Spot container freight indexes are still falling. Cargo shippers are signing annual contracts at sharply lower rates than last year. Import demand continues to be crippled by high inventories. A massive wave of new container ships is now hitting the market in full force.

And yet, the container shipping industry does not appear to be battening down the hatches for a looming storm. It is not behaving like an industry facing an imminent crisis.

The rates paid by liner companies to charter container ships bottomed out earlier this year and are now increasing. The duration of charters is rising as well.

The number of idle container ships has decreased in recent weeks. Liner companies continue to buy more vessels in the secondhand market.

The expected tsunami of ship recycling has yet to occur. The number of older ships demolished year to date is lower than expected. And container lines continue to place orders at shipyards for more vessels.

Charter rates rise off bottom

Even as liner companies “blank” (cancel) sailings in the face of weak transport demand, they continue to lease more vessels — and they’re doing so at rising charter rates.

The Harpex index, which measures global charter rates, has been inching back upward since early March.

According to Maritime Strategies International (MSI), spot freight rates are still eroding, while “in contrast, charter markets not only found a floor but also recorded slight upticks across different vessel size categories.” MSI said the “disconnect between the spot freight and the charter markets continued to widen in recent weeks.”

The nonoperating owners (NOOs) — the companies that charter ships to ocean carriers — “seem to have the edge over liner operators at this point, as demand for vessels remains firm and supply tight,” added MSI.

Alphaliner reported Tuesday that “charter rates are now rising markedly for all ship sizes” and “demand is strong across the board.” It acknowledged that charter market gains are “at odds with the current challenging environment, characterized by low spot freight rates on most routes and rising pressure on the supply side.”

During the 17th Annual Capital Link International Shipping Forum, held on March 20 in New York, George Youroukos, chairman of Global Ship Lease (NYSE: GSL), said, “If you forget about the last two supercycle years and go back to pre-COVID, charter rates are at very high levels today compared to normal territory.”

Clemens Toepfer, managing director of ship brokerage Toepfer Transport, said, “Container shipping has such a large orderbook that this is wishful thinking, but we are still in a very good market compared to pre-COVID and if we get through this at the rates we have now, container shipping will continue celebrating.”

Charter durations rise off bottom

Charter durations were extending out to three to five years at the peak of the container shipping boom. By early this year, they had contracted back to six months. Now, they’re increasing again. “A 12-month period is becoming the new normal,” said brokerage Braemar.

Some deals are now being done for two years or more. Braemar reported that ONE chartered the 6,350-twenty-foot-equivalent-unit Brighton starting in May for 23-25 months at $32,500 per day (the same charter rate as a 6,500-TEU ship obtained for half that duration in January).

Alphaliner cited “the return of long periods” and pointed to a 2,345-TEU vessel that was just chartered for 36-40 months.

Capital Product Partners (NASDAQ: CPLP) chartered out its 9,288-TEU Akadimos starting this month for 24-26 months at $47,250 per day.

Euroseas (NASDAQ: ESEA) disclosed Wednesday that it chartered out its 4,253-TEU Synergy Keelung for 24-26 months at $23,000 per day.

“We believe that both the rate and — especially — the duration of the charter are indicative of the resilience of the container-ship market, which has firmed up after the adjustment that took place over the last six months,” said Euroseas CEO Aristides Pittas.

