(Editor’s note: A table posted yesterday by FreightWaves of key financial and operational data from Marten had errors. That table has been removed. The accompanying table is accurate).

Third-quarter earnings at Marten Transport were negative almost across the board, with little sign of a truckload market recovery visible in the numbers.

The company was profitable; it posted net earnings of 5 cents per share, down from 17 cents in the third quarter of 2023 and 10 cents per share in the second quarter. According to SeekingAlpha, the consensus forecast was for Marten to earn 8 cents per share in the third quarter.

But beyond that, the numbers painted a picture of a truckload carrier for which virtually all metrics were deteriorating, not improving.

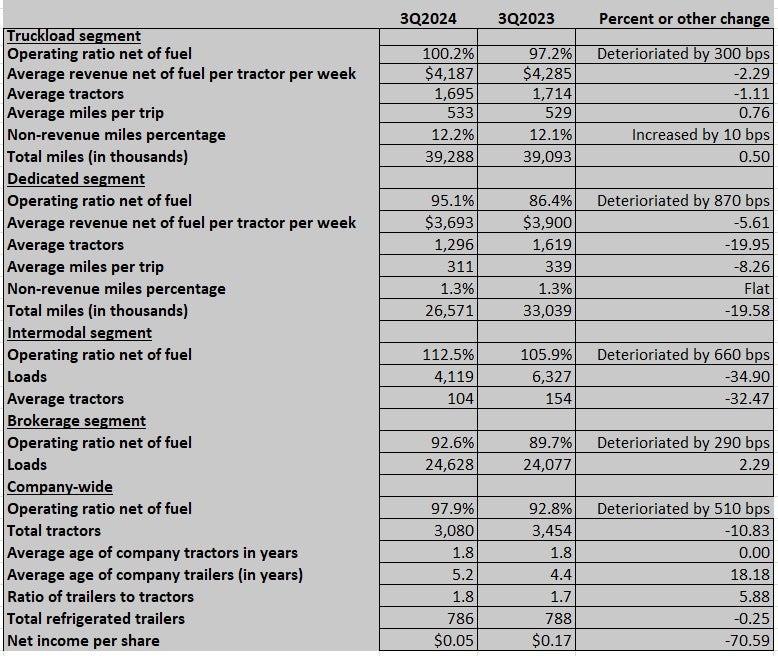

Start with operating ratio. Companywide, it was 97.9% for the quarter, compared with 92.8% in the corresponding quarter of 2023 and 95.3% sequentially from the second quarter of 2024.

The Truckload segment at Marten (NASDAQ: MRTN) posted an OR net of fuel for the quarter of 100.2%, 300 basis points worse than a year ago and 140 bps worse than in the second quarter.

Dedicated’s OR net of fuel blew out to 95.1%. That’s a whopping 870 bps worse than in the third quarter of last year, and a 500-bps deterioration from this year’s second quarter.

Marten does not hold a conference call with analysts. FreightWaves has reached out to the company for comment.

In previous quarterly earnings releases, Executive Chairman Randolph Marten has noted that the company has not been chasing rates down a sliding market. That was not mentioned in this quarter’s commentary from Marten.

In both the second- and third-quarter earnings releases, Randolph Marten was quoted as saying: “We are focused on minimizing the freight market’s impact on our operations while investing in and positioning our operations to capitalize on profitable organic growth opportunities, with fair compensation for our premium services, across each of our business operations for what comes next in the freight cycle as the market moves toward equilibrium.”

But in the second-quarter statement, that was followed by his declaration that “We have not agreed to rate reductions since last August.” That was not in the third-quarter statement.

The earlier declarations suggest Marten may have been turning its back on some business because of rates it saw as untenable and possibly unprofitable.

