The ocean carrier cocktail is back and it packs a punch. Two parts canceled sailings that spice up spot rates, coupled with a stiff pour of general rate increases, leaves shippers with a dull headache and a thinner wallet.

While this iteration of the cocktail is not as strong as previous ones, it is potent enough to sour shippers’ stomachs. With no end in sight to the Red Sea diversions and “meh” consumer demand, ocean carriers are in lockstep with their mission of trying to establish an artificial floor to stave off rate erosion and add some girth to their wallets.

Peter Sand, chief shipping analyst at Xeneta, says the market right now contains equal shares of “desperateness, defying gravity and frontloading.”

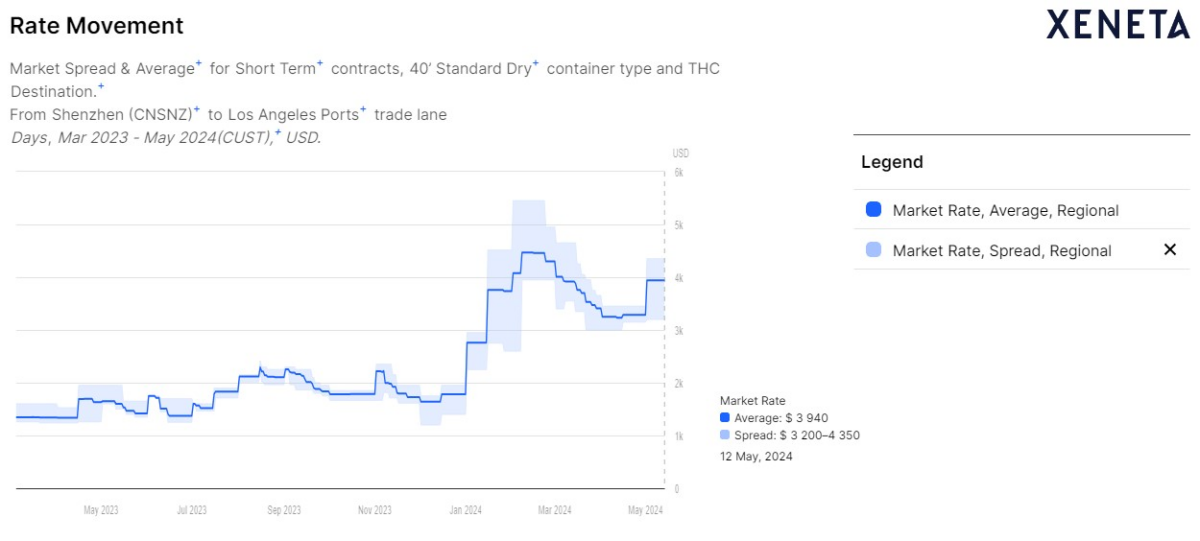

“As per desperateness: Xeneta data shows that the spot market average on key trades like Shanghai-Rotterdam, Ningbo-New York/New Jersey and Shenzhen-Los Angeles ports is going up, almost exclusively because the shippers who are paying more than the average (our Market High) are now paying much more ($900 per FEU) — whereas the larger, non-desperate shippers are only paying a little bit more ($50 in May) than what they did in the second half of April,” explained Sand.

While some shippers American Shipper has spoken with are not happy with the latest round of general rate increases per 40-foot container, Sand says compared to prior years, GRIs in 2024 are not coming at a faster rate.

“Carriers push for GRI to stick every fortnight — during severe downturn, they often avoid the mid-month push, but when the market is ‘ripe,’ like right now — they push as often as they can. Not only GRI to lift base rates, but also lifting ‘Peak Season surcharge’ or other surcharges,” said Sand.