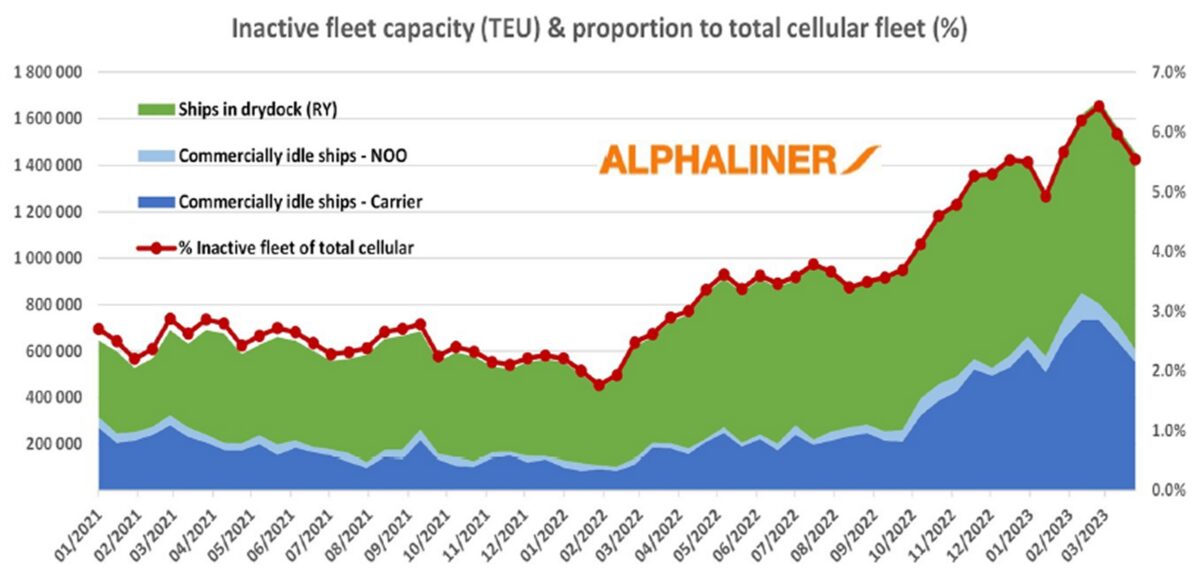

Commercially idle capacity falls back

Analysts expect the onslaught of newbuildings together with continued weak transit demand will lead to more commercially inactive ships as owners and operators temporarily idle their tonnage.

According to Alphaliner data, the percentage of inactive ships sank to historically low levels of 1.8% at the height of the boom in late January 2022. It rose thereafter, peaking at 6.4% in late February, following the predicted script.

However, inactive tonnage has actually decreased since then. As of late March, it was down to 5.5%.

Of that total, 58% were inactive because vessels were in shipyards, with only 42% commercially idle.

The amount of commercially idle tonnage peaked in mid-February at 850,417 TEUs. As of late March, Alphaliner data showed commercially idle tonnage was down to 606,943 TEUs. That’s a six-week drop of 242,474 TEUs or 29%.

S&P activity bounces off floor

Toepfer said that there was “massive activity at very, very high prices” during the boom in the container-ship sale and purchase (S&P) market. That evaporated when the boom ended, but it has since picked up again from the floor.

“A lot of people who were scared of buying into the falling knife are coming to the market,” he said. “It’s very, very active right now.”

There are several categories of buyers. One is the larger liner companies, two in particular. According to Alphaliner, “The secondhand market has generated a multitude of deals lately, with MSC and CMA CGM being the most active buyers.”

MSC has purchased over 300 secondhand ships since mid-2000. CMA CGM has bought over 100. “This high activity, and the fact that fewer vessels are hitting the S&P market due to the increasingly remunerative charter market, is pushing prices up, and this trend is unlikely to reverse in the short term,” said Alphaliner.

Toepfer pointed to two other drivers of purchasing in smaller size categories.

Virtually all of the major liners ceased serving Russian ports, with the notable exception of MSC. Toepfer said that “about half of the purchasing interest for container ships is backed by trade into Russia — buyers from Turkey, Dubai and China who are actively looking into that area.”

Another buying source is “the people who have around $10 million to spend who were not even able to buy a small 20-year-old ship at that price during the boom. Now, for $10 million, they can get a decent ship,” said Toepfer.

Demolitions remain low

One of the narratives going into the downturn was that older ships were not scrapped during the boom because they could earn exorbitant returns despite their age, but with freight rates and charter rates now far below their highs, those vessels would go to demolition yards. This would reduce supply pressures from arriving newbuildings.

In October, shipping consultancy Drewry laid out a base-case scenario in which 600,000 TEUs of capacity would be scrapped this year. That would be the second-highest level of scrapping since 2016, when Hanjin went bankrupt.

Alphaliner projected in January demolitions would “skyrocket” this year to 350,000 TEUs. Ocean carrier Hapag-Lloyd projected during its latest earnings presentation on March 2 that 900,000 TEUs would be scrapped in 2023.

