The rise of East Coast ports has been largely credited to the fall of West Coast ports — to shippers switching routes following the expiration of the West Coast port labor contract in July. But that’s only part of the story.

Double-digit growth in imports from Europe has been another big driver of East Coast strength.

Even after recent declines, Europe-East Coast spot rates remain almost triple pre-pandemic levels and more than triple rates in the Asia-West Coast market.

Indexes falling but still very high

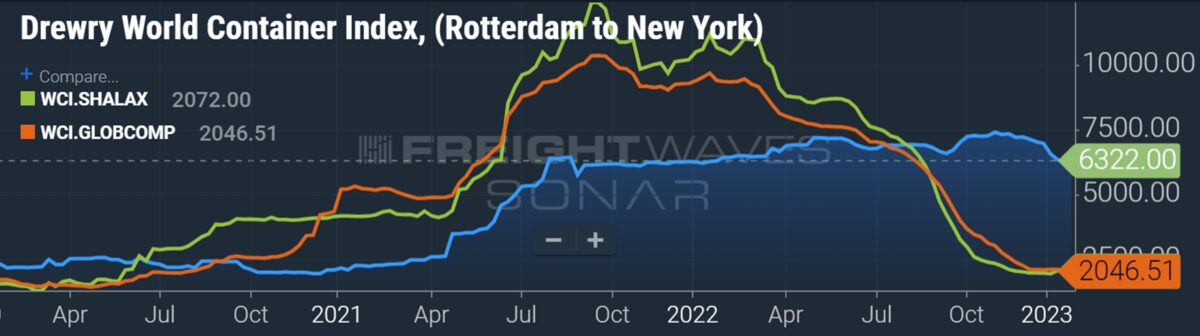

Different spot rate indexes provide different numbers but generally show the same trend. The Drewry World Container Index (WCI) put Rotterdam-New York spot rates at $6,322 per forty-foot equivalent unit in the week ending Thursday, unchanged from the week before. In contrast, Drewry’s Shanghai-Los Angeles Index and its global composite are just above $2,000 per FEU, close to pre-pandemic levels.

While the WCI Rotterdam-New York index has fallen 15% from its all-time high in November, it’s still 2.6 times higher than it was in January 2020.

The Freightos Baltic Daily Index assessed Europe-East Coast spot rates at $5,210 per FEU on Friday, relatively unchanged since the beginning of this year.

This is down 27% from November, but still 2.9 times January 2020 levels.

Xeneta tracks both contract rates and spot rates. Its short-term index put North Europe-U.S. East Coast rates at $6,086 per FEU as of Wednesday. Long-term rates for this trade were under $6,000 per FEU as of mid-January.

Spot rates have fallen below contract rates in almost all of the world’s container trades — but not yet in the trans-Atlantic westbound lane. In markets where spot rates have sunk well below contract prices, carriers have agreed to lower some of their long-term rates in mid-contract, further reducing revenues. That renegotiation dynamic does not apply in the trans-Atlantic.

Europe-U.S. rates remain “historically strong,” said Xeneta Chief Analyst Peter Sand earlier this month, adding that both short-term and contract rates in January 2021 “were roughly a third of today’s prices.”

Carriers shift more ships to the Atlantic

Rate strength continues to attract more ships to the trade, which are being shifted in from less profitable markets like the trans-Pacific. The new capacity is “now undermining the high rates that attracted the vessels in the first place,” noted Sand.

Sea-Intelligence said last month that trans-Pacific westbound capacity will increase 20%-30% in the first quarter.

Alphaliner has reported numerous service additions: Cosco, OOCL and ONE doubled the sailing frequency of their East Med-East Coast “EMA” service. THE Alliance and Ocean Alliance reinstated calls in New York and Savannah, Georgia, for their joint Med-East Coast “AL6” loop. Ellerman City Liners launched a new North Europe-East Coast service. Evergreen upsized its ships in the trans-Atlantic market. The 2M alliance between Maersk and MSC added three ships to its coverage.

Meanwhile, East Coast port congestion has largely cleared, releasing even more vessel capacity into the market.

Platts, a division of S&P Global, believes these additions are having an increasingly negative effect on spot rates. Unlike the Drewry and Freightos indexes, which were steady last week, Platts’ trans-Atlantic assessment plunged. Its Europe-East Coast index fell $800 per FEU, to $5,000 per FEU, down 14% from the week before.

Sources told Platts that the sudden drop was due to capacity additions and that they expect rates to keep falling.

Imports from Europe exceptionally strong in 2022

Customs data compiled by the U.S. Census Bureau shows that containerized imports from Europe are dominated by building supplies, wine and other beverages, furniture, automotive parts, paper products, and food.

According to the latest data, containerized imports from Europe in January-November were up 2% year on year and up 13% versus the same period in 2019, pre-COVID.

While imports from Europe fell in November versus October, they were still 21% higher than volumes in November 2019.

One volume driver last year was the strength of the dollar versus the euro. This currency advantage has been reversing over the past three months.

Maritime Strategies International (MSI) said in a report on Friday: “There has been a brightening of investor sentiment toward the European economy, which could result in an influx of money into Eurozone financial assets, strengthening the euro against the dollar. This could further weigh on U.S. imports from the region.”

As a result of the currency factor, reduced U.S. consumer demand and the unwinding of congestion at East Coast ports, MSI expects trans-Atlantic rates “to drop further in the coming months.”

Click for more articles by Greg Miller

Related articles:

- How will Maersk-MSC split redraw container shipping landscape?

- Top 10 container lines: How did rankings change during boom?

- Container shipping’s ‘big unwind’: Spot rates near pre-COVID levels

- Coast is (almost) clear as port congestion fades even further

- East Coast container imports still far above pre-pandemic levels

- Trans-Pacific rates still sinking. Trans-Atlantic rates still peaking