Chart of the Week: Drewery World Container Index – Shanghai to Los Angeles, TAC Air Cargo Rate Index – Hong Kong to North America, Truckstop.com All-in Van Rate per mile – USA, Intermodal Spot Rate – USA SONAR: WCI.SHALAX, AIRUSD.HKGNOA, TSTOPVRPM.USA, INTRM.USA

Transportation costs have skyrocketed across all modes over the past year and a half, leaving many who operate largely outside of the space baffled as to why the situation has not improved. To understand why supply chains are still broken, you need to understand what broke them.

Looking across the four main modes of transportation’s spot rates for ship, air, truck and train, their charts look like an echocardiogram of four people that got hit with a defibrillator after being in a coma.

Obviously, the pandemic is at the root of the cause, but COVID-19 was really just an accelerant that was placed on a smoldering ember. In other words, supply chains were headed in this direction, to some extent, regardless of the pandemic.

Bracing for recession

Looking back into 2019, spot rates were basically flatlining as the freight market was experiencing a cycle of oversupply and stagnant demand. A robust 2017-18 thanks to an overstimulated economy spurred rapid investment and growth only to be followed by a hangover event, which led to the beginning of economic contraction. Many feared a recession was imminent.

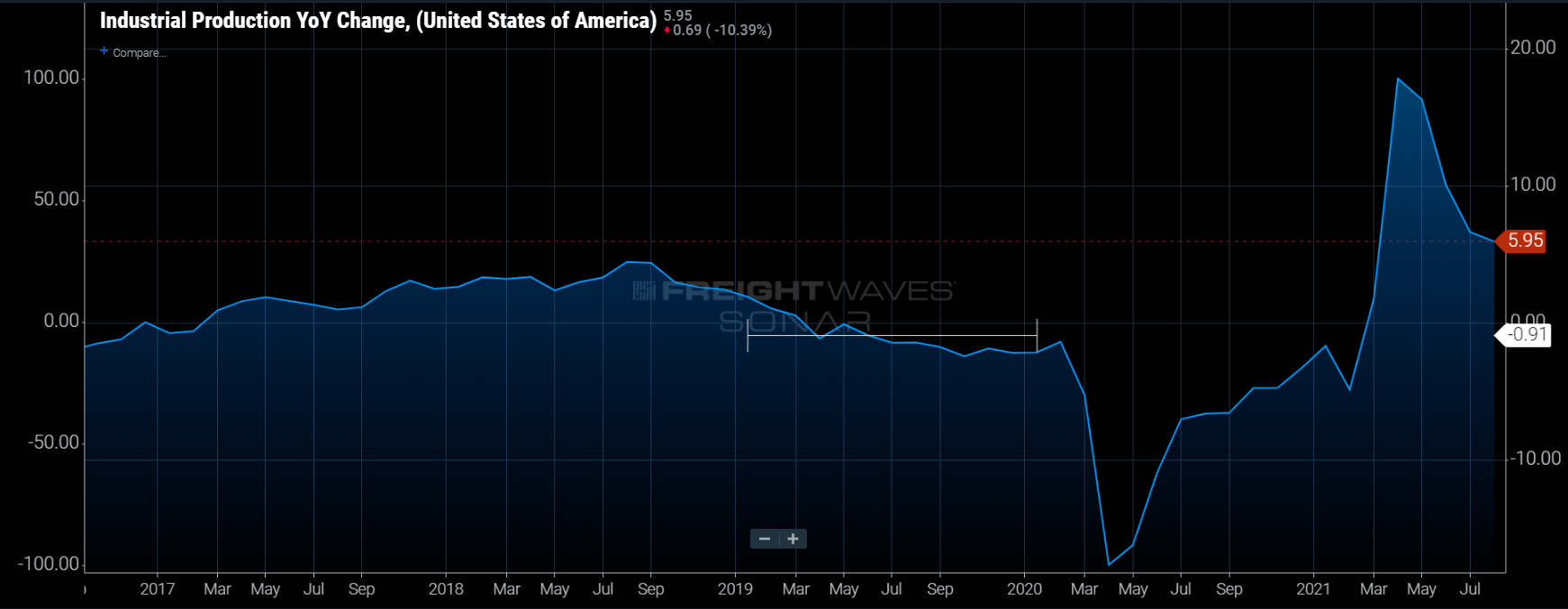

A sluggish industrial sector in which industrial production growth was negative for nearly a year indicated stagnant business and infrastructure investment, a sign that the economy was entering a phase of risk aversion and consolidation.

Once the initial wave of the pandemic hit the U.S. in March, many companies prepared for the worst by canceling orders and furloughing employees, entering survival mode as they expected economic devastation.

The government was able to quickly pass a stimulus package that spurred consumer demand to new heights. After a depressing April, consumers took the reins of the economic recovery by using the stimulus money and savings from not driving to work, buying new clothes and dining out to remodel their houses and purchase electronics. This was a shift in a large portion of the population’s lifestyle from a 9-to-5 commute to a remote work one, and the durable goods economy flourished.

