One more great quarterly result along with a healthy dose of caution from management teams were among analysts’ expectations heading into the third-quarter earnings season. J.B. Hunt Transport Services delivered both Tuesday after the market closed.

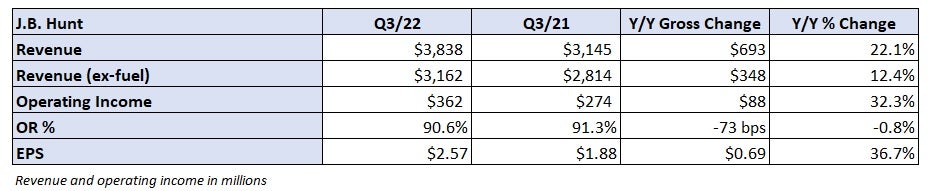

The Lowell, Arkansas-based company reported earnings per share of $2.57, 12 cents ahead of analysts’ expectations and 69 cents above the year-ago quarter.

Consolidated revenue grew 22% year over year (y/y) to $3.84 billion, which was also ahead of the consensus estimate. Excluding the impact of fuel surcharges, revenue was 12% higher y/y. The outperformance was primarily due to growth in the company’s intermodal and dedicated units.

However, as the freight market has moderated in recent months, “caution” and a “readiness to pivot” were management’s focal points on a call with analysts Tuesday evening. Management said it was exploring cost reductions in each of its five segments, with particular interest in right-sizing business units that have seen significant investment, like brokerage and final mile.

“Further evidence has presented itself over the course of the quarter that requires an increased level of caution and awareness on broader demand trends and economic activity,” said CEO John Roberts on the call.

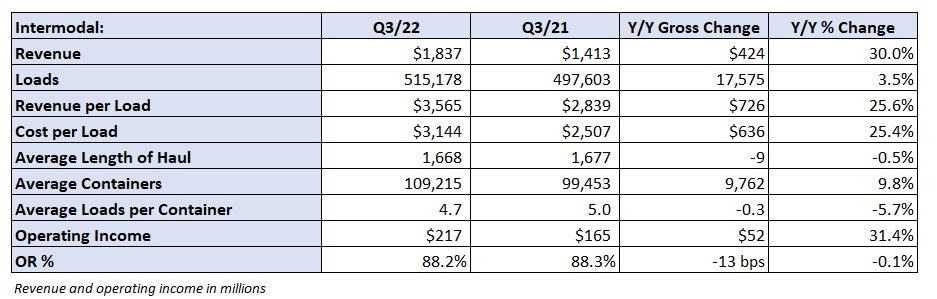

Intermodal service starting to improve

J.B. Hunt’s (NASDAQ: JBHT) intermodal revenue increased 30% y/y to $1.84 billion as revenue per load surged 26% y/y and loads were 4% higher. Higher fuel expenses drove a portion of the yield increase, but excluding the impact of fuel surcharges, revenue per load was still 17% higher y/y in the period.

The company’s intermodal contracts begin to roll over in the third quarter of each year, reflecting recent annual price negotiations. Yield was 5% higher than in the second quarter even though fuel prices were off by mid-single digits sequentially and length of haul only ticked up slightly.

“We believe the sequential increase mainly reflects a further improvement in core pricing, which should sustain through at least 1H’23 based on how JBHT’s contracts work,” Deutsche Bank (NYSE: DB) analyst Amit Mehrotra told clients in a note. “We note, for example, that the third quarter represents the highest level of new contract implementations, and so the sequential increase, we believe, is mostly explained by higher core pricing.”

Intermodal volume growth at J.B. Hunt outpaced the rest of the industry as intermodal container traffic on the U.S. Class I railroads was down 1% y/y during the quarter. However, the company did increase the container fleet by 10% y/y. J.B. Hunt recorded load growth of 4% y/y in July and 6% y/y in August. In September, volumes fell 2% y/y, in part due to the threat of a rail worker strike. Excluding the event, management said loads would have been up 3% to 4% y/y in the month.

