Florida seeks CDL skills testing waiver

The Federal Motor Carrier Safety Administration on Monday published a notice in the Federal Register that the state of Florida is seeking an exemption to the CDL testing regulation pertaining to skills testing. The Florida Department of Highway Safety and Motor Vehicles (FLHSMV) has applied for an exemption from the regulation that requires a three-part CDL skills test that must be completed in a specific order.

FreightWaves’ John Gallagher wrote, “Currently, federal regulations require the three-part CDL skills test — pre-trip inspection, basic vehicle control skills and on-road skills — to be administered and completed in that order. If an applicant fails one part of the test, he or she is not allowed to start the next part of the test but instead must return on a different day to retake all three parts.”

One reason behind this exemption request is that the third-party testers set aside blocks of time to conduct each driving test, often between one and two hours; if an applicant fails the first skills test (pre-trip inspection), then the application must come back at a later date. The challenge for skills examiners is waiting out the remaining time until the next applicant arrives for his or her scheduled testing block. The exemption could streamline and speed up testing, with the FLHSMV noting this “would allow their compliance staff to better utilize their time and resources in completing the required monitoring of third-party testers.”

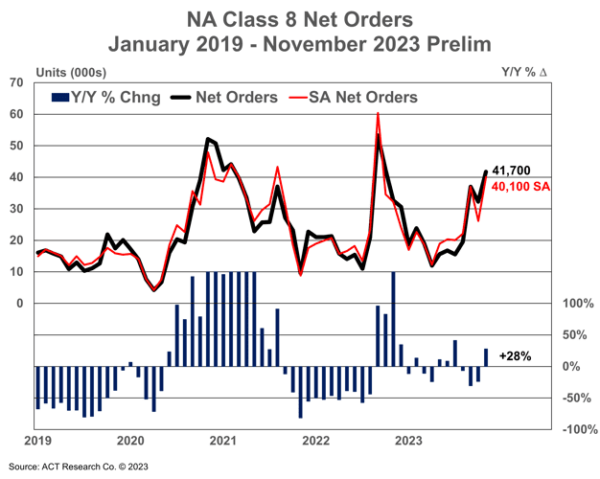

Class 8 preliminary orders surge in November

ACT Research on Monday released its preliminary Class 8 order data for November showing a surge in orders to 41,700 units, an increase of 9,000 units from October. The report notes this was the highest monthly intake since October 2022 and the best “real” order month since September 2022. Kenny Vieth, president and senior analyst at ACT Research, said in the report, “Even though backlogs, in seasonal fashion, are rising, they continue to point to a different market vibe heading into 2024: Still good, for sure, but solid, rather than stellar.”

FreightWaves’ Alan Adler wrote that FTR Transportation Intelligence reported lower preliminary orders of 36,750 units, up 30% from October and 2% year over year. FTR Chairman Eric Starks said, “Despite prolonged weakness in the overall freight market, fleets continue to be willing to order new equipment. Order levels were above the historical average but continue to follow seasonal trends, stabilizing our expectations for replacement demand in 2024.”

The stronger demand appears to also exist in other segments, with Paccar Inc. CEO Preston Feight noting in the company’s Q3 earnings call, “We see a really strong vocational market out there. We see a strong medium-duty market. The LTL market is very strong.” Feight predicts a strong Q1 for 2024 based on demand.