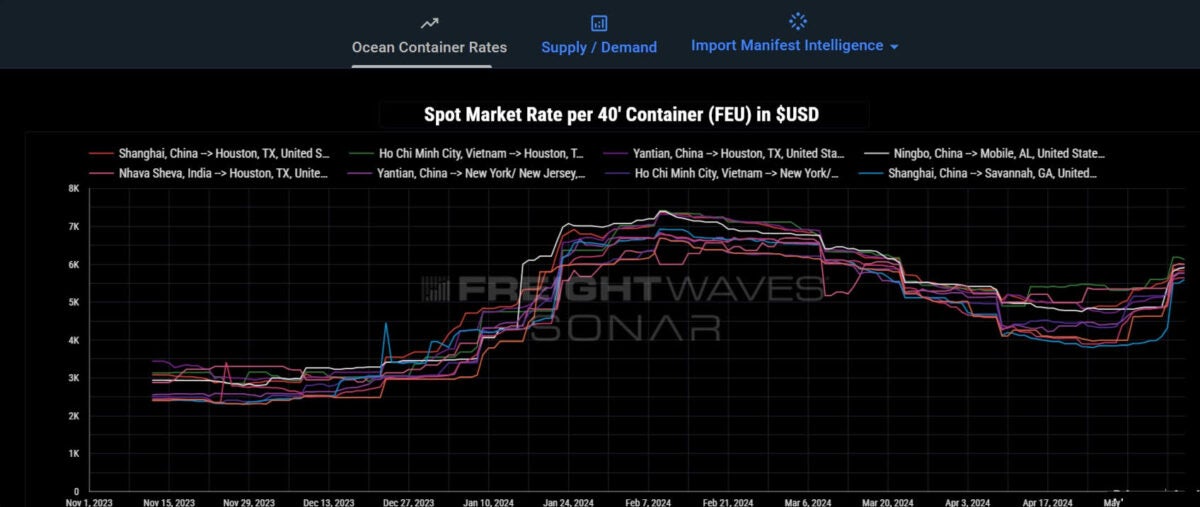

Blank sailings, the major component of this cocktail, are increasing after ocean carriers gorged on higher Red Sea rates while they could with the added capacity. But the window to capitalize on this was short-lived, and spot rates started to drop because of the decrease in freight orders. Spot rates are now rising back as capacity is being cut.

Antonella Teodoro, senior consultant at MDS Transmodal, tells American Shipper it would appear that there are changes in level of capacity offered on the Gulf and Indian subcontinent and Far East trade lanes, as well as on the trans-Atlantic.

Capacity offered on the Europe and Mediterranean-North America route is estimated to contract by more than 13% in the second quarter of 2024 compared with the same quarter last year. The Red Sea crisis diversion and the capacity shuffle as a result on the routes could be the factor to to which this contraction is attributed.

“The globalized nature of the container shipping industry means that local disruptions can be felt globally,” said Teodoro. “We have seen [this] during the peak of congestion experienced by the North American ports a few years ago and we are experiencing this now as well. Differently from 2020-2021, shipping lines now have more capacity at their disposal. However, adjustment in capacity allocation is still required to deal with the re-routing via the Cape of Good Hope. For North America, the trade lane that appears to be suffering is the North America — Europe & Med, expected to see a contraction of more than 13% in 2024Q2 vs 2023Q2.”

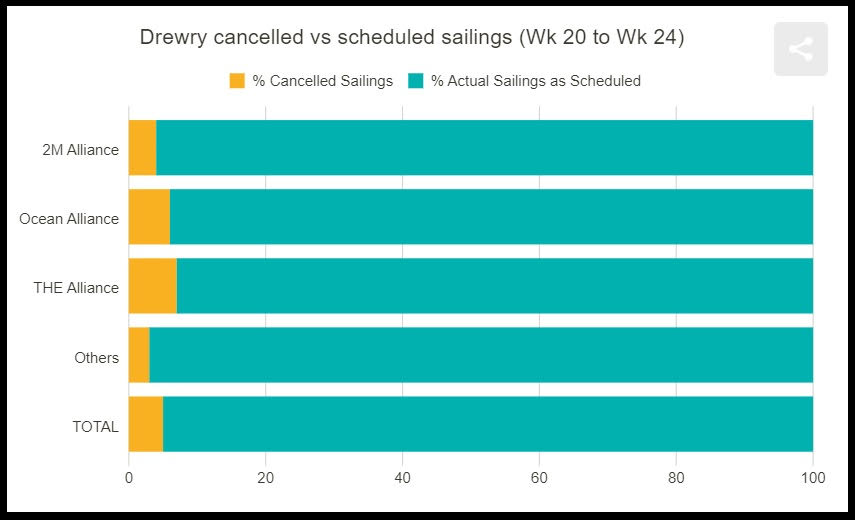

According to Drewry, the alliances have canceled 5% of sailings between week 20 (May 13-19) and week 24 (June 10-16). That’s 32 canceled sailings of 653 scheduled. The biggest loser is the Eastbound route on the trans-Pacific, with 53% of the cancellations. Trans-Atlantic Westbound is down 22%, and Asia to North Europe was slashed by 25%. Leading the charge is THE Alliance followed by the Ocean Alliance.

