J.B. Hunt kicks off earnings season

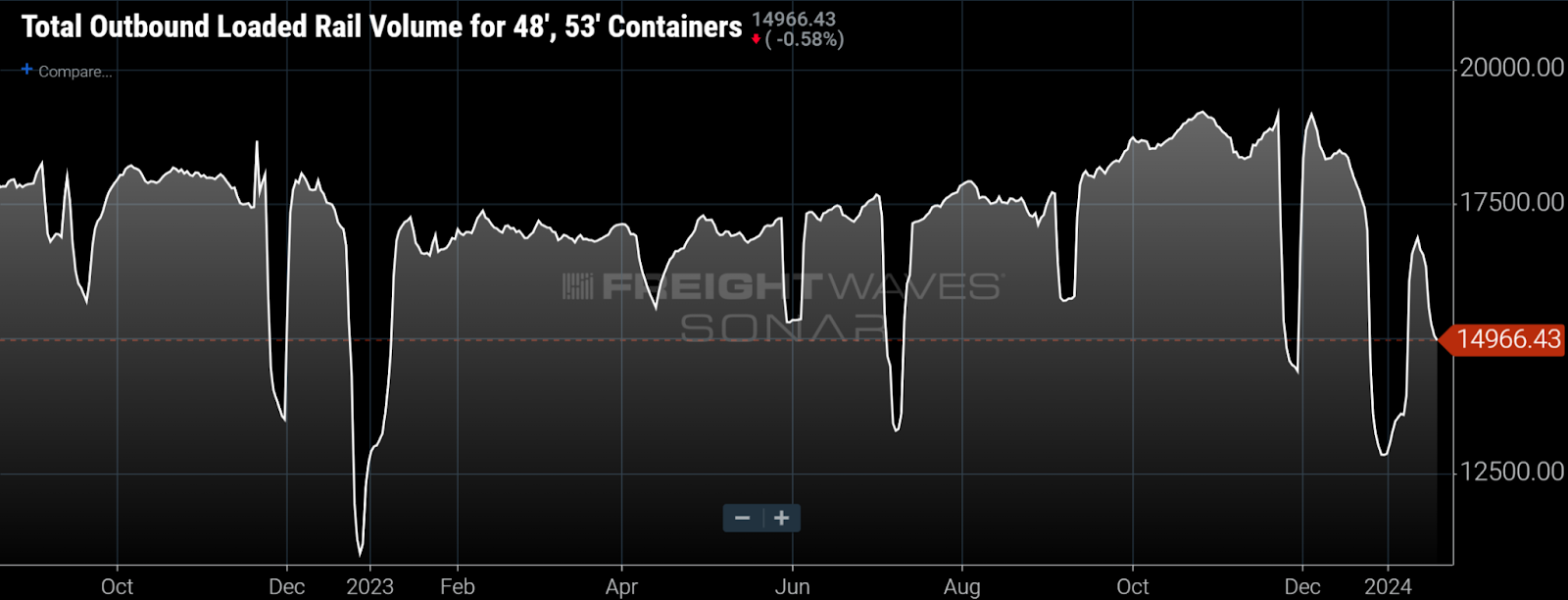

On Thursday’s analyst call (see Todd Maiden’s earnings writeup here), J.B. Hunt highlighted both improved intermodal volume and pressure on intermodal rates. Intermodal volume exceeded most industry participants’ expectations for a lack of peak season in the fourth quarter of last year. The carrier’s intermodal volumes were up 6.5% year over year in the fourth quarter, which implies market share gain when compared to the 5% y/y increase in loaded containerized domestic intermodal volume in SONAR (ORAILDOML.USA ticker).

Loaded domestic intermodal volume rose throughout 2023, peaking in the fourth quarter.

Comparing J.B. Hunt’s Q4 intermodal volume growth to SONAR data shows that the carrier outperformed the market by about 150 basis points in each of the past three months. J.B. Hunt intermodal volume increased 6% in October (versus up 4.4% for industrywide loaded domestic intermodal container volume in SONAR), up 6% in November (versus up 4.6% in SONAR) and up 8% in December (versus up 6.7% in SONAR). In the first 18 days of 2024, SONAR shows loaded domestic intermodal volume down 1.2% y/y, reflecting adverse weather.

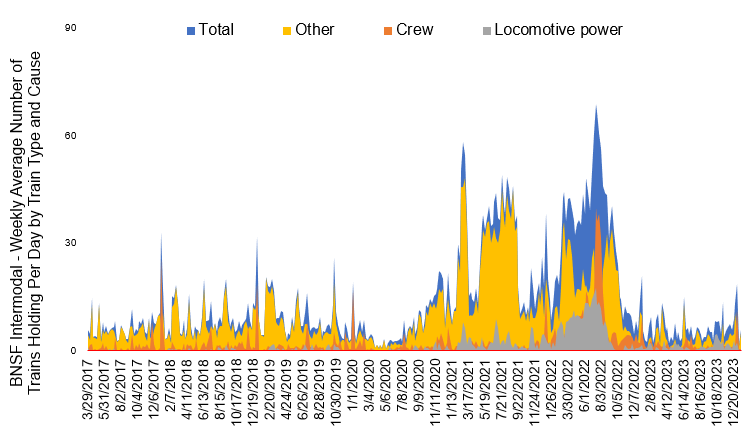

A metric for service, intermodal train holdings per day improved on BNSF, J.B. Hunt’s Western Class I rail partner, last year from disruptions experienced in 2020-2023. (Chart: U.S. Surface Transportation Board and FreightWaves)

