Freight upcycle may come early, says Morgan Stanley

The freight recession may ease earlier than expected, according to recent comments from Morgan Stanley analyst Ravi Shanker. In a call to clients on Monday, Shanker said, “Shippers continue to remain on reorder ‘strike’ while they wait for stronger signals or more favorable conditions on macro but while destocking at the same time, which could lead to everyone wanting to restock at the same time, when the coast clears (or they run out of inventory).”

Shanker believes the freight upcycle will begin as early as the end of Q1 while admitting this prediction was “out of consensus.” His prediction is based on Morgan Stanley’s recently released Q4 2023 shipper survey that showed ongoing inventory destocking at historic levels. Regarding the survey results, FreightWaves’ Todd Maiden writes, “Of those polled, only 5% said they needed to increase inventory levels. Thirty-nine percent of respondents said they would reduce stock levels, which was a notable decline from the cycle-high of 48% that was registered during the second quarter.”

This optimism is most likely not going to be noted in Q4 2023 earnings and guidance in the coming weeks. Shanker predicts management teams’ outlooks will “be a tale of two halves” with the first half of the year clouded by macro uncertainty followed by the back half spurring more constructive commentary. Shanker concludes, “We are more bullish as we believe the pressure to restock is likely to be more intense than carriers or shippers believe. We believe only a black swan event or severe recalibration of macro expectations will push the upcycle into 2025.”

New independent contractor rule ‘Much ado about (almost) nothing’

After a yearlong effort, on Wednesday the Department of Labor formally released its final rule effective March 11 on “how to analyze who is an employee or independent contractor under the Fair Labor Standards Act (FLSA).” The new rules are part of an effort by the Biden administration toward rolling back a previous final rule by the Trump administration that was enacted in 2021 before Trump left office. The difference is in the details. The Trump 2021 rule focused on an “economic realities test” created by courts with core and noncore factors to be considered. Under the Biden 2024 rule, the economic reality expands to covering six factors, with a seventh “additional factor” examining if a worker or business is economically dependent on the potential employer for work.

Trucking lobbyists decried the Biden rule, with American Trucking Associations President Chris Spear saying, “I can think of nothing more un-American than for the government to extinguish the freedom of individuals to choose work arrangements that suit their needs and fulfill their ambitions,” In comments issued Tuesday, Todd Spencer, president of the Owner-Operator Independent Drivers Association, wrote, “Truckers are tired of the endless parade of classification rules that do not listen to their concerns.”

Richard Reibstein, attorney with Locke Lord who blogs on independent contractor status issues, is less concerned. FreightWaves’ John Kingston notes, “That apocalyptic view of the rule differs sharply from what Reibstein wrote. In his blog posted Tuesday, he referred back to an earlier statement of his on the proposed rule. ‘Unlike most regulations with hard and fast rules, the regulation was in the nature of an administrative interpretation comprising the Labor Department’s review of existing court decisions and its articulation of a preferred legal analysis … [that] courts would give little if any deference to.’”

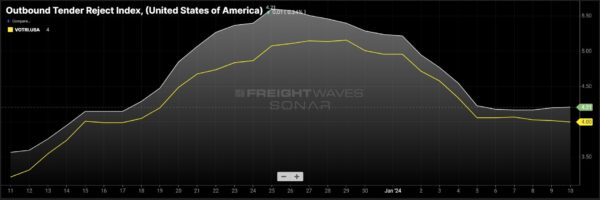

Market update: Outbound tender rejection rates settle post-New Year

Nationwide outbound tender rejection rates stabilized this week following a brief rally leading up to New Year’s. The Outbound Tender Reject Index fell 56 basis points week over week from 4.77% on Jan. 3 to 4.21%. Dry van rejection rates saw a similar decline, falling 58 bps w/w from 4.58% on Jan. 3 to 4%. Truckload capacity returning to the market is the most likely cause as drivers who took extended holiday time off return to work and fleets reposition assets to cover committed freight. Reefer and flatbed tender rejection rates continue to overperform the average, with reefer at 7.29% and flatbed at 8.76%, respectively, but their share of the overall freight marketplace remains small compared to dry van freight.

A development to monitor will be ongoing winter weather and storms moving across the U.S. into next week, bringing significantly lower temperatures. The weather may impact truckload operations in the Upper Midwest, Great Plains and Northeast. Spot market rate declines, which normally begin the second week of January, are declining at a slower rate as weather-related volatility may be a factor. Smaller fleets and owner-operators exposed to regions impacted by weather events may reposition assets further south unless primarily customer-routed. The FreightWaves National Truckload Index 7-Day average declined 4 cents per mile in the past seven days, from $2.43 per mile all-in to $2.39 per mile. Removing an estimated fuel surcharge, NTI linehaul rates (NTIL) fell 4 cents per mile w/w from $1.81 on Jan. 3 to $1.77 per mile.

FreightWaves SONAR spotlight: Trucking exits accelerate over the holidays

Commentary courtesy of the Daily Watch, a newsletter for SONAR subscribers

Summary: The truckload market was down over 6,800 operating authorities over the last 10 weeks of 2023. That is compared to approximately 5,500 down through the last 10 weeks of 2022, according to Carrier Details analysis of Federal Motor Carrier Safety Administration data. The takeaway is that the freight recession is continues but is moving toward an end at a faster pace than it was at this time last year from a supply perspective. Most transportation service providers are simply wondering how long they have to hold on in order to come out on the other end — the billion-dollar question. While no one knows for certain when the market will shift, the data says that it is coming. If there were no changes in capacity, then the market shift would be totally dependent on demand conditions changing. Outside of seasonal swings, demand conditions seem relatively stable. Supply-side changes tend to be much slower and carry more momentum, meaning overcorrection is very likely when the market flips.

The Routing Guide: Links from around the web

‘Leave us alone’: Union labor and trucking (Commercial Carrier Journal)

Supreme Court rejects review in broker liability case, leaving the issue unresolved (FreightWaves)

Kodiak reveals production-ready autonomous truck at CES (FreightWaves)

PS Logistics acquires flatbed, dedicated hauler Buddy Moore Trucking (FreightWaves)

We got too accustomed to peaceful seas (FreightWaves)

DOT tangles with watchdog over $1.5 billion in freight grants (FreightWaves)