(Photo credit: Jim Allen/FreightWaves)

by Chris Henry and Daniel Pickett

The scenario is becoming all too familiar – you receive a notice from your current truck insurance provider that your premiums will be going up 25% for the next policy year. This raises your annual cost of insurance from $7,500 to almost $9,500 per truck per year. Oh, and you have to come up with all the money in 60 days (or be forced to finance the premium). Your insurance broker lets you know that you have options, and tells you that he’ll be going to the market to look for a better deal. The problem is that since last year three major insurers have exited the market, and the remaining ones are under pressure to rapidly increase premiums to offset rising claims and lower the liability related to nuclear verdicts. The situation is dire, and you have decisions to make.

In your conversations with other trucking companies, the word ‘captive’ has been mentioned many times, but you never really paid attention. The only thing you recall was that the companies who participated in captive insurance agencies did not seem to be as affected by premium increases in recent years. Maybe it’s time you start investigating further.

Why should you consider joining a captive?

For the purposes of this article, we are going to stick to the basics, and not confuse things with technical jargon that actuaries (equal parts accountant and statistician) like to use. Captives can be extremely complicated insurance arrangements with different ‘layers’ of ownership, responsibility and liabilities. For the trucking industry, most of the captive insurance programs act like a co-op – they are owned and controlled by the individual trucking companies participating in this ‘co-op-like’ arrangement. This type of captive is defined as a ‘group captive.’ Another spin on this arrangement is a company that is large enough to have its own captive without the need for other trucking companies to reduce risk. These captives are defined as ‘single parent’ captives.

The primary purpose of a captive is to insure the operating risks of its owners. At a basic level, if you become involved with a captive, you are making a conscious decision to accept a potentially larger amount of retention (deductible) per occurrence (accident), with the hope of pricing consistency over longer periods of time (which is not guaranteed), and control over policy/plan design. The latter objective typically doesn’t get the attention it deserves. Being involved in a captive gives owners access to a massive marketplace of ‘reinsurers’ that are willing to place bets on general and very specific risks – if you can dream it, these folks can price it.

The mechanics of a captive insurance agency

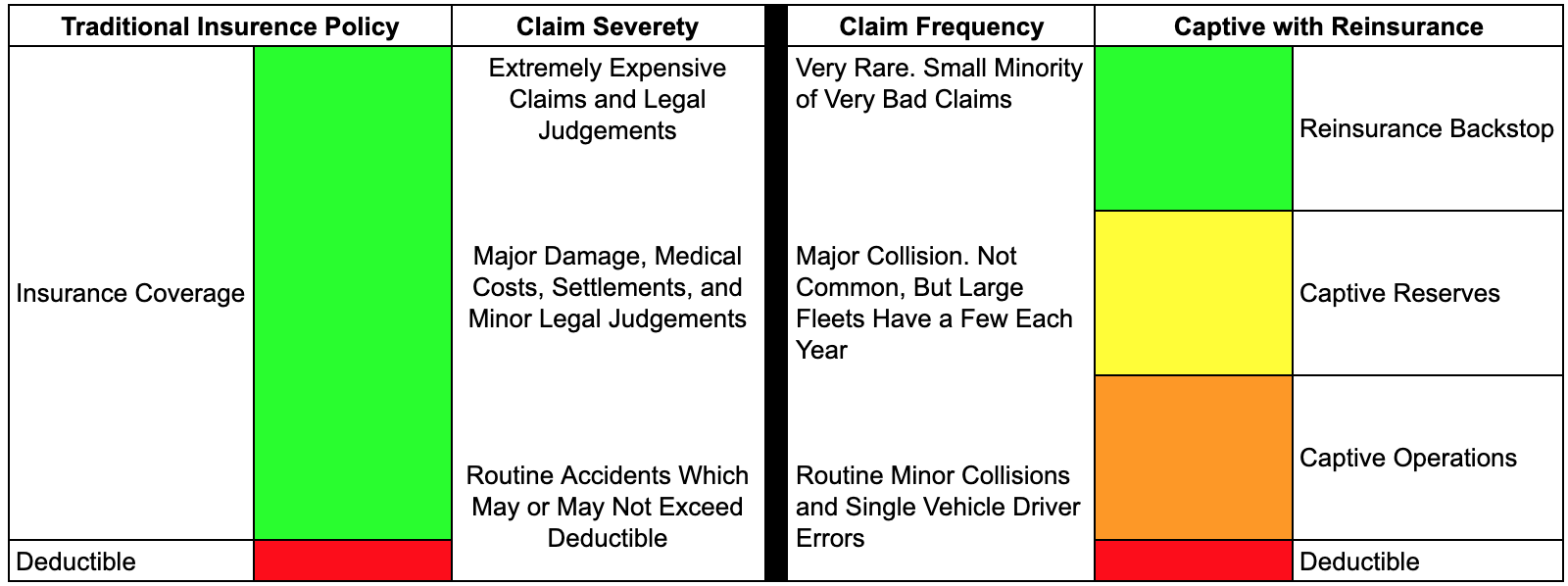

Source: Daniel Pickett/FreightWaves

With a conventional insurance policy, the policyholder is responsible for a deductible. Any losses in excess of that deductible are covered by an insurance company. Small, but common losses can include damage while backing up, single vehicle (truck-only) accidents, or low speed and not-at-fault collisions. Moving upwards, there are fewer truly cataclysmic collisions, but the dollar value can stretch into the millions when repairs, medical costs and legal penalties are considered.