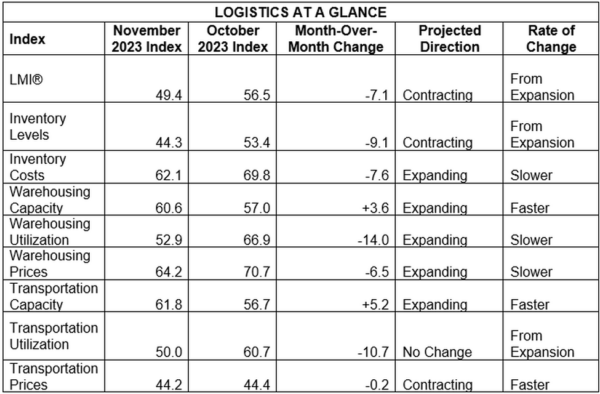

Market update: November LMI data back in contraction

The Logistics Managers’ Index November data, released Tuesday, showed the overall metric drop back into mild contraction. The overall LMI score fell 7.1 points from an October reading of 56.5 to a November reading of 49.4. This contraction marked the end of three consecutive months of expanding rates of growth and the largest drop since the ongoing freight downturn began in April 2022. Compared to last April, “November’s dip was largely triggered by a decline in Inventory Levels (-9.1) which is attributable to Q4 holiday sales and the subsequent dips in Warehousing Capacity (+3.6) and Transportation Capacity (+5.2) and slowdown in Warehousing Utilization (-14.0) and Transportation Utilization (-10.7),” the report said.

Regarding the significance of November’s drop, the report noted that the decline in inventory levels was from firms selling off inventories quickly compared to the decline in April 2022, when firms held too much and could not sell any of it. For shippers, the cost of transportation fell at a reduced rate. The report added, “It is interesting that Transportation Prices, which have been the lowest metric all year and are often the canary in the coalmine for the overall logistics industry, is the metric that had the smallest drop during November’s swoon.”

For a capacity outlook, it appears respondents predict further contraction. FreightWaves’ Todd Maiden wrote of the report, “Transportation capacity remained ‘prevalent across the supply chain’ and has been on the rise since April 2022, according to the Tuesday report. When asked about transportation capacity one year from now, respondents returned a reading of 48.2, with downstream participants like retailers expecting a faster rate of contraction (43.8).”

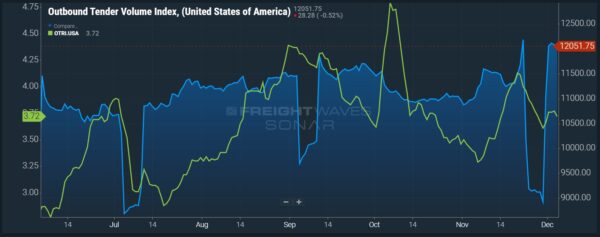

FreightWaves SONAR spotlight: Peak season outbound tender volume boom resumes

Summary: Outbound tender volumes nationwide (OTVI) remain elevated following the Thanksgiving holiday as shipping facilities reopen and clear freight backlogs. Looking at the past month, outbound tender volumes rose 9.23% or 1,018.7 points from 11,033.05 points on Nov. 5 to 12,051.75 points. Peak season saw an increase in van outbound tender volumes in the past month with VOTVI rising 10.1% or 796.36 points from 7,912.18 points on Nov. 5 to 8,708.54 points. Putting the post-holiday bump in context, outbound tender volumes, currently at 12,051.75 points, are 1,131.05 points or 10.36% higher than 2022 but remain lower than the record outbound tender volumes seen during the pandemic, which were 3,017.02 points higher in 2021 and 3,771.95 points higher in 2020.

The return of truckload capacity from the holiday caused outbound tender rejection rates to fall 1 basis point week over week from 3.73% on Nov. 27 to 3.72%. For fleets heavily exposed to contracted volumes, this slight decline suggests greater fleet availability during the holidays or that customers shipping contracted volumes had greater flexibility, removing the need to reject tenders that may be preloaded or dropped at a terminal to deliver at a later date. The spot market saw greater volatility from carriers exiting for Thanksgiving with the FreightWaves National Truckload Index 7-Day average (NTI) rising 4 cents per mile all-in from $2.29 per mile on Nov. 27 to $2.33 per mile. Removing an estimated fuel surcharge, NTI linehaul rates rose 5 cents per mile from $1.63 on Nov. 27 to $1.68 per mile.

The Routing Guide: Links from around the web

Average per-worker cost of health benefits rose by 5.2% in 2023: survey (Trucking Dive)

Feds told to start rating ‘unrated’ trucking companies for safety (FreightWaves)

VC-backed CloudTrucks exits factoring business to focus on core offerings (FreightWaves)

Truck parking expansion money still elusive on Capitol Hill (FreightWaves)

CARB Clean Truck Check Compliance Begins Jan. 1 (Heavy Duty Trucking)

FMCSA issues policy on sexual assault among truck drivers (FreightWaves)