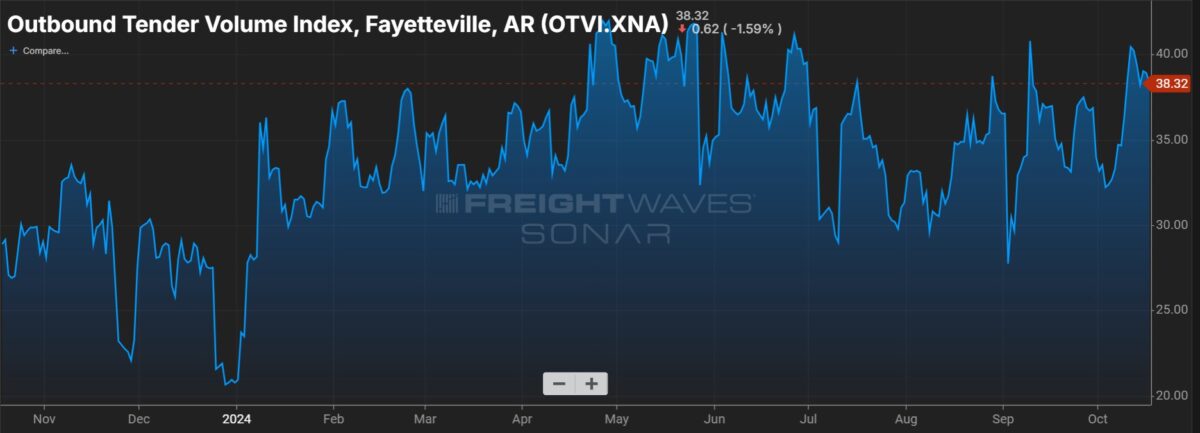

There are hints within the earnings report that has occurred, given that overall volumes in the trucking market have remained relatively steady, per the Outbound Tender Volume Index in SONAR. But that hasn’t happened at Marten.

For example, total miles driven in the Truckload segment were 39.29 million. That is down almost 3% from the figure in the second quarter but just 0.5% from the third quarter a year ago.

But in the Dedicated segment, where declining rates that would be the basis for a longer-term deal might be more of a deterrent for Marten to avoid the low-rate conundrum, the decline was steeper. Total miles driven in the Dedicated group were down 5.9% just from the second quarter and a whopping 19.6% from a year ago.

That falloff in business may be behind the sharp drop in the number of tractors in the Dedicated segment. The total was down almost 20% from a year ago, to 1,296 from 1,619. Tractors in Dedicated were down 6.2% sequentially.

Truckload tractors were down a little more than 6% sequentially and just about 1% from a year ago, suggesting a significant purge in equipment just in the July-to-September period.

In his comments this quarter in a prepared statement, Randolph Marten pointed to one quarterly positive: The third quarter was the first since the fourth quarter of 2022 during which the combined Truckload and Dedicated total rate per mile has increased from the prior quarter.

But the specific figure is not disclosed in the earnings.

What was not up sequentially was combined revenue for Truckload and Dedicated. The split on that in the third quarter was $108.4 million for Truckload and $75 million for Dedicated. The prior quarter, the split was $112.6 million and $81.3 million.

But the executive chairman also looked forward. Marten said there is “increased interest by our customers to secure dedicated capacity.”

And while some metrics in the earnings report suggested a carrier that has shrunk, Marten spoke of growth in the Dedicated segment at his namesake company. He said the company has new dedicated programs that have added 149 drivers to the Marten ranks, up from 133 a quarter earlier. The new Dedicated services are expected to be “substantially in service by the end of the year.”

Marten’s stock price reacted negatively to the earnings news. At approximately 10:45 a.m. EDT, when the S&P 500 had eked out a gain of about 0.25%, Marten’s stock was down roughly 2.75% to $16.23, a decline of 46 cents.

The 52-week low at Marten is $15.33, recorded April 19. Since then the price of Marten stock is up about 6.8%.

But in the past 52 weeks, Marten’s stock is down about 16.1% while the S&P 500 is up 35.6%.

Marten has company in other truckload stocks that have been lagging the broader market index. In the past 52 weeks, per Barchart, Heartland (NASDAQ: HTLD) is down 21.2% and Pam (NASDAQ: PTSI) is down 16.5%. But Werner (NASDAQ: WERN) is down just about 1% while Covenant Logistics (NYSE: CVLG) is up about 21.4%.

The 5-cent earnings per share figure at Marten is less than what the company pays out in quarterly dividends, which at present stands at 6 cents.

The 6-cent dividend has been in effect since the first quarter of 2022. Marten also paid a 50-cents-per-share special dividend in December 2020.

The past few years have taken a toll on Marten’s cash on hand. At the end of the third quarter of 2022, when the strong post-pandemic freight market was starting to recede, Marten had cash on hand of $71.4 million, up from the $57 million it had on hand at the close of 2021.

But in the latest earnings report, cash on hand was down to $42.9 million, after the company closed out 2023 at $52.2 million.

Total operating revenue at Marten for the quarter was $237.4 million, down from $280 million a year earlier. The nine-month revenue total was $733.4 million, down from $863.2 million in the first nine months of 2023.

Expenses did fall as well in the quarter, dropping to $233 million from $262.3 million a year earlier.

One reason for lower expenses: management salary reductions. Marten filed notice with the Securities and Exchange Commission last month that it was cutting salaries for six top managers.

More articles by John Kingston

Trucking and marijuana testing find their way to the Supreme Court

TriumphPay gets back to a positive EBITDA

AB5 notches another win: Supreme Court won’t hear Postmates/Uber case