-shelf availability, as a way to mitigate stockouts.

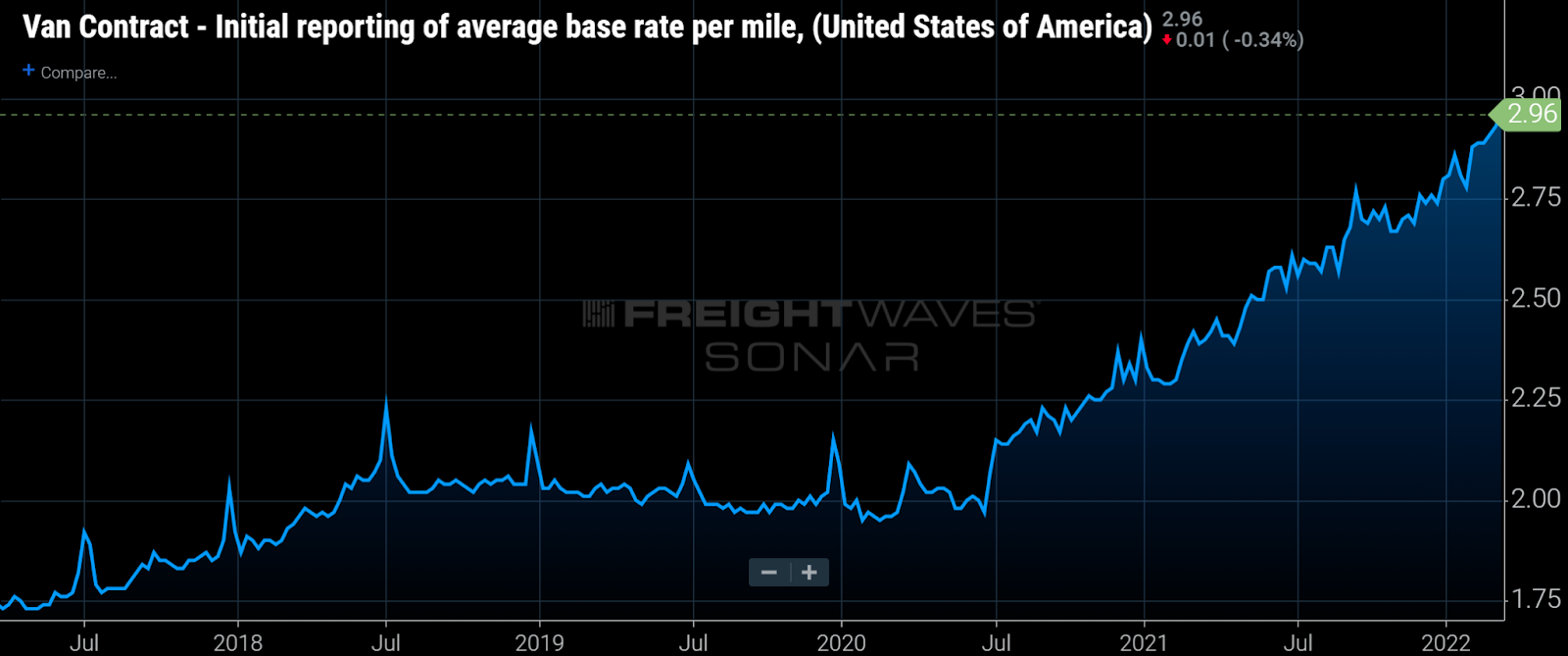

Average dry van freight rates, not including fuel, have increased steadily since mid-2020.

Chart: SONAR

So far, elasticity is in line with historical levels. General Mills’ management describes elasticity as “benign” and no worse than historical levels despite inflation persisting at a 40-year high. However, the company is seeing at least some degree of elasticity in consumer demand across the board and says pet food is less elastic than most categories. General Mills calls “the humanization of pet food” the dominant trend in pet food, which causes consumers to be less sensitive to rising prices. Remarkably, organic price/mix increased 13% in the pet food category, easily outpacing the 7% price/mix growth for the company as a whole. Other CPGs have called out coffee (which Nestle is no longer selling in Russia) as having a below-average degree of elasticity, particularly brands that serve the mass market, such as J.M. Smucker’s Folgers brand.

General Mills will be spending capital to expand its manufacturing capacity in the coming year. One of the major CPG trends during the pandemic has been the greater use of outsourced contract manufacturing, which has the benefit of creating volume flexibility during periods of uncertain demand. The downsides of contract manufacturing are that it is more expensive, the CPG has less control of production costs, and supply chain complexity and working capital requirements increase as more inventory is required in more places. Now, following a surge in contract manufacturing rates and a growing expectation that CPG demand will remain at pre-pandemic levels, I expect to see CPGs bring more of their production in-house.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.