Landstar System noted a deceleration in trends during the 2022 third quarter on a call with analysts Thursday. However, the freight broker’s rate and load metrics have remained firm compared to the broader spot truckload market.

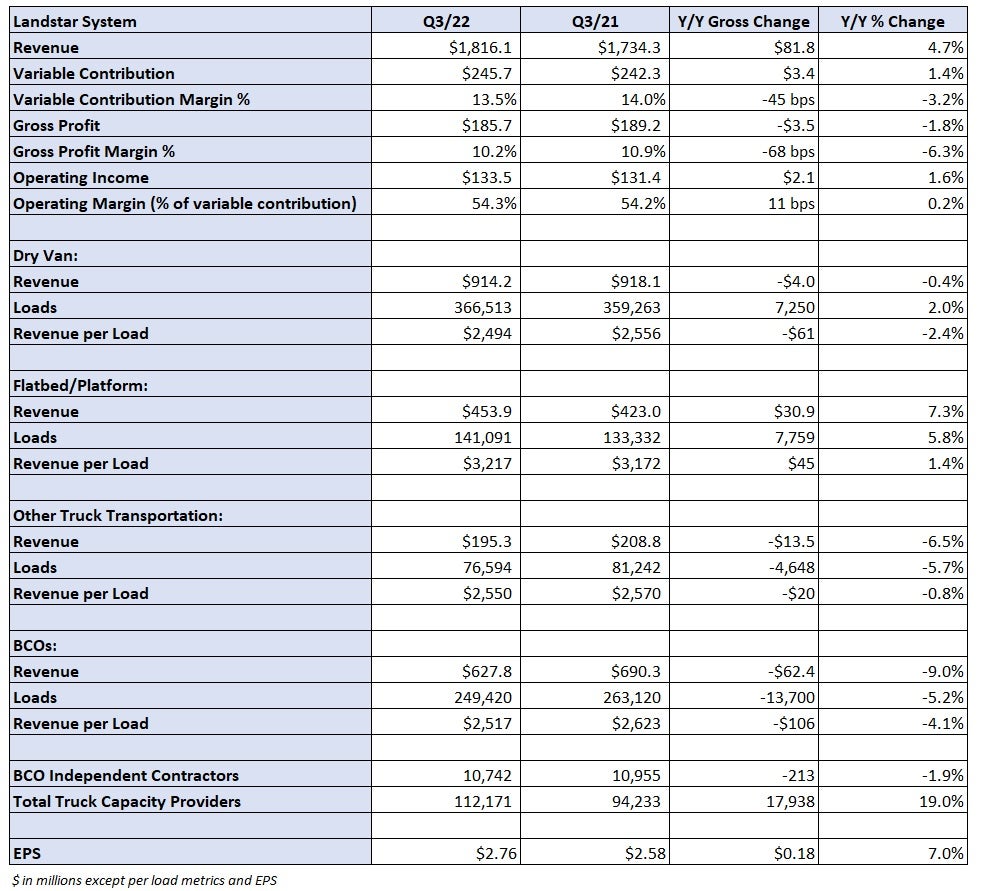

Landstar (NASDAQ: LSTR) reported earnings per share of $2.76 Wednesday after the market closed. The result was in line with analysts’ expectations but at the low end of management’s $2.75 to $2.85 guidance range. The result was a record for any third quarter in company history and 18 cents higher year over year (y/y).

Fourth-quarter guidance was slightly ahead of consensus forecasts at the time of the print. The outlook calls for revenue of $1.78 billion to $1.83 billion (compared to consensus of $1.73 billion) and earnings per share of $2.60 to $2.70 (versus consensus of $2.58).

So far in October, loads hauled by truck are down by a mid-single-digit percentage y/y. However, the 2022 fourth quarter has one extra operating week in which Landstar expects to haul between 30,000 and 40,000 loads. The company is forecasting volumes to only decline by 2% to 4% y/y in the period, with truck revenue per load expected to fall between 5% and 7% y/y (down 2% to 4% from Q3).

“Everybody’s [indicating a] flat to a soft, muted peak season,” President and CEO Jim Gattoni said on the call in regard to customer expectations for the fourth quarter. “Since our July call, I would say things have clearly softened up compared to the anticipation of a better peak season.”

Gattoni said the y/y comparisons get tougher moving forward as the freight economy was operating at record levels a year ago and that outperformance carried through the first half of 2022. Landstar reported an all-time high for EPS in the 2022 first quarter at $3.34. Its average revenue per load is down roughly 15% to 20% since then, and it cautioned that rates normally step down another 5% to 6% sequentially from the fourth to first quarters.

“I think it’s going to be an extremely tough first half next year, just on the comparisons and the direction of the economy,” Gattoni added.

