Like an elementary school-aged kid that stayed up several hours past their bedtime, the freight market appears to be showing signs of exhaustion after an extended period of overexertion. As we discussed last week, this October has been a far cry from the same month in 2017. Tender rejections for the U.S. have been falling steadily throughout the current month to today’s value of 13.06%. At this time last year, tender rejection rates hovered around 23% until mid-November until they shot up to 28% preceding the Thanksgiving holiday.

This year’s base is far lower than 2017, so it is probably safe to assume we will not see the same level of instability and therefore less rate volatility heading into the holiday season. That does not, however, mean the market will be flat for the rest of the year.

Inventories have been building as record inbound container volumes were reported at the U.S. ports this week. The Institute of Supply Management’s Inventories Index, which gauges inventory levels in the U.S., reported a 53.3% value in September, an indication that inventories are still growing in the manufacturing sector. The influx of containers could mean a big late year surge in freight volume is in order.

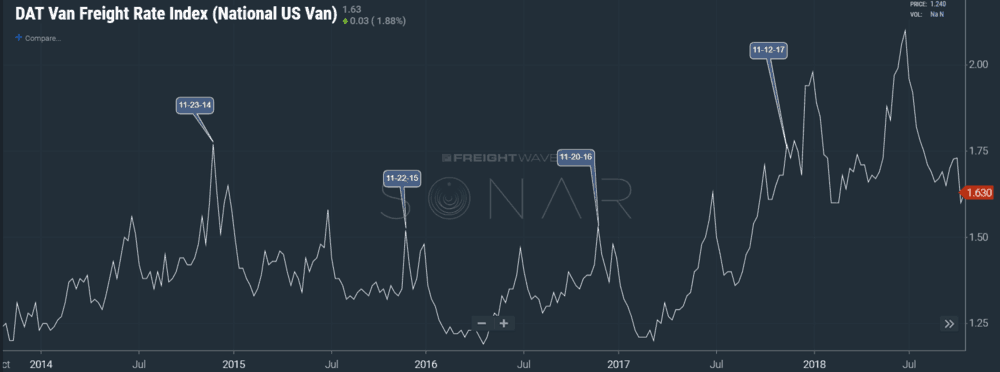

History tells us that a mid-November surge in spot market rates is inevitable, even in down years. Looking at the National DAT Van Freight Index we can see the pre-Thanksgiving spike in spot market rates in each of the past four years. Of course, this rate pressure is not entirely volume-driven, but timing also has a lot to do with it. Driver availability declines due to vacation schedules, and shipping lead times shrink as production windows narrow to get the inventory to the stores and distribution centers.

This year feels like we will see a pattern more like 2015, where the late fall peak is lower than the mid-year one. Historic rate increases as well as the addition of incremental capacity should temper the market into the late fourth quarter. The market is also starting this season without any major preceding disruption as the two major land-falling hurricanes did not disrupt capacity on a large scale this year like Harvey and Irma in 2017.

Volume is also at the lowest levels we have seen since winter. The fact that we are seeing lower volume at this point is concerning, but it probably feels more exaggerated due to the fact the market is coming down from 10-year highs. Regardless, this will help keep the market tempered in the near term. Increases in contract pricing also has a stabilizing influence on the market. Carriers are less likely to turn down loads with rates that are 10-20% higher than those last year.

An economic reason for the apparent market slowdown is the industrial economy starting to show signs of slowing as input costs are starting to catch up to manufacturers. In recent weeks OEMs like Wabash, the largest publicly traded trailer manufacturer, have cited rising steel and aluminum cost increases are keeping them from turning a profit.

The freight market has lost some steam along with the economy, but there will be another late year surge. There are signs of market correction after an extended period of expansion. Most understand seasonality, but looking at the cycles each year there are significant differences in their amplitude.