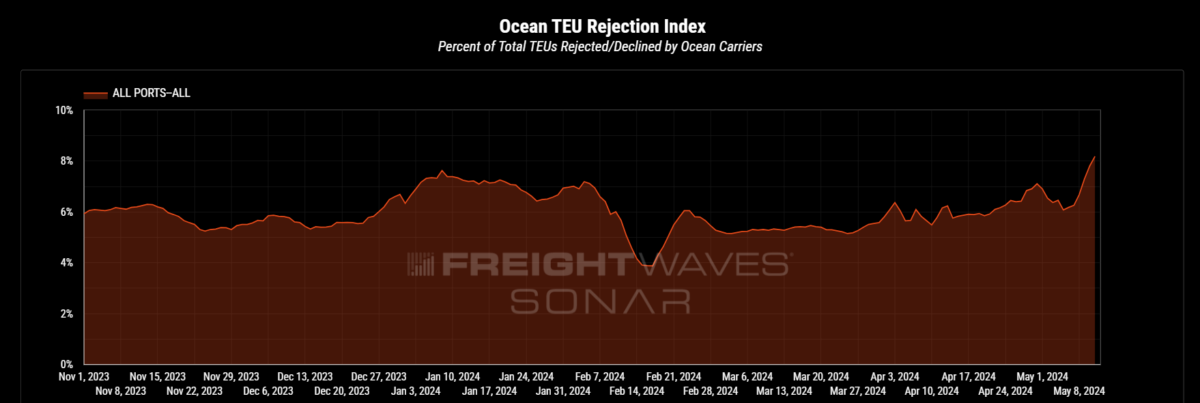

As a result, rejections are up.

Sand tells American Shipper that measuring blank sailing and supply-side action/manipulation from the carriers’ side can be done many different ways. The first is by reviewing the blanked vessels versus deployed: Sand said the data is measured by weekly departures in Asia and doesn’t take into account how many ships are needed to perform that service. For Asia-Med and Asia-North Europe, that would be a massively higher amount.

Another gauge given by Sand is the amount of capacity blanked due to Chinese Lunar New Year in 2023 versus 2024. In 2023, 663.705 TEUs was blanked; in 2024 326.430 TEUs was canceled.

Alan Murphy, CEO, Sea-Intelligence, tells American Shipper it would indicate that carriers are blanking at a ratio in line with demand, whether increasing or decreasing.

“If anything, we are seeing less blanked sailings in a market with decreasing demand, which would normally indicate a risk of over-capacity,” said Murphy. “However, with the disturbances going on in the Middle East (and the Red Sea in particular), this over-capacity is being absorbed by the need to sail around South Africa for the Asia-EUR services. The real issue may therefore only arise the day that circumstances will normalize in the Red Sea, and the (over)capacity currently used for the routing around South Africa will be released back into the open market, unless the demand will start increasing again.”

Sand did warn that he cannot rule out a larger storm brewing.

“It seems to me that shippers have made a lot of effort to avoid just that,” said Sand. “Still Xeneta expects spot rates on key trades to jump again by mid-May, as carriers have pushed hard to get GRI to stick — successfully at the start of May (in the eyes of the carriers) — giving them appetite for another push. That brings me to ‘defying gravity’ — as something that can’t be done forever. But whereas the spot rates peaked in mid-Jan on main Europe-bound trades and early-Feb on main North America bound trades, they have been falling gradually ever since — until April was fairly flat, and May now sees rising rates.”

But when reviewing growth rates for Q1 2024 versus last year, Sand stresses that Q1 of 2023 was “poor” so when compared to 2024, the numbers will be inflated.

“We need to remember the eurozone have only left recession behind in Q1-24,” said Sand. “The point I want to make is that shippers have moved much more cargo in the first 4 months of the year, because they want to avoid a potential squeeze in Q3, when those shippers that left the restocking or overstocking of inventory too late could get squashed IF demand should exceed that of deployed capacity.”

So grab some baby aspirin and drink lots of water. Shippers could be in for some hangovers. Perspective and a clear head will be needed as the rest of the year shakes out.