The good news is that the Baltic Dry Index (BDI), which tracks bulker charter rates, recently hit its highest point since late July 2018, and the stocks of several publicly listed bulker owners are up 30 to 50 percent since June 1.

The not-so-good news is that the July 2018 BDI level was well below the peaks seen in 2014 and 2011, and dry bulk stocks are up off an extremely low base and are still trading under the companies’ net asset value (market-adjusted assets minus liabilities).

Regardless of these caveats, there is no denying that rates in dry bulk have shown promising strength in recent days and weeks. Meanwhile, tanker rates are pulling back after recent surges, and container freight rates continue to inch up as the industry heads into the third-quarter peak season.

Bulkers continue to impress

According to Clarksons Platou Securities, rates for Capesize bulkers – vessels with capacity of 100,000 deadweight tons (DWT) or more – reached $26,400 per day on July 9, up 25 percent week-on-week and 76 percent month-on-month. Rates for Panamaxes (65,000-90,000 DWT) were $15,200 per day, up 22 percent week-on-week and 33 percent month-on-month.

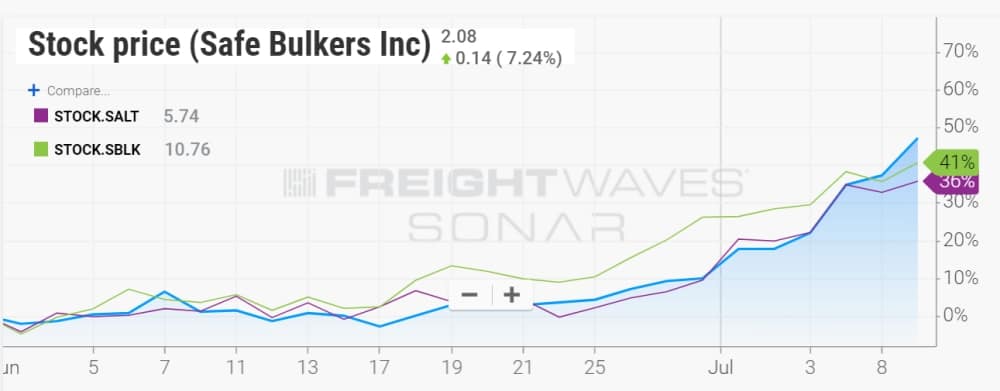

The reasons behind the upturn were discussed in a Capital Link webinar on July 9 featured top executives from Safe Bulkers, Star Bulk and Scorpio Bulkers. Since June 1, the stock prices of these three companies have risen 47 percent, 41 percent and 36 percent respectively.

The first reason for rate strength is, as usual, China. “China may look weaker in some sectors but not in steel production, which is up 10 percent in the first half and that is what drives iron-ore imports,” said Hamish Norton, president of Star Bulk.

He believes the Chinese government will enact a stimulus program to counteract any negative impact of U.S. tariffs “and their fiscal stimulus has almost always involved subsidized steel production for infrastructure and real estate – so there should be no shortage of demand from China.” Scorpio Bulkers president Robert Bugbee added, “We are certainly not seeing China fall apart.”

The next reason for rate improvements involves the Brazil-to-China iron-ore trade. Because this route is three times as long as the voyage from Australia to China, it soaks up three times the ship capacity. Vessels carrying Brazilian ore are dominated by Capesize bulkers and larger ships known as Valemaxes or very large ore carriers (VLOCs), which have a capacity of up to 400,000 DWT. VLOCs are largely under the commercial control of Brazilian iron-ore producer Vale (NYSE: VALE) through multi-year contracts.

Vale’s Brucutu mine, which produces 30 million tons per year of iron ore, went offline in January after the deadly collapse of a tailings dam, and reopened in late June. While Brucutu was offline, China drew down its iron-ore stockpiles, which will now need replenishing.

According to Norton, Capesize operators were afraid to ballast (sail empty) toward Brazil because of the Brucutu mine closure, “so there is a significant shortage of Capes in the Atlantic Basin, and all of the VLOCs controlled by Vale have already been loaded up and are laden and heading east.”

This “almost guarantees high Capesize rates for the next 50 days,” he maintained. In other words, it will take 50 days’ sailing time for enough Capesizes to ballast their way to Brazil and bring down rates.

The next reason for dry bulk strength involves the consequence of the Capesize shortage in the Atlantic Basin for smaller vessel classes. When Capesizes are not available, shippers will split bulk cargo lots in half and employ two smaller ships instead, such as Panamaxes and post-Panamaxes (90,000-100,000 DWT).

According to Polys Hajioannou, chief executive officer of Safe Bulkers, “Smaller sizes are starting to benefit from the lack of Capesizes in the Atlantic. We are seeing post-Panamaxes in the Mediterranean achieving rates of $26,000 to $27,000 a day from the Black Sea to the Far East. Those would normally be Capesize cargoes but they are being split down the middle.”

Yet another positive, added Hajioannou, is strength in the transport of coal, a commodity carried by both Capesizes and Panamaxes. “The majority of what we carry is coal and grain and we see a lot of coal going to Vietnam and the Philippines, as well as to Japan, and India has been doing very well – there were some big movements of coal to India in the past two to three months, before the monsoon season.”

