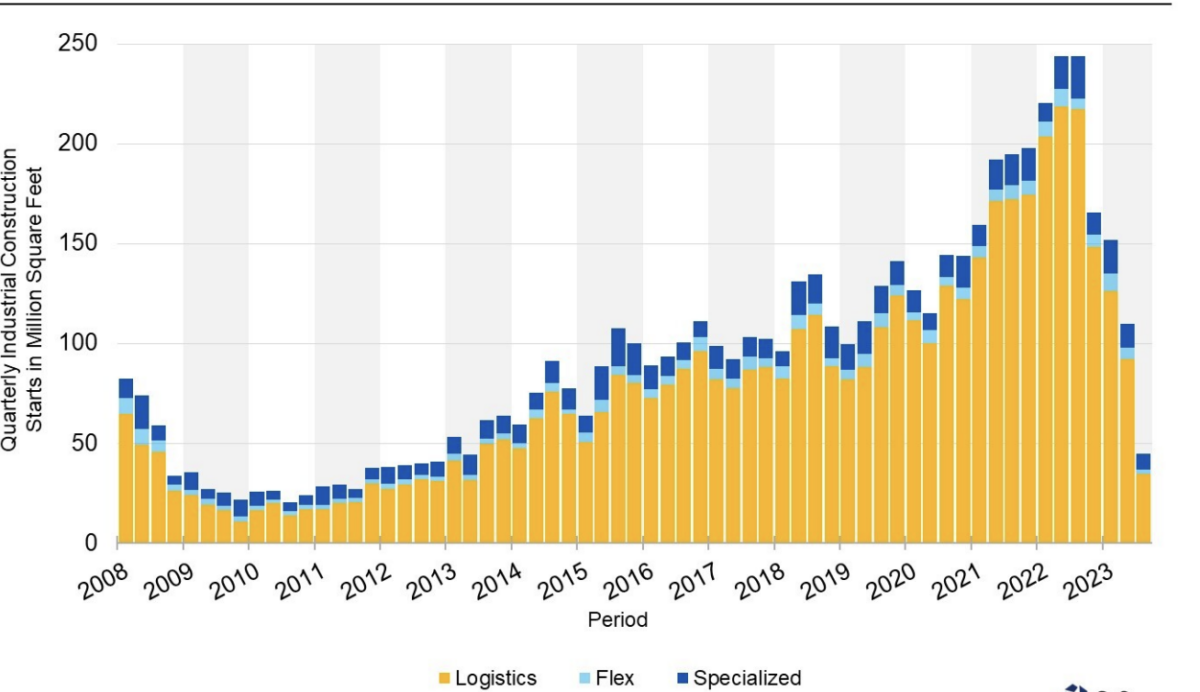

The volume of U.S. logistics warehousing construction starts has plunged to its lowest levels in nearly 10 years as higher interest rates and weaker end demand have combined to virtually shut down new construction, according to a commercial real estate research firm.

According to CoStar, not since the first quarter of 2014 have logistics construction starts — defined as concrete being poured and metal placed in the ground — fallen so dramatically. The present-day decline has hit every major market, even those markets like Dallas/Fort Worth and Phoenix that aren’t land constrained and have plenty of space for development, CoStar said.

Net absorption, the net change in the amount of space occupied in a given period, has also declined as retailers with fortunes closely tied to the residential housing and office markets pull back their warehousing footprints due mainly to the impact of higher rates on all real estate transactions. Even third-party logistics providers, a bulwark of industrial demand, have been easing off the pedal, CoStar said, noting that demand from e-commerce providers remains relatively solid.

The dramatic rise in borrowing costs has resulted in a knock-on effect on the logistics warehousing ecosystem. Banks that have long deployed capital for industrial construction have been saddled with large nonperforming loans on office development. This has made banks reluctant to lend for any type of transaction, even though the industrial segment is not nearly in the same challenging boat as the office market, CoStar said.

Developers that have dealt for many quarters with high labor costs now face higher costs of capital as well. Institutional investors, a key factor in the unprecedented bull market for logistics warehousing, are demanding lower prices as compensation for higher interest expense.

Adrian Ponsen, director of U.S. industrial market analytics for CoStar, said in an interview that he was surprised by the magnitude of the decline. At the same time, he has been surprised that interest rates have continued to rise and that the Federal Reserve seems comfortable with raising them again, or at the very least, keeping them higher for longer.

The waterfall decline in starts is a story that won’t play out until the latter half of 2024 and into 2025, said Ponsen. Current projects, 70% of which have been under construction for at least nine months, will be seen through to fruition, he said, adding that those facilities will be delivered within the next six to nine months. Industrial starts had reached their highest levels in 30 years during 2022, despite slowing in the final months of the year. Many of the projects in the pipeline have been delayed due to an ongoing shortage of various building components, CoStar said.

The fallout late next year will become evident should a rebound in logistics warehousing demand collide with an acute dearth of supply. If occupancy rates return to near historical levels, tenants will be faced with paying materially higher prices for space, Ponsen said.

Atlanta, one of the nation’s leading logistics warehousing markets, is the poster child for the current cycle. Atlanta went into the downturn before other major markets and will likely emerge from it before others do, Ponsen said.

In the meantime, construction starts in Atlanta for the past four quarters have totaled just 6.2 million square feet, according to CoStar data. That figure is more than 70% below the average for construction starts during the previous two years and less than half of the annual net absorption that Atlanta averaged over the past five years.

This translates into very little new industrial space wrapping up construction in late 2024, CoStar said. “If tenant demand for additional space during that period is anywhere close to the market’s long-term average, the market for distribution space there will tighten significantly.”