J.B. Hunt Transport Services (NASDAQ: JBHT) updated operating income margin targets for each of its five divisions during its first-quarter earnings call Thursday evening.

The company slightly lowered its intermodal margin target to a range of 10%-12% from the prior range of 11%-13%. The dedicated segment’s margin target was raised by 100 basis points on each end to 12%-14%. Targets were reiterated in brokerage (4%-6%) and final mile (4%-8%). The margin target for the truck division was lowered to 8%-10% (from 8%-12%) as the division continues to transition to a more asset-light model.

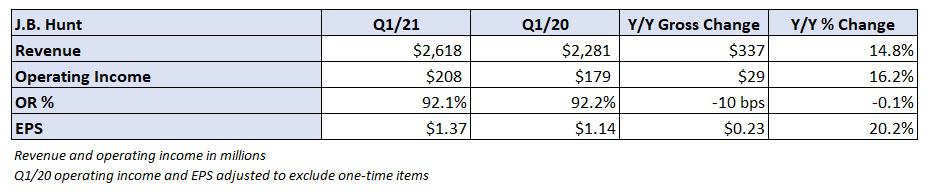

The Lowell, Arkansas-based company reported first-quarter earnings of $1.37 per share after the market close, 19 cents ahead of the consensus estimate and up 23 cents year-over-year on an adjusted basis. The first-quarter 2020 result included $24 million in one-time expenses – COVID-related bonuses, an accrual related to its revenue division with BNSF Railway (Berkshire Hathaway, NYSE: BRK.B) and equity-comp expense for executive retirements.

Intermodal target trimmed, backdrop likely improves in 2021

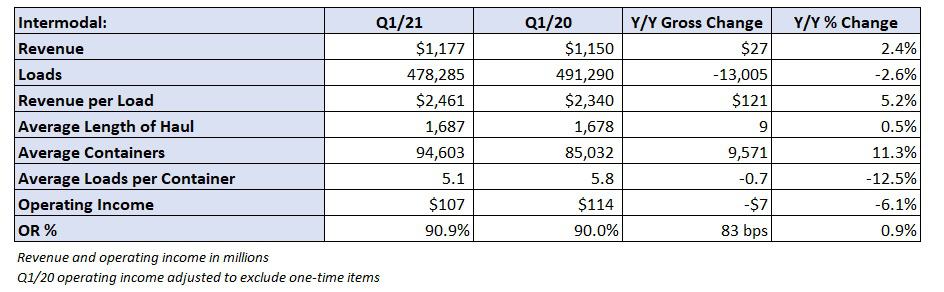

The division’s operating margin has hovered just north of 9% for the last two years as it has contended with several hurdles including arbitration expenses to settle a dispute on its BNSF contract, significant service headwinds due to precision scheduled railroading initiatives and pandemic-related port congestion.

Management said the revised intermodal target assumes some improvement in rail service but noted that velocity on the railroads is unlikely to reach the levels seen in recent years.

Rail service was an issue again during the first quarter. Since the beginning of March, J.B. Hunt has issued more than a dozen service advisories to customers. On Tuesday, the company posted a service notice explaining “container availability will remain extremely constrained throughout the country for the next two weeks.”

Poor weather contributed to a 3% year-over-year decline in intermodal volumes with 25,000 load opportunities being negatively impacted during February. Across the U.S. Class I railroads, intermodal traffic was up 13% year-over-year with J.B. Hunt’s partners BNSF recording a 19% jump and Norfolk Southern (NYSE: NSC) posting an 8% increase.

J.B. Hunt has struggled with load counts recently as container turns have declined. The primary culprits have been poor rail service and equipment getting stuck at customer facilities due to labor issues with dockworkers. During the quarter, loads per container dropped roughly 13% year-over-year.

In response, management has raised capital expenditure plans for 2021 by 40% to $1.25 billion. The company now plans to add 12,000 containers this year to its current fleet size of almost 100,000 boxes.

Excluding fuel surcharges, revenue per load increased 6%, but operating income fell by a similar amount, excluding one-time costs from the year-ago quarter. The weather impact to operating income was estimated to be a $17 million hit for the division.