Finally, preparations for IMO 2020, the global cap on the sulfur content of marine fuel and emissions starting January 1, 2020, are providing further support for rates, as owners pull bulkers from service to install emissions scrubbers, temporarily removing vessel capacity from the market.

Public companies with spot Capesize and Panamax spot exposure: Genco Shipping & Trading (NYSE: GNK), Golden Ocean (NASDAQ: GOGL), Scorpio Bulkers (NYSE: SALT), Star Bulk (NASDAQ: SBLK), Safe Bulkers (NYSE: SB), Seanergy (NASDAQ: SHIP)

Tankers take a step back

Tanker rates have recently received a boost from external events. Rates for very large crude carriers (VLCCs), which have the capacity to carry two million barrels of crude oil each, surged as a result of June 13 tanker attacks in the Gulf of Oman and resultant geopolitical tensions.

Medium-range (MR) product-tanker rates rose when the largest refinery on the U.S. East Coast, Philadelphia Energy Solutions, suffered a cataclysmic explosion and fire on June 23. MR tankers (comprised of MR1 and MR2 categories) have capacity of 25,000-54,999 DWT.

Over the past week, however, both VLCCs and MRs have given back some of their gains. According to Clarksons Platou Securities, VLCC rates as of July 9 were $18,300 per day, down 9 percent week-on-week, although still up 22 percent versus the same day last month. MR product tanker rates were $14,100 per day, down 11.5 percent week-on-week, but still up 16 percent month-on-month.

Regarding weaker VLCC rates, Deutsche Bank transportation analyst Amit Mehrotra commented, “Despite escalating tensions in the Middle East, crude tanker spot markets took a step back last week following strong gains. While we continue to observe a tight supply picture in the [Arabian] Gulf, with some ship owners avoiding the region, limited demand out of the Middle East pushed the market lower.”

On the drop in product-tanker rates, Mehrotra said, “We would have expected a firmer product-tanker spot market last week” but “spring refinery maintenance schedules may be turning around slower than previously expected.” One a positive note, he said that “product-tanker spot markets continue to soften,” but “time-charter rates are making new highs, which we view to be a better indicator of market health and fundamentals.”

Public companies with spot VLCC exposure: Euronav (NYSE: EURN), DHT (NYSE: DHT), Frontline (NYSE: FRO), International Seaways (NYSE: INSW). Public companies with spot MR product-tanker exposure: Scorpio Tankers (NYSE: STNG), Ardmore Tankers (NYSE: ASC), International Seaways (NYSE: INSW), Torm Tankers (NASDAQ: TRMD).

Container rates slowly rising

With tariffs and politics looming in the background, the China-US container trade is picking up pace in July following its stumble in May.

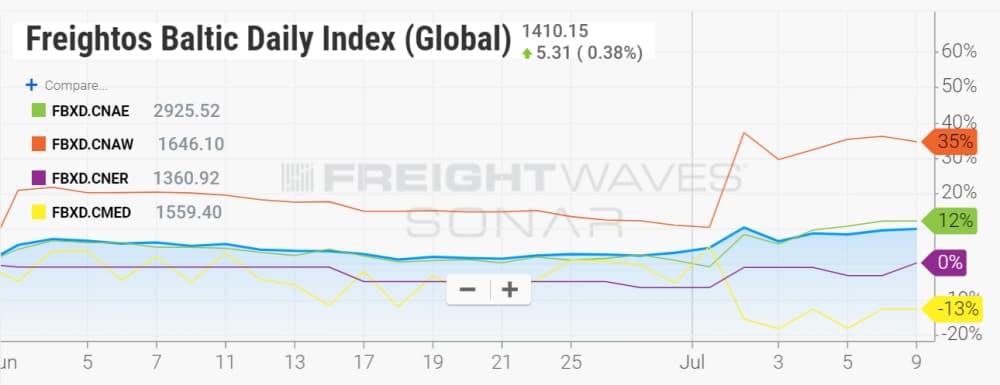

Since June 1, the Freightos Baltic Daily Index (Global), which tracks the price to ship 40-foot containers worldwide, is up 11 percent. Eastbound trans-Pacific demand appears to be a key driver.

Rates from China to the North America West Coast (FBXD.CNAW) are up 35 percent since June 1, and rates for shipments from China to the North America East Coast (FBXD.CNAE) via the Panama Canal are up 12 percent.

U.S. demand-driven gains are being counterbalanced by weaker rates elsewhere. The rates for shipments from China and North Europe (FBXD.CNER) are flat since June 1, although they are up in July. Rates for cargoes from China to the Mediterranean (FBXD.CMED) are down 13 percent, which much of that slide occurring this month.

Public shipping companies with exposure to spot box shipping rates: Maersk Line (Copenhagen: MAERB.C.IX), Hapag-Lloyd (Frankfurt: HLAG.D.IX), Matson (NYSE: MATX)

Editor’s note: Freightos has a business agreement with FreightWaves that includes editorial coverage.