A traditional insurer sets rates for all customers based on the frequency and severity of all the claims it receives. As such, if the pool of all customers increase the total claims payout, nearly every customer can expect increased premiums.

Source: Daniel Pickett/FreightWaves

By contrast, in addition to having the standard deductible, the owner (or co-owners) of a captive own a small insurance company that collects premiums and pays claims on smaller, more frequent, claims. That captive also purchases reinsurance, which will absorb the largest, most catastrophic claims. If the captive insurance company pays out less in claims than it collects in premiums, that surplus becomes the “reserves” of the captive insurance company. Healthy reserves allow the captive to either buy less reinsurance (thereby lowering premiums) or return capital to the owners.

Benefits of a captive insurance agency for a trucking company

Provides a large incentive to invest in safety – Your company may already be investing significant sums in safety-related training and technology. However, once you are the insurer, it forces captive owners to become extremely focused on safety. You’re no longer treating the symptom, you are treating the disease. Your Vice President of Safety will become a key part of the executive team (where they belong). In typical group captives, you will meet regularly (three to four times per year) and compare and contrast your accident/incident results with your fellow owners. Likewise, the group will share best practices and benchmark each other. The whole purpose is to lower the individual risk profiles of each owner, and overall as a group. A side benefit is that a safer fleet is a more profitable fleet (TPP has the data to prove it), and has lower driver (and non-driver) turnover. If done right, participation in a captive can have a compounding positive effect on culture and profits.

Stability in pricing and availability – This is the reason you considered captives in the first place. You’re sick of the song and dance each year, which starts 90, 60 or even 30 days before renewal. The outcome is rarely great, and there are always surprises, especially in recent years. Although you and your fellow trucking companies own the captive, they still need to be managed exactly like an insurance company. The capital reserves of the agency (and its owners) will be continuously monitored to ensure there are sufficient reserves to fund current and future claims. Likewise, the actuaries that are contracted directly or indirectly (through a broker manager) will set premium rates for current and future years, establish reserve funds, and generally report on the health of the captive. This is very serious stuff – captives can become insolvent, just like any other insurer and company, and can have very detrimental long-term effects on individual owners if mismanaged.

Improved cash flow – The two main ways that traditional insurers make money is: 1) pay out less in claims then they receive in premiums; and 2) invest the cash ‘float’ (cash reserves that the actuaries have deemed set aside from cash used to fund current claims) in various equities, bonds and other investment vehicles. In recent years, the latter has been the only way insurers (in trucking) have made money. Similar options are available to both group and single-parent captives, with the key point being that all profits accrue to the group owners – not the insurance company. If you are lucky enough to join a captive with a group of carriers with excellent claims performance, there will likely be a surplus of cash that can be returned to the owners via: 1) lower future premiums; or 2) dividends. We won’t get into the tax advantages of captives; however depending on the domicile (where the captive is established), there could be important tax benefits and avoidance benefits for captive owners.

Risks associated with a captive

You’re on the hook – Regardless of your current deductible with your traditional insurer, you will definitely be accepting much more risk oif you join a captive (whether directly or indirectly). If your broker has experience with, or manages captives, they will fully educate you and your team on the risks that are involved with joining a captive. The main risk is that you have little control over the daily practices that your fellow owners have implemented for their safety and compliance programs. That’s why it is very important that all members are vetted thoroughly by a professional risk professional to verify that a new (or existing) member doesn’t pose a hazard to the group.

Bad apples – Businesses change, executives change, people and companies can get complacent. Change (or lack thereof) can turn into a significant risk to the group. As trucking is the perfect supply and demand industry, short-term rate pressure can lead to improper short-term decisions. These bad decisions can be hiring unqualified (as defined by the group) drivers, spending less on collision mitigation and other safety technology or simply not monitoring critical events and addressing them via remedial training. If this begins to happen, you may not catch it until it’s too late – insurance is one of the most unforgiving business models that exists.

It’s not a piggy bank – Although captives provide significant cash flow benefits, it’s not a bank account. The amounts accruing to the group and individual accounts may seem too good to be true. That’s because they are. When an actuary states that the group cannot use a certain percentage of cash reserves (or all), they mean it. They are licensed professionals whose sole purpose is to keep the insurance company and captive solvent and sustainable. From a mental point of view, the best way to participate in a captive is to consider it your money when a potential claim arises, and someone else’s money when surpluses are accruing (until they pay out as dividends).

They are hard to exit – Every good thing comes to an end. Companies get bought, business strategies change, and traditional insurers come knocking with an offer you can’t refuse. The decision is made to exit the captive, and repatriate your cash. Sorry, that’s not how it works. It was hard to get into a captive, it is even harder to leave. Typically, you will not be able to fully exit a captive for five or more years if you decide to move on. That’s because of existing claims that need to be funded (both your claims and the group’s), as well as claims that are insured (based on policy wording) but have not yet been reported. These are called ‘Insured but Not Reported’ (IBNR), and you will always see an ‘IBNR’ reserve amount for both your individual account and the group’s account when the actuary does its periodic valuation of the captive. Based on experience, these calculations are eerily accurate over long periods of time. In summary, don’t think it’s an easy process to exit. As such, when making a decision to move on, you have to consider the lengthy process and the time value of money.