So far in October, volumes are “back in line with where we were running throughout the quarter without that disruption,” according to head of intermodal Darren Field. However, he did acknowledge that “peak season this year just doesn’t appear to be much of an event,” although the company is taking market share.

Poor rail service and delays at customer facilities weighed on intermodal volumes and equipment utilization.

Container turns declined to 4.7 in the quarter, which was lower than five turns per box during both the second and year-ago quarters. Eastern rail partner Norfolk Southern (NYSE: NSC) saw rail speeds slow 8% and dwell time increase 17% during the quarter while Western partner BNSF (NYSE: BRK.B) saw velocity improve by 2% but dwell times rise 6%.

Field said rail service improved in the second half of August and throughout September. He remains hopeful that equipment utilization will improve at some point. “As we go through December and as we continue to highlight benefits from faster velocity to our customers, and as we go through the bid season, we absolutely do anticipate an improvement in the box turns.”

Pressed about plans to add as much as 40% in container capacity to the intermodal fleet over the next few years, Field said J.B. Hunt has the ability to be “agile” with the timing of additions so as not to upset the supply-demand dynamic. However, with BNSF’s intermodal rail franchise wide open for J.B. Hunt given the departure of competitors, the company isn’t backing down on its growth plans.

“We do absolutely anticipate an opportunity to grow from that scenario, and having equipment available and ready for that opportunity is one of the core important strategies for the next year.”

Intermodal operating income increased 31% y/y to $217 million. The division recorded 10 basis points of operating ratio improvement at 88.2%. Profit per load increased 27% y/y to $421.

Other Q3 highlights

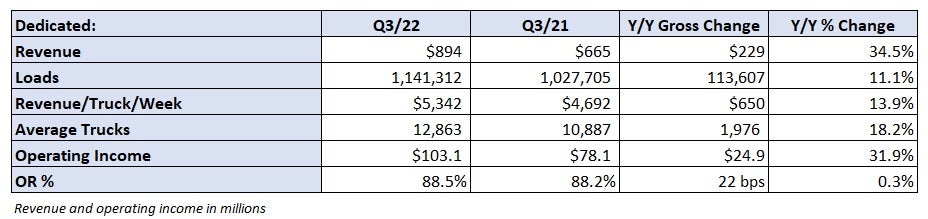

Dedicated revenue increased 35% y/y to $894 million. Nearly 2,000 additional trucks were in service on average in the quarter compared to a year ago, and revenue per truck per week was up 14% y/y (6% higher excluding fuel surcharges). Operating income increased 32% y/y to $103 million. Increased hiring and retention, equipment maintenance, and new account startup costs weighed on the OR, which deteriorated 20 bps y/y to 88.5%.

Typically, when dedicated demand moderates, margins expand as startup costs fade. However, higher fuel and maintenance expenses, as the unit is forced to run slightly older equipment due to production delays at the OEMs, will cap some of the potential margin improvement if demand declines.

