Freight rates and shipping charter rates are on the upswing in certain segments of the ocean transport market. For ship owners who have suffered through years at break-even or below, it’s a welcome reprieve, for however long it lasts.

In the spotlight this week are larger bulk carriers carrying iron ore from Brazil to China, container ships bringing Chinese goods to California, and gas carriers transporting propane from the U.S. Gulf and Middle East to Asia.

Capesize resurrection

Rates appear to be recovering in earnest for Capesize bulkers. These vessels have a carrying capacity of 100,000 deadweight tons (DWT) or more, generally around 180,000 DWT. They are the workhorses for the carriage of the so-called ‘major bulks’ – iron ore and coal.

Capesize rates sank to near all-time lows of under $4,000 per day in the first quarter of 2019 in the wake of the mining dam accident in Brazil, which curbed iron-ore exports to China from Brazilian mining giant Vale.

According to Amit Mehrotra, shipping analyst at Deutsche Bank, “Capesize spot rates have rallied significantly over the last two months, quicker than expected. Capes are current earning about $14,000 per day in the spot market.”

He noted that “while the market did not expect a meaningful Cape recovery until the second half,” there is now reason for “optimism for continued Cape strength.” Specifically, Vale’s export volumes have sharply increased in May and early June, averaging around 5 million tons per week, up from 2.7 million tons per week in April, as weather issues affecting Vale’s northern production system have alleviated.

According to Frode Mørkedal, shipping analyst at Clarksons Platou Securities, “Bulk rates are now largely in line with what they were before Vale’s dam breach on January 25. The FFA [forward freight agreement] market is pricing Capesize third-quarter and fourth-quarter contracts at year-highs in the $16,500-18,500 per day range – higher than prior to the Vale disaster.”

Mørkedal acknowledged, however, that Wall Street investors are not convinced. “There is a large disconnect between sentiment in the shipping market, and sentiment among investors. Dry bulk stocks continue to trade down,” he noted.

“What [investors] may not realize is that Brazilian iron-ore volumes are normalizing, while shipping fundamentals are looking strong. We believe the markets are past the worst and that dry bulk companies should see a significant increase in earnings [starting in] the third quarter.”

Public companies with spot Capesize exposure: Star Bulk (NASDAQ: SBLK), Golden Ocean (NASDAQ: GOGL), Safe Bulkers (NYSE: SB), Seanergy (NASDAQ: SHIP)

Container shipping’s bounce

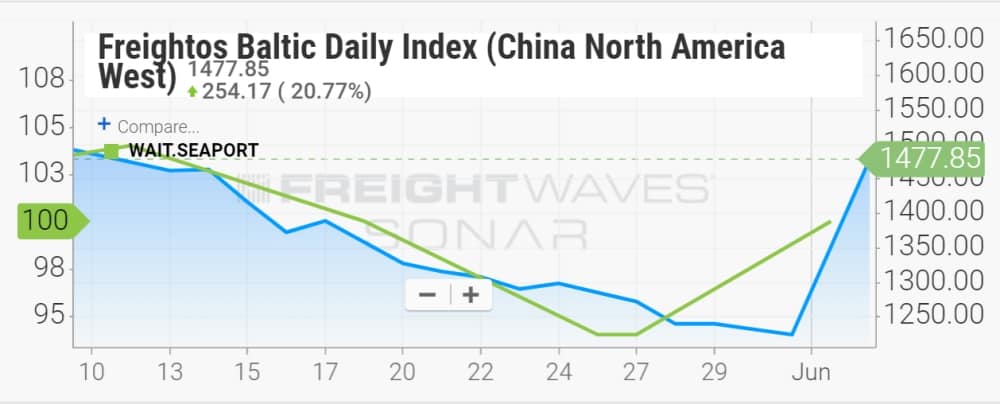

As previously reported by FreightWaves, the Freightos Baltic Daily Index (China-North America West) – which tracks the cost to ship containers on the trans-Pacific route – appears to be behaving as a proxy for cargo demand.

This Freightos index has been strongly correlated with the WAIT.SEAPORT index, a proprietary index on FreightWaves’ SONAR data platform that measures the weekly average waiting times for trucks at U.S. ports. Port properties are geotagged and trucks’ locational devices are used to determine average wait times. If the Freightos trans-Pacific rates index was not being driven by cargo demand, it is unlikely that it would correlate so closely with WAIT.SEAPORT.

These two indexes have been falling in unison through 2019, with declines escalating throughout the month of May, since U.S. President Donald Trump made remarks indicating that more tariffs on Chinese goods could be levied.

But now, something is changing. As the latest data indicates, the Freightos Baltic Daily Index (China-North America West) has started to rise. And the correlation with WAIT.SEAPORT continues to hold. It is now also on the upswing.

Could this be the first glimmer of a repeat of the second half of 2018? In that period, U.S. importers rushed to bring in goods from China before tariffs hit. Could the latest index moves be the consequence of U.S. importers moving to beat the next round of tariffs? Is it happening only now, in early June, because it took time to set supply chains motion? Time will tell whether this is a ‘dead cat bounce’ or something more.

Public shipping companies with exposure to spot box shipping rates: Maersk, Hapag-Lloyd, Matson (NYSE: MATX)

Editor’s note: Freightos has a business agreement with FreightWaves that includes editorial coverage.

VLGC rates getting ‘heady’

After a multi-year stretch of painful losses, one sub-category of the liquefied petroleum gas (LPG) segment is finally starting to throw off cash in a major way.

Rates for very large gas carriers (VLGCs), which have a capacity of around 82,000 cubic meters, are hitting new highs. VLGCs focus on the long-haul transport of LPG – primarily propane and secondarily butane – from the U.S. Gulf to Asia, and from the Middle East to Asia.

According to Clarksons Platou Securities, VLGC spot rates between the Middle East and Japan reached $51,300 per day as of June 4, up 12 percent week-on-week and up 21 percent month-on-month. Rates year-to-date are averaging $25,700 per day, compared to just $12,000 per day over the same period last year.

Mørkedal at Clarksons said that current returns for VLGC owners “are close to the highest level since the heady days of 2014-15, and the U.S. [to Asia route] continues to trade at a premium.”

“Recent weeks have shown a majority of spot fixtures concluded with owners, rather than with charterers re-letting tonnage,” he said, referring to charterers leasing from owners and then rechartering to pocket the spread. “This poses the longer-term question as to whether the VLGC market is finally beginning to balance out after a couple of tough years for owners.”

He explained, “With limited re-lets, it is reasonable to question whether charterers are perhaps not as long on tonnage, leading to a spot market more dominated by owners, and a general firming in rates.” In other words, according to this theory, the more owners are directly involved in the charter negotiations, as opposed to middle men ‘trading’ on rates, the stronger the market could be.

While the stock price of a VLGC-centric company like Dorian LPG (NYSE: LGP) is up since March, it’s clear that equity investors have yet to jump on the VLGC bandwagon. Dorian’s stock is still relatively flat year-on-year, despite the dramatic surge in rates over that stretch.

Public companies with spot VLGC exposure: Dorian LPG (NYSE: LPG), BW Gas (Oslo: GAS)