With second-quarter earnings starting to roll in, one question will become paramount: What do they get compared to?

This is not just an issue in trucking. The issue that Wall Street analysts have is that the usual year-on-year comparisons will be against the second quarter of 2020, a three-month period of turmoil brought on by the pandemic.

By those standards, as well as almost any other benchmarks, Marten Transport (NASDAQ: MRTN) had a strong quarter. In a prepared statement announcing its earnings, Marten said the second quarter of 2021 recorded the highest operating revenue and operating income for any quarter in the company’s history, and that its operating ratio, net of fuel, was also a record since it became a publicly traded company in 1986.

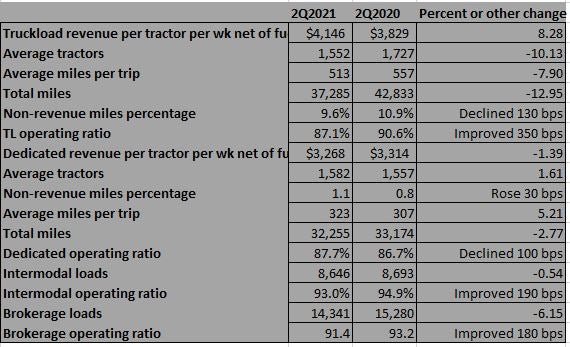

The comparisons against the second quarter of 2019 looked strong, though two years ago was not considered a particularly bang-up quarter. Marten’s truckload segment posted an OR of 86.2% in this year’s second quarter, an improvement of 110 basis points from last year but up 540 bps from two years ago (and 460 bps from three years ago, which was considered one of the strongest freight markets in recent history but is generally seen as having been eclipsed this year.)

Marten’s dedicated division had a second-quarter 2021 OR of 86.7%, which actually marked a deterioration of 190 bps from the prior year. But it was 180 bps stronger than two years ago.

Bringing in the ORs of the smaller brokerage and intermodal divisions led to a consolidated OR for Marten of 87.7%, up 30 bps from last year and an improvement of 290 bps from two years ago.

The strong performance came on a relatively modest increase in operating revenue from last year, up 9.4% to $232.4 million despite a far larger increase in average rate per mile since then. But it is that figure that Marten said was a company record for any quarter.

However, the operating revenue climb of 9.4% was aided by a significant boost in revenue from fuel. Operating revenue net of fuel surcharges was up just 5% from last year. But the bottom line is that even getting past the bump that higher fuel prices created in the overall operating revenue figure, net income for Marten was $21.4 million, up 18.1% from last year’s second quarter.

Costs and taxes were up modestly as well; salaries, wages and benefits rose just a small amount, to $75.3 million from $73.4 million. Insurance costs declined to $9.4 million from $11.6 million, purchased transportation climbed significantly to $45 million from $36.1 million, and the company’s gains on disposition of equipment was up slightly more than $3 million.

The end result was a rise in operating income of 12.8%, to a Marten record of $28.52 million from $25.26 million. Two years ago, operating income was just $19.9 million.

The improvement in the truckload segment came even as the company drove significantly fewer miles compared to last year, dropping 13% to 37.2 million miles from 42.8 million miles. But revenue per tractor per week climbed to $4,146 from $3,829 so that even though the mileage decline was significant, revenue for the truckload segment rose slightly to $95.94 million from $94.2 million.

In the dedicated sector, revenue per tractor per week dropped to $3,268 from $3,314, total miles dropped to 32.25 million from 33.17 million. But the average miles per trip rose to 323 from 307, and that helped revenue rise 6.2% to $80.12 million from $75.42 million.

Although the line item on salaries was up only slightly, signs of the driver squeeze could be seen in the big increase in purchased transportation, an indication Marten needed to turn to the independent owner-operator segment to move freight. The result of that squeeze will be higher costs for some customers, Marten said.

“We have been increasing and will continue to increase the compensation from our customers for our premium services within the constrained freight market largely caused by the unrelenting national shortage of qualified drivers,” Chairman Randolph Marten said in the company’s statement. “We are also heightening our emphasis on structurally improving our drivers’ jobs and work-life balance by collaborating with our customers.”

More articles by John Kingston

Latest package of New Jersey laws further targets independent contractor status

A first: Teamsters union reaches agreement on contract with XPO

Big push to restrict overnight parking in Minneapolis hits the brakes