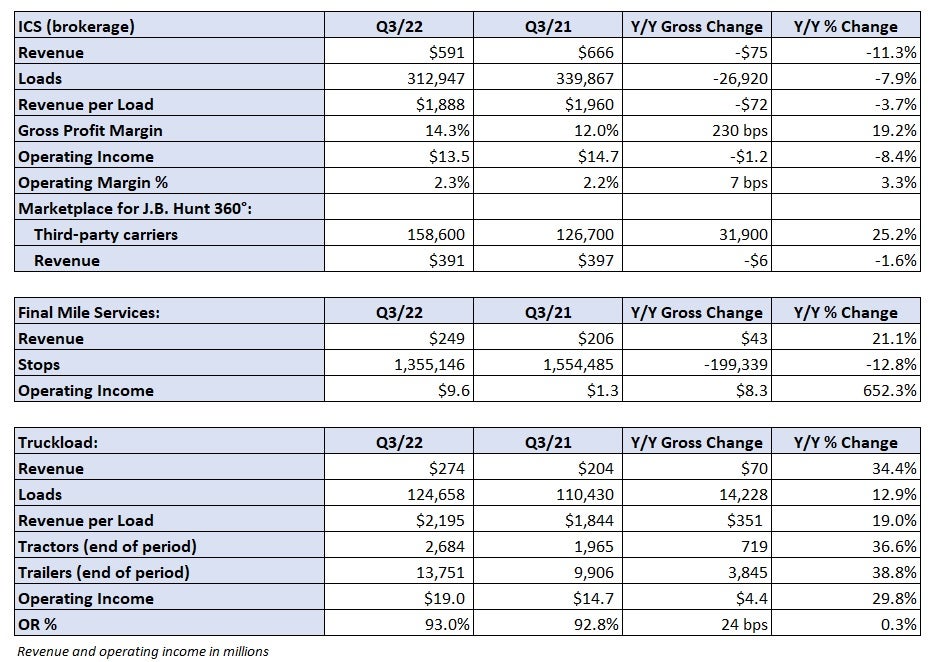

Brokerage revenue fell 11% y/y to $591 million as loads declined 8% y/y (truckload volume down just 1% y/y) and revenue per load was off 4% y/y. Revenue on digital platform J.B. Hunt 360 was down 2% y/y to $391 million. Operating income was down 8% y/y to $13.5 million. Higher personnel costs, tech-related expenses and bad debt expense weighed on results.

“We’re just navigating this current environment the best we can. It’s a fight out there for volume in the brokerage space,” said Brad Hicks, president of highway services.

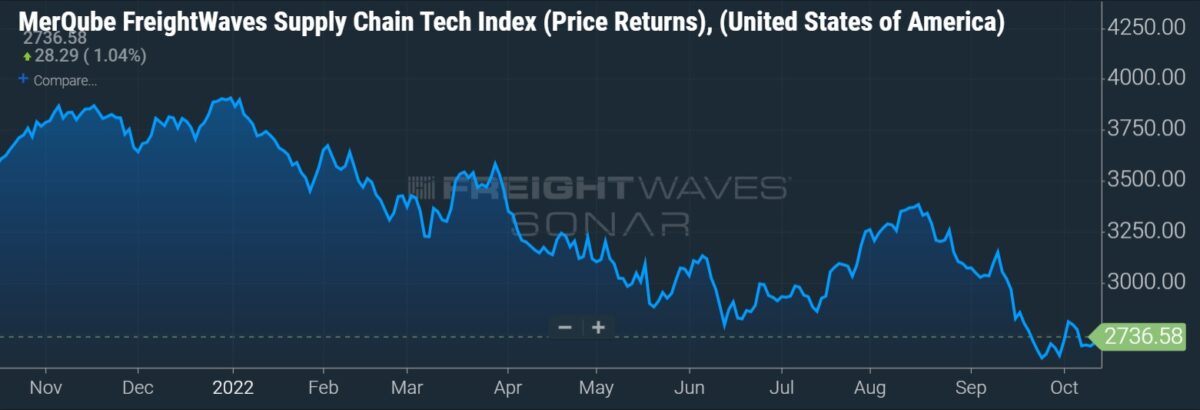

Shares of JBHT were up 2.5% in after-hours trading Tuesday. The stock is off just 3.8% since the company reported second-quarter results on July 19. By comparison the MerQube FreightWaves Supply Chain Tech Index (SCTI) is down 10.6% over the same time. The SCTI measures share price performance of tech-enabled supply chain services providers.

More FreightWaves articles by Todd Maiden

- XPO, RXO financial targets imply no letup through 2027

- Cass: September increase in shipments a head fake

- Transfix pulls IPO, new private funding round planned