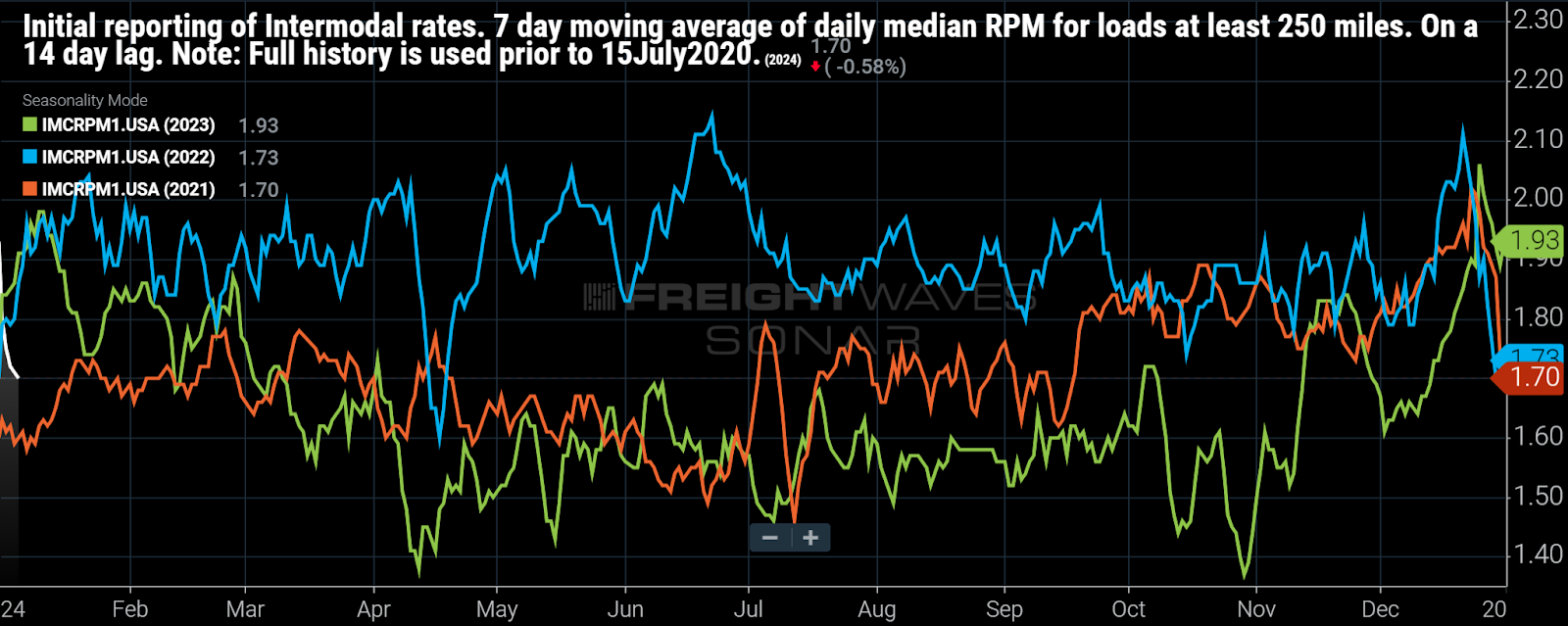

The company mentioned several times that it believes the improving volume is a leading indicator of market conditions and the rate pressure is a lagging indicator. The company’s revenue per load declined 12.8% in the fourth quarter (a metric that includes fuel, mix and changes in rates). That’s directionally consistent with the most comparable metric in SONAR, which shows a 9.7% decline in average intermodal rates per mile in the fourth quarter (chart below) — that number, however, excludes fuel surcharges. It appears, both from J.B. Hunt’s comments on Thursday and from discussion we had with shippers, that bids conducted during the fourth quarter resulted in significantly lower rates that will result in lower revenue-per-load and revenue-per-mile metrics during the first half of 2024.

Following bids conducted in H2 2023, average intermodal rates per mile started 2024 (white line above at left of chart) below the prior two years.

Potential Kroger-Albertsons close date pushed back

A major grocery merger is now expected to close by August, pushing back the initial close date of “early 2024.” According to Axios, the Federal Trade Commission is not expected to weigh in on whether the Kroger-Albertsons deal is anticompetitive until sometime in February. In December, the grocers informed the FTC that they believed they had met all the requirements for the merger following the announcement that 413 stores will be divested to C&S Wholesale. The state of Washington’s attorney general filed a lawsuit to block the merger, citing an expectation that merging the two chains will be to the advantage of nonunion retailers, such as Walmart and Amazon, which will ultimately hurt workers. A group of liberal lawmakers wrote to the FTC opposing the transaction.

The FTC has three options: (1) close its investigation, which would allow the deal to proceed, (2) ask for specific requirements before approving the deal, or (3) take legal action in federal court to block the deal.

For CPG companies, the merger would mean greater customer concentration, with the combined company representing 10% of sales or more for many CPGs. In addition, the combined grocer could become more aggressive in growing its private-label brands by promoting its bestselling private labels across grocery chains.

Retailers look to AI to assist in supply chain management

This article from SymphonyAI following the National Retail Federation (NRF) meeting outlines how retailers are looking to make productive use of AI. Demand and inventory forecasting are some of the use cases that have retailers most excited. The idea is that AI can incorporate a broader universe of data sets, considering more variables, to potentially improve demand forecasts for higher-in stock rates, fewer instances of over-ordering, and protection against potentially disruptive events.

FreightWaves’ John Kingston also wrote up takeaways from NRF (article here), which included an apt quote from Helen Davis, senior vice president and head of North America operations at Kraft Heinz, describing the benefit of AI to supply chains. AI processes at Kraft Heinz will look to create “data flows and a self-driving supply chain that can automatically reset itself when there are disruptions.”

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.