ATRI predatory towing data

On Wednesday the American Transportation Research Institute (ATRI) released a report that examined causes and impacts of predatory heavy-duty towing. The report defined predatory towing in which “a T&R [towing and recovery] company egregiously overcharges, illegally seizes assets, damages assets by use of improper equipment, or illegitimately withholds release of a truck, trailer, and/or cargo.” When a trucking company is overcharged, it can happen in two ways, through either excessive costs or unnecessary additional equipment.

One of the impacts the report notes is these costs are passed on to insurance companies, which then pass on the charges as higher premiums. If the invoice exceeds the limits of an insurance policy, those extra costs are then absorbed by the motor carrier or driver, who must pay the difference out of pocket. Adding to the complexity, a patchwork of local and state towing regulations hampers efforts for carriers evaluating an invoice. Even after service is invoiced, there are inconsistent and nonstandardized invoice practices to cause further headaches for carrier accounting teams.

The report notes that the most common form of predatory towing is in the form of excess rates, according to 82.7% of the motor carriers surveyed. Unwarranted extra charges were a close second at 81.8% of those surveyed. An example of extra charges can be the hourly rate charged by a heavy-duty rotator versus a heavy-duty wrecker. The report adds, “Due to asset availability, rotators are sometimes used as wreckers, without the use of their rotating arm, and are thus billed at a wrecker rate.”

Price declines for used Class 8 trucks stabilizing?

Prices for used Class 8 trucks are beginning to see signs of stabilization but are still in flux, according to October data released recently by ACT Research. ACT reports that the used Class 8 average retail sale price came in at $62,900 in October, a decline of 1% month over month and down 25% year over year. A big question the report examines is whether pricing declines will continue or improve. The report predicts continued lower prices through the end of 2023 but expects m/m growth toward the end of 2024.

Steve Tam, vice president at ACT Research, said: “The answer to that question seems to be in flux. There are still too many trucks chasing too little freight. Until the economy can strike a balance between those two factors, downward pressure on pricing will continue to exist. Once the excess capacity is absorbed, the freight rate environment and trucker profits will correct, restarting the cycle that is the commercial vehicle industry.”

FreightWaves’ Alan Adler wrote that according to J.D. Power, “In October, the average sleeper tractor sold at retail was 71 months old, had 437,227 miles and sold for $67,441. A month earlier, the average sleeper was four months older, had 20,547, or 4.9%, more miles and sold for $4,240, or 5.9%, less.” Power notes that depreciation for 2023 is averaging 4.4% m/m with new model years showing values below the strong pre-pandemic period of 2018 and 20% lower when adjusted for inflation.

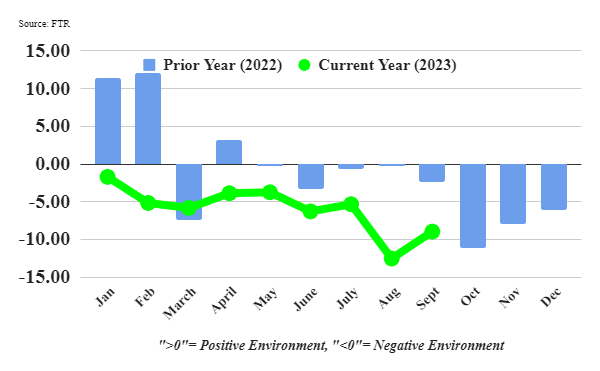

Market update: Trucking conditions improve in September

FTR Transportation Intelligence’s recently released Trucking Conditions Index (TCI) for September saw some improvement but tough market conditions remain. The TCI improved from minus 12.54 in August to minus 8.97 in September due to improving fuel prices and slightly higher freight demand. The index covers five major conditions in the U.S. full-truckload market, including freight volumes, rates, fleet capacity, fuel pricing and financing. A TCI reading above zero shows an adequate environment with a reading of 10 or above showing volumes, prices and margins are in a good range for carriers.

Avery Vice, vice president of trucking, noted in the report: “The TCI was less negative in September principally because fuel costs did not rise as much as they did in August, but trucking companies saw no real improvement in freight market conditions. Although carriers today are seeing some temporary relief due to the recent drop in diesel prices, freight rates look to improve only gradually over the next year. The trucking industry continues to struggle with more capacity than is ideal given sluggish freight volume. Many operations apparently are hanging on or maintaining driver levels in hopes of a near-term rebound, but that approach amounts to an increasingly high stakes game of chicken.”

FreightWaves SONAR spotlight: Spot market rates reheat post-Thanksgiving

Summary: All-in spot rates rose sharply in the past week and are at levels not seen since Oct. 10, according to the FreightWaves National Truckload Index 7-Day Average (NTI). NTI spot rates rose 3 cents per mile week over week from $2.26 on Nov. 20 to $2.29 per mile. Over the past month, spot rates rose 7 cents per mile from $2.22 all-in on Oct. 28 to $2.29 per mile. Truckload capacity leaving the market for the Thanksgiving holiday contributed to the rise, as fewer drivers competing on the spot market will cause a jump in rates.

Spot market linehaul rates with a projected fuel surcharge saw a similar jump from $1.60 per mile on Nov. 20 to $1.63 per mile, according to the FreightWaves National Truckload Index (Linehaul Only) or NTIL. Looking ahead, the NTI Forecast 28-Day outlook (NTIF28) projects all-in spot rates to rise 23 cents per mile from $2.29 to $2.52 by Dec. 26.

Spot market rate increases follow a seasonal pattern in which rates climb leading up to Thanksgiving, peak past Christmas and then begin a decline in the new year. This primarily is driven by truckload capacity changes in which drivers from fleets of all sizes take additional time off to spend with family just as truckload volumes climb for holiday replenishment orders. For truckload carriers, projecting and adjusting to changing working tractor percentages will remain a challenge, as customers expect higher service and tender compliance levels right as fewer assets are available to dispatch.

The Routing Guide: Links from around the web

Michigan trucking fraudster sentenced to 17 years for $40M Ponzi scheme (FreightWaves)

How to not just survive, but thrive, through the bottom of the freight markets (Overdrive)

Renewed migrant surge forces closure of Texas border bridge (FreightWaves)

‘An absolute privilege’: Werner drivers recount driving Capitol Christmas Tree (The Trucker)

Biden administration announces massive logistics plan (FreightWaves)

FMCSA administrator: Compensation, lack of parking among root causes of truck crashes (Land Line)