It’s no secret the logistics industry has faced significant pandemic-related volatility throughout the past two years. With 2021’s elevated rates and strained capacity, many shippers are holding out hope for significant rebalancing in the new year. They may need to wait a little longer, however, as experts suggest current market conditions could last well into 2022.

David Spencer, Arrive Logistics director of business intelligence, expects most of 2021’s challenges will bleed into 2022. Relief is unlikely to come quickly on the supply side as carriers continue to grapple with the driver shortage and parts shortages push delivery of 2021 new truck orders into mid-2022.

Instead, the reprieve is more likely to come from the demand side as consumers reevaluate their spending habits in light of rising prices and waning pandemic-fueled financial support, including the resumption of paused student loan payments in January.

“Demand will be impacted by consumer sentiment throughout the year. Costs of both goods and housing are rising, and despite recent news of President Biden’s Cabinet extending student loan debt relief, the impact on consumer spending is just pushed out further down the road,” Spencer said. “These influences on consumer spending should then translate to declines in truckload demand.”

Impact on demand is pushed further down the road. The impact to consumer sentiment should be the same, assuming the relief does not get extended again. President Biden’s Cabinet recently extended the relief on student loan debt.

As of right now, however, demand is stronger than ever and shows no indications of an immediate post-holiday crash. Changes on the demand front are likely to be slow and steady, leading to gradual market shifts over the course of the next several months.

The current peak season is proving to be a strong one, with demand up significantly over already elevated pre-peak levels. Nationwide freight volumes remained elevated in November; imports continued to flow into the country at record levels as consumers checked off their holiday shopping lists and stores worked to keep shelves stocked.

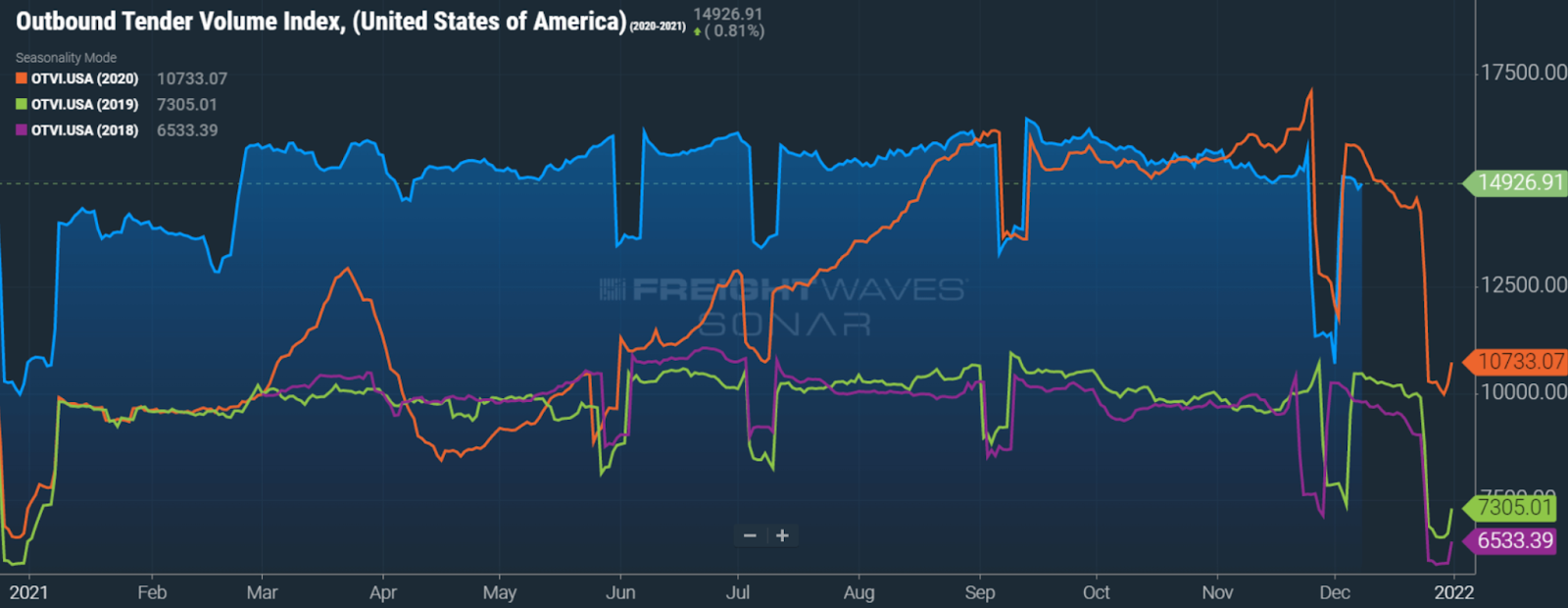

The FreightWaves SONAR Outbound Tender Volume Index (OTVI) was down 5% year-over-year in early December. This index includes both rejected and accepted load tenders, however, and must be evaluated in light of the FreightWaves SONAR Outbound Tender Reject Index (OTRI) to measure accepted volumes.

Combined data from the OTVI and the OTRI indicates that accepted volumes were actually up 3% year-over-year in early December. Tender rejections are currently down about 25% year-over-year. In fact, rejection rates are currently at their lowest levels since July 2020.

Decreasing tender rejections indicate that freight is being moved at contract rates, a hopeful sign for shippers. Still, with a rejection rate of over 19%, it is clear that strong demand and constrained capacity are continuing to stress the market.

Unfortunately for shippers, both spot and contract rates have continued to climb as demand surges, shortages drag on and peak retail season continues. In early December, dry van spot rates climbed to $3 per mile for the first time ever. Dry van contract rates reached an all-time high — $2.96 per mile — at the same time, according to Arrive’s December market update.

It is worth noting that stores do not seem to be having trouble keeping products on the shelves, even with strong demand and port bottlenecks. In mid-November, information from the White House’s Transportation Supply Chain Dashboard indicated that on-the-shelf availability was at 90%, down just 1% from pre-pandemic levels. These numbers indicate that strong demand is not likely to bring more volatility to the market in the short term, as current import levels seem to be supporting consumer demand.

Ultimately, Spencer does not anticipate much change as the calendar ticks over into 2022. When change does occur, it is unlikely to be swift or severe. This means shippers should prepare to continue wrestling with current headwinds.

“We’re looking at significant challenges, but we are at a new water level right now,” Spencer said. “We probably won’t see any more surprises in 2022, aside from weather or another unprecedented event. From where we are, we’re expecting conditions to improve gradually.”

Spencer recommends that shippers stay the course in the coming year. They should continue to adopt price-saving technologies, grow their networks, and, perhaps most importantly, foster strong relationships with carriers. All these efforts combined will help shippers navigate continued high rates and capacity constraints well into 2022.

“From a shipper perspective, if we do start to see market improvements, that is an opportunity to start to capture savings on their contract freight,” Spencer said. “This is especially true for shippers who have moved away from the annual RFP.”

Shippers that can create more flexibility in their transportation strategies will fare best as conditions gradually improve in the upcoming year. Moving away from annual RFPs in favor of shorter contracts is one way shippers can take full advantage of any upcoming rate drops. While these shippers are also exposing themselves to slightly more risk in the event of unexpected rate hikes, taking a chance just may pay off in 2022.