The onslaught of unexpected demand in late spring caught most shippers and transportation providers off guard as they were expecting the next depression. They quickly found their once overstocked inventories depleted and needed to order more goods — all at once.

Panic hoarding

What most people do not know is that it takes months to build inventory levels to where companies like Amazon can offer two-day delivery on loofah sponges. With the pandemic interrupting production and shipping operations, shippers began to order not just for replenishment but for the future to avoid missing revenue.

Most consumer durable goods like electronics and furniture have origins overseas, largely Asia. Most of the population lives in the eastern half of the U.S. In order to get goods from China to New York City, it takes several weeks from the initial order date. So in order to prevent inventory shortfalls, shippers need to order months in advance.

As production and subsequently transportation capacity became strained, shippers learned to increase their order sizes. Port infrastructure does not increase in size overnight and transportation providers were reducing capacity prior to the pandemic, meaning demand quickly outstripped supply on multiple levels.

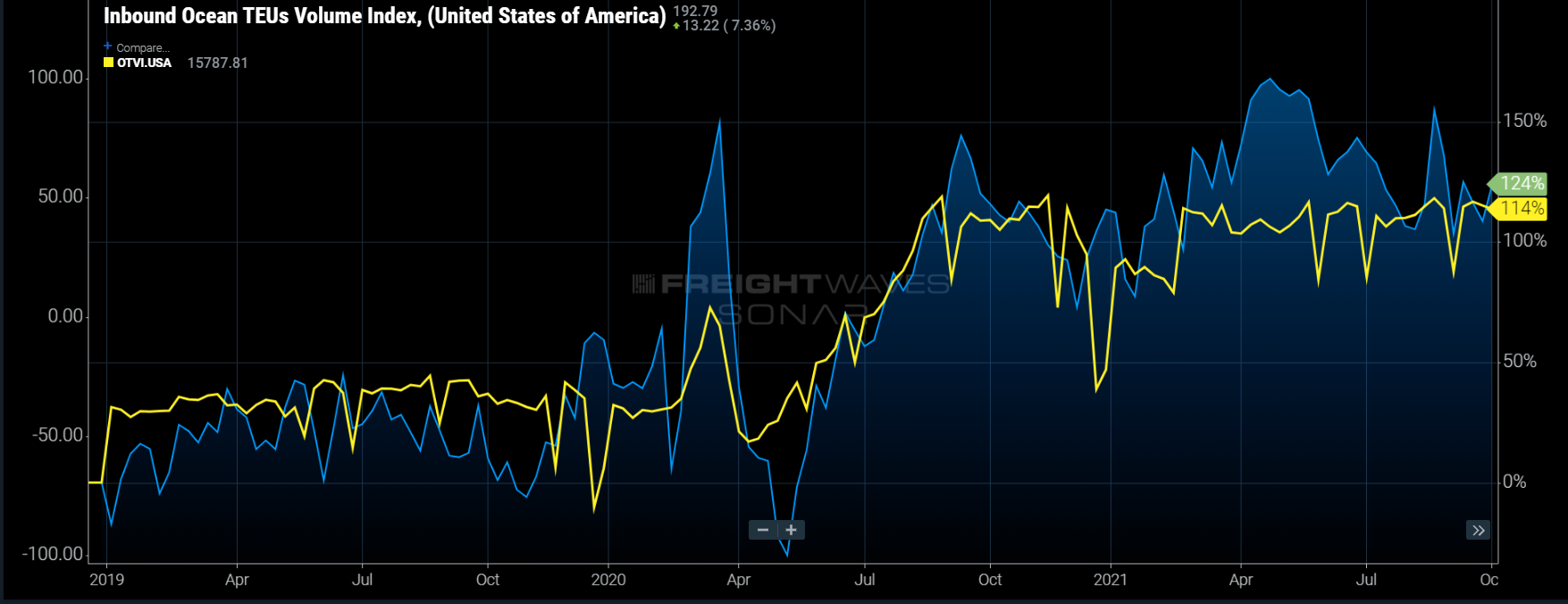

The violent swings in demand can be seen on the Ocean TEUs Volume Index (IOTI) that represents the container demand headed into the U.S. and the Outbound Tender Volume Index (OTVI) that measures truckload tenders from shippers requesting capacity. Both illustrate just how much transportation demand has grown over the past two years.

Supply side/infrastructure growth is slow

The supply side infrastructure is much slower to grow in response, limited by physical production and ironically supply chain constraints itself. An example of this would be Class 8 truck orders not being able to be completed due to limited availability of semiconductors and the subsequent transportation thereof. This expands upon the six to nine months to complete in general.

Expanding ports is a multiyear process and the focus on technological improvement around them is years behind due to the fact that it has never really been an issue until now. So the big question is how long will this cycle last?

The reality is that demand side easing will more than likely be the reason supply chains begin to unkink. Long-term improvements take years to implement and require decent investment. Look no further than road construction to see this in action. Any expansion project takes years from approval to completion.

To put it another way, look to the place where it all started in consumer behavior for the first sign of relief. Shippers will follow suit with industry not far behind.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new data sets each week and enhancing the client experience.

To request a SONAR demo, click here.