ATRI: Cost of congestion to trucking hits $94.6 billion

On Wednesday the American Transportation Research Institute (ATRI) released its latest Cost of Congestion study showing U.S. highway traffic congestion added $94.6 billion in costs to the trucking industry. The study notes the states of Nevada, Louisiana, Georgia and California saw the largest increases.

FreightWaves’ John Gallagher writes, “ATRI’s 2021 congestion costs — based on the cost-per-hour to operate a truck, average truck highway speeds and the most recent truck volume data — were 22.4% higher than 2020’s and 27% higher than the 2016 baseline. During that same five-year period, the Consumer Price Index, a measure of inflation, increased 12.9%, ATRI noted.”

The report adds that delays increase trucking operational costs including driver compensation, fuel, repair and maintenance. Lower utilization and slower transit from congestion caused trucking costs to increase at twice the rate of inflation during 2021. Breaking down the data, the study noted that when distributing the overall costs to all registered tractor-trailers, the annual added cost came in at $6,824 per truck, or 3% of the revenue generated per truck in 2021.

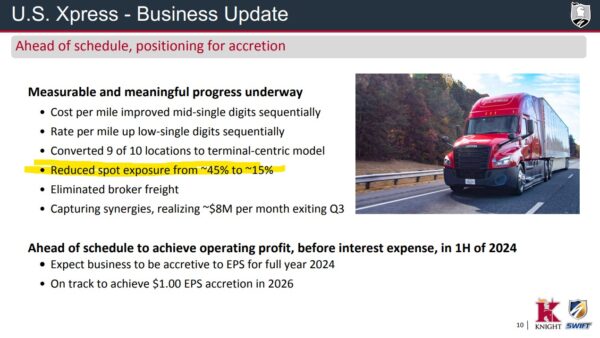

Knight-Swift highlights U.S. Xpress integration

Truckload carrier Knight-Swift’s third-quarter earnings release updated the progress on turning around U.S. Xpress, which was recently acquired by the company and closed in June. One major challenge involved getting USX’s spot exposure back to industry norms. Knight-Swift noted in a slide deck that its spot exposure was reduced from 45% to 15%. Typical large, nationwide truckload carriers prefer a spot-to-contract exposure of around 10%.

Part of this change involves adjusting the fundamental business model of USX. During the earnings call, David Jackson, president and CEO said, “U.S. Xpress is rolling out a decentralized terminal-based operating model similar to Knight-Swift where there is P&L accountability at the local level with far more personal driver interaction. Nine out of the 10 locations have been converted from places to park to operating terminals.”

Jackson noted that the bottom of the freight market cycle remains but there are early signs of market sensitivity when either truckload supply leaves the market or an incumbent carrier can no longer honor lower rates. He added, “However, we are not seeing enough of that kind of activity or enough supply leave and/or enough strength in volumes to move rates to a meaningful inflection position right now.”

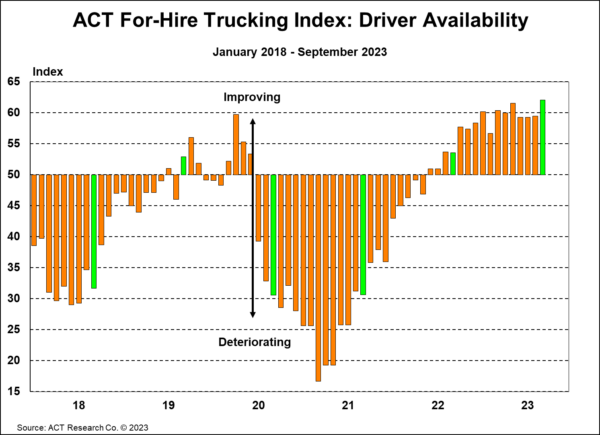

Market update: Gradual improvement for October For-Hire Trucking Index

On Tuesday, ACT Research released results for its October For-Hire Trucking Index, suggesting a gradually improving freight market. Notably, the driver availability index saw an all-time record high of 62 index points for September. An index reading over 50 indicates an expansion while a reading below 50 signals a contraction.

The report notes: “Fleets continue to see a large influx of drivers, unprecedented in our survey’s relatively brief history. We believe the source of these drivers is the challenged owner-operator market, which tends to rely on spot rates. With the scars of being unable to find drivers, or lure them away from stimulus money with the pandemic still fresh, employers across the economy are focused on labor retention.”

Truckload pricing recorded a 9.2-index-point improvement in September, to 48.5 seasonally adjusted as rates stabilize and capacity rebalancing continues. Volumes dipped 4.9 points to 49.5 compared to August’s reading of 54.4. The report is optimistic for future freight volumes in spite of declining consumer savings rates and private fleet growth, which have been headwinds for for-hire trucking volumes.

FreightWaves SONAR spotlight: More strikes, longer wait times for automotive

Summary: On Tuesday, the United Auto Workers expanded its ongoing strike to a crucial General Motors plant in Arlington, Texas, following GM’s reporting of its third-quarter earnings. The Arlington Assembly plant includes around 5,000 workers who produce the Cadillac Escalade and Escalade ESV, GMC Yukon and Yukon XL, and Chevrolet Tahoe and Suburban SUVs.

The ongoing strikes against the Detroit Three automakers appear to be causing higher-than-average wait times for automobile manufacturers, measured by the FreightWaves SONAR Wait Time index (WAIT). As of Oct. 15, a truck spent an average of 168 minutes at a shipper or receiver for loading or unloading, compared to a pre-strike average of 110 minutes.

The total impact of these lost automotive freight volumes is important for carriers exposed to these disruptions. Specialized automotive carriers are at the most risk from a prolonged strike, with either specialty equipment for transporting or an inability to replace the contracted automotive volumes on such short notice. Van outbound tender volumes remain muted as October draws to an end, down 285.91 points or 3.43% from 8,329.66 points on Sept. 24 to 8,043.75 points.

The Routing Guide: Links from around the web

Convoy’s shutdown exposes the desperate state of trucking (FreightWaves)

Death from overfunding: An obituary for Convoy (FreightWaves)

New data shows 14% decline in large-truck fatalities (FreightWaves)

Nikola claws back $165 million from founder Trevor Milton (FreightWaves)

How long will the capacity correction take? (FreightWaves)

Covenant Logistics Group sees Q3 revenue slip in weak freight market (FreightWaves)