Total revenue during the third quarter increased 5% y/y to $1.82 billion, which was near the midpoint of management’s guidance range. Total loads hauled by truck increased 1% y/y versus guidance of 3% to 5% growth. Truck revenue per load was flat y/y as expected.

A 2% y/y increase in dry van loads was offset by a similar decline in revenue per load. Revenue in the power-only, or “other truck transportation,” segment fell 7% y/y. The weakness was due to reduced demand from parcel and less-than-truckload carriers, which resulted in a 36% y/y decline in substitute linehaul revenue.

Flatbed revenue increased 7% y/y as loads increased 6%. Landstar’s revenue growth was highest in verticals like automotive (up 33% y/y), machinery (up 14% y/y) and building products (up 8% y/y) during the quarter.

Landstar’s yield metrics are outperforming general spot market rate trends, which have been off by roughly 30% y/y excluding the impact of fuel prices. Revenue per mile (excluding fuel) for business capacity owners (BCOs) hauling van freight was up 2% y/y in July, flat in August and down 4% in September. The metric is off only 17% from the February peak even though spot rates are down 40% excluding fuel over that time.

BCOs hauling flatbed freight saw record revenue per mile during the third quarter. However, the comps diminished as the period progressed, declining from up 9% y/y in July to just 2% higher y/y in September.

Capacity on Landstar’s platform increased 19% y/y to more than 112,000 providers. Trucks provided by BCOs declined 1% y/y and 2% from the second quarter.

Variable contribution, or revenue less purchased transportation and agent commissions, increased 1% y/y to $246 million. Variable contribution margin was down 50 bps y/y to 13.5% as the revenue mix included a greater percentage form truck brokerage carriers and multimodal providers, which utilize higher rates of purchased transportation.

Gross profit margin, which includes other variable costs like trailer depreciation and certain IT and insurance-related expenses, was down 70 bps to 10.2%. The operating margin, operating income as a percentage of variable contribution, increased 10 basis points to 54.3%.

Gattoni said even a 20% y/y decline in revenue next year would still produce an operating margin better than 50%, assuming insurance and claims expenses hold steady. That scenario would also generate $300 million in free cash flow.

Debt to capital was 10% at the end of the quarter. Year to date, Landstar has generated $436 million in cash flow from operations, double the amount in the same period last year. Operating cash flow in the first nine months of 2022 is higher than any full-year performance for the company.

Landstar will continue to return cash to shareholders through stock buybacks and dividend payments.

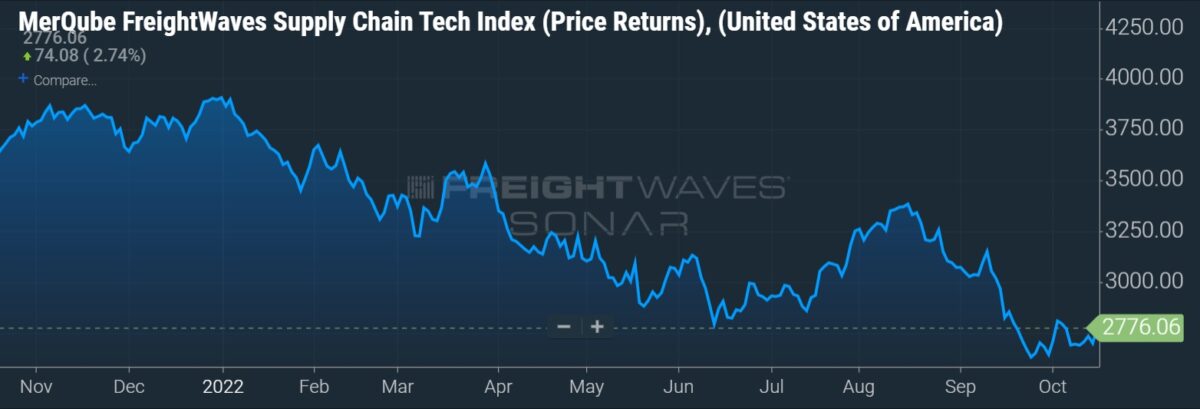

Shares of LSTR were up 3.3% at 11:02 a.m. EDT Thursday. Heading into the print, the stock was off 8.1% since it reported Q2 results on July 20.

By comparison the MerQube FreightWaves Supply Chain Tech Index (SCTI) was down 10.2% over the same period. The SCTI measures share price performance of tech-enabled supply chain services providers like Landstar.

More FreightWaves articles by Todd Maiden

- Logistics real estate market moderating but rents going higher

- J.B. Hunt looks to balance costs with moderating demand

- XPO, RXO financial targets imply no letup through 2027