Looking forward, management expects to grow the intermodal segment at a faster pace than the industry average. Loads were up by 3% and 4% in January and March, respectively, but 16% lower in February due to the disruption. Intermodal contracts are expected to reprice toward the high end of the prior guidance range of high-single-digit to low-double-digit rate increases.

Dedicated margin target ticks higher

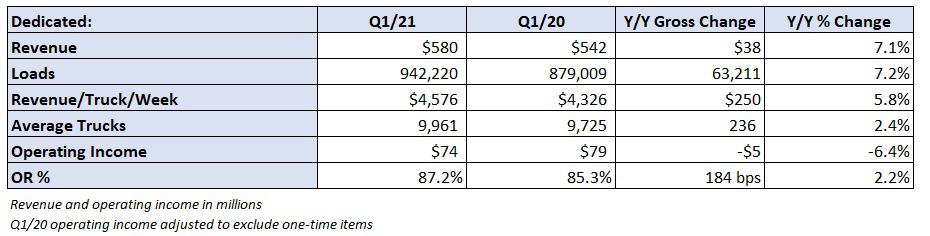

Dedicated revenue increased 7% year-over-year as loads increased by a similar amount. Revenue per truck per week was up 6%. Management said that it booked dedicated service for 380 trucks during the quarter. The company added 1,300 contracted trucks in the division in 2020 and plans to add 800 to 1,000 revenue-producing trucks per year moving forward.

The operating ratio deteriorated 180 bps to 87.2%, within the increased target range, as improved productivity was offset by wage inflation. Management called out difficulties with driver recruitment multiple times on the call.

Brokerage sees consecutive quarters of profitability

While the original guidance called for the brokerage segment to not achieve sustained profitability until the second half of 2021, the division posted its second consecutive quarterly profit. Brokerage revenue increased 57% year-over-year with higher revenue per load accounting for the increase. Total loads were down 1% but truckload volumes increased 10%. Management said the volume decline was primarily due to the loss of a less-than-truckload customer.

Higher spot and contractual rates resulted in a gross-profit-margin improvement of 280 bps to 12.4%. Favorable spot market conditions led to contractual volumes accounting for only 35% of revenue compared to 54% a year ago.

Brokerage revenue on digital freight platform, Marketplace for J.B. Hunt 360, increased 53% year-over-year to $359 million.

Management expects to hit the long-term margin goal through increased scale and productivity gains, noting that the division saw volumes increase as the quarter progressed. Another tailwind will be the wind down of investment in the segment.

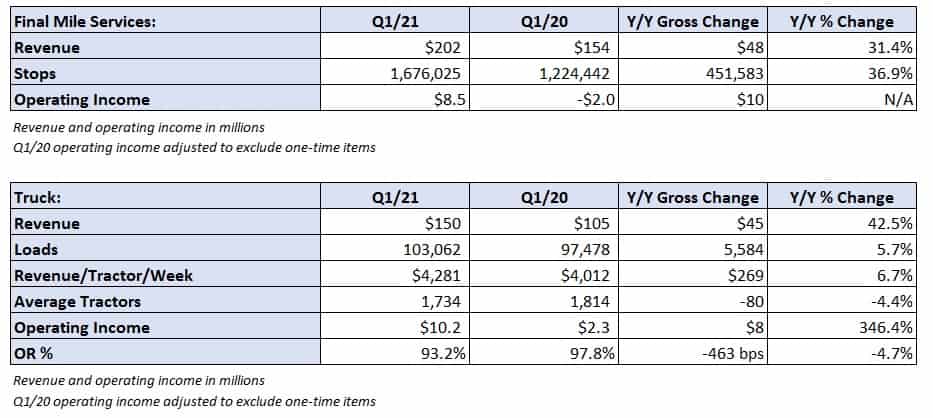

The truck and final-mile segments saw robust revenue growth and profitability improvements. Revenue per loaded mile, excluding fuel surcharges, increased 28% year-over-year in the truck segment, with contractual rates up 14%.