National freight volumes dropped slightly over the past week with average volume running 0.16% less than the previous week. The national Tender Volume Index (TVI) fell from a value of 9563.6 to 9548.54 this week as the market continues to remain relatively stable. The TVI indicates we are roughly 4.5% lower than March 1 volumes of last year, the period on which the index is based. As we get closer to that date, the farther the value is below the 10,000 base level becomes more significant.

The capacity remained relatively unaffected as the national Tender Rejection Index (TRI) hovered around 7.6% this week, about 10 bps lower than previous week’s average. The Midwest remains the tightest region with the most volume with tender rejection rates climbing above 11%. The inclement weather and relatively stable supply of freight are making things tighter. Western markets are looser, with rejection rates falling to 2.74%.

Many industry and economic analysts are calling for a softening market and economy in 2019 and so far, the data is supporting a slower market than we saw last year. After starting 2019 off with stronger than expected volumes, the market has slowed steadily. Capacity has followed suit, with national tender rejection rates dropping from over 14% on January 1 to 7.53% — the lowest point since index inception last January — on January 30. Since the beginning of February there has been little to no change in the daily value as it sits at 7.55% as of February 20.

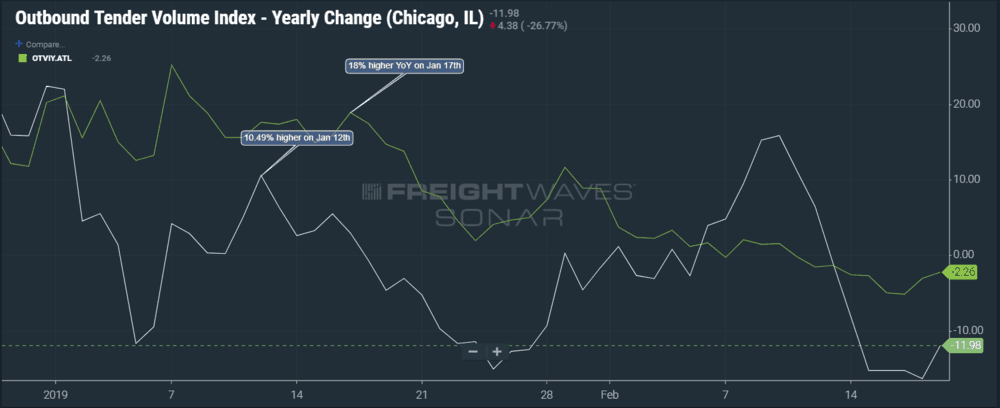

Volumes have started to fall under year-over-year values in some of the larger markets such as Atlanta, down 2%, and Chicago, down 12%. Both markets started off 2019 averaging roughly 16% and 4% higher volumes, respectively. In contrast, the Los Angeles market is seeing outbound volumes 62% higher than this time last year.

Southern California is still the largest outbound area of the country, with the Los Angeles and Ontario markets representing almost 8% of the total U.S. outbound volume. The L.A. market is averaging about 20% higher daily volume than it did at peak levels in 2018. Most of this activity is still regional, as inbound volumes remain high into the Stockton, Ontario, and Phoenix markets as the port city deals with the excess inventory. Inbound volumes are up proportionally to L.A. outbound volumes in each of those markets.

In terms of maritime freight, the Freightos Baltic Index rates, which measure the average spot rate for 40-foot container shipment, from China to the North American West Coast were flat this week, indicating no real change in volume or capacity. Rates from China to the East Coast fell about 2.3% this week, however, as there was little hope for those ships to hit the port prior to the impending March 1st tariff deadline. Interestingly, the rates from Europe to North America’s East Coast jumped 29% from $1,400 to $1,976, perhaps on looming concerns over automotive import tariffs. No real impact to the freight market has been observed in the data from this yet.