Scrapping year to date has been at nowhere near the pace needed to reach those goals. According to MSI, only 19,800 TEUs of capacity was scrapped in Q1 2023.

“Scrapping has not picked up as much as initially expected, with only liners having sent ships for demolition in 2023 up until today,” said MSI. “In contrast, NOOs see no incentive to scrap even their oldest ships yet, so long as charter rates remain firmly above their pre-pandemic levels.”

It’s not just the charter market that’s keeping container ships from the breakers. It’s also the S&P market.

Star Asia Shipbroking reported this week: “Cold water was poured on recent hopes of recyclers when Wan Hai’s 25-year-old Wan Hai 282 was sold for further trading. This is a classic example of the demand for elderly container ships from Far Eastern buyers.”

Alphaliner reported that MSC just bought Evergreen’s 1999-built, 5,300-TEU Ever Liberty and Ever Uniform, ships “that were expected to be sold for demolition given their age.”

Newbuilding orders keep coming

Lower-than-expected scrapping is coinciding with the debuts of newbuildings ordered during the boom. In recent months, the container ship orderbook reached an all-time high in terms of TEUs scheduled for delivery.

The new ships began hitting the water in earnest last month. According to Alphaliner, 24 container vessels with aggregate capacity of 188,000 TEUs were delivered in March, making it “among the strongest delivery months of all time.”

The newbuilding market — as with the charter and S&P markets — is defying expectations and not following the script. It was widely assumed that fresh orders would cease in the wake of plunging freight rates. But liner companies are still ordering, driven by demand for dual-fuel vessels.

“Contracting picked up pace again in February, with 312,000 TEUs of new orders, most for methanol-powered vessels and the rest for LNG-powered units,” said MSI.

The ordering continues. China’s Cosco ordered four methanol-powered 16,000-TEU newbuildings last week. More contracts appear imminent.

According to Alphaliner, “Brokerage sources claim that both CMA CGM and Hapag-Lloyd are interested in methanol-powered vessels of around 4,000 TEUs.” CMA CGM is reportedly looking at 10 newbuilds and Hapag-Lloyd at six.

Liners and owners have huge cash cushions

Both carriers and NOOs have gone into the cyclical downturn with huge cash reserves amassed during the boom, which will cushion the fallout from excess ship capacity.

Zim (NYSE: ZIM) had $4.6 billion in cash as of the end of last year. Hapag-Lloyd had liquidity of $17 billion, up from $1.2 billion at the end of 2019. Maersk’s liquidity was $28 billion at the end of 2022.

Jefferies analyst Omar Nokta told the Capital Link forum, “It’s very easy for us to look at the orderbook and think, ‘Wow, this sector is gone for a long time,’ but this is one of the very rare times in history when a downturn has come and people have foreseen it coming.

“Usually, downturns in cyclical industries, and definitely in shipping, come unexpectedly. We’re all surprised and companies are stuck with stretched balance sheets. Here, when we look at the container sector, liners are all flush with cash. Their leverage ratios are historically low.

“The shipowners themselves [NOOs] are also well prepared. They’ve got deep [charter] backlogs and strong balance sheets. So, I feel there’s a better future for container shipping than people think if they just look at freight rates and the orderbook. When you have companies in a sector that are very strong financially, it’s a much better outlook.”

According to Toepfer, “Container shipping didn’t leave many people ‘naked’ with the drop. They’re not so exposed. Basically, everybody had a good party and everybody had a good drink and everybody is sitting there and maybe they’re still drunk but they’re smiling.”

Click for more articles by Greg Miller

Related articles:

- Mighty fall: Container line profits plummet from historic peak

- How much will container lines ‘earn’ in 2023? It depends on the metric

- Zim Q4 results surprise to upside but 2023 ‘extremely challenging’

- Container shipping market yet to bottom as spot rates keep slipping

- ‘Colossal’ tidal wave of new container ships about to strike

- Container lines still chartering ships despite drop in cargo demand

- Container trade’s next turn: Price wars, cheap contracts, new ships

- Maersk: Container shipping contract rates will sink to spot levels