This morning, FTR released its preliminary figures for North American Class 8 truck orders during the month of June. Fleets ordered 41,800 trucks last month, the busiest June ever recorded and 140% above June 2017. North American Class 8 orders have now exceeded 40,000 power units in four of the six months of 2018 so far.

June is normally a weak month for new truck orders, but 2018 continues to break all the old rules. January and February were unexpectedly hot months for freight markets, and carriers are loading up on new trucks in June: up is down, and down is up.

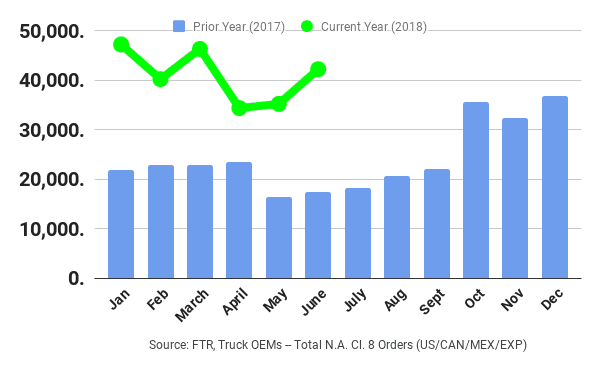

The chart below compares monthly truck orders in 2018 to the previous year:

Stock prices of several truck manufacturers jumped on the news. PACCAR (NASDAQ: PCAR), which builds Kenworths, Peterbilts, Leyland Trucks, and DAF trucks, has had a difficult month on the stock market but was up .8% on the day; Navistar (NYSE: NAV) climbed 2.61%; Daimler AG (ETR: DAI) posted a solid day, rising 3.76%, and Volvo (CPH: VOLV-B) was up 2%.

“There is an enormous demand for trucks due to burgeoning freight growth and extremely tight industry capacity,” said Don Ake, FTR VP of commercial vehicles, in a press release. “However, supply is severely constrained because OEM suppliers cannot provide the needed parts and components required to build more trucks fast enough. This bottleneck is causing fleets to get more orders in the backlog in hopes of getting more trucks as soon as they are available.”

“We’re expecting in June that the backlog will rise to a level we haven’t seen since about 1999,” Kenny Vieth, president of Columbus, Ind.-based ACT, told the Wall Street Journal. Vieth went on to say that most trucks ordered last month won’t be delivered until the first half of 2019.

FTR said that because of component shortages, OEMs are not able to keep up with demand for new trucks, and their backlogs are growing, causing more carriers to place orders to secure their spot in line. We do think that favorable rate environments and the Trump tax cuts have put more cash into carriers’ hands, allowing them to accelerate their fleet replacement, but there are reasons to think that, industry-wide, capacity is growing. The average price for three year old trucks (SONAR code: ut3.usa) has been strengthening all year: after a lull in January at $56,310, the average price climbed to $59,150 for February, $62,331 in March, $62,620 in April, and held steady in May at $62,654, the last month we have used truck price data for.

The chart below tracks used truck prices for three year old models since 2009:

The Cass Freight Index – Expenditures (SONAR code: cfie.usa) is also at an all-time high, indicating both healthy economic growth and inflationary pressures on transport and logistics costs. The Cass Freight Index uses January 1990 as its base month—so the Cass Freight Index – Expenditures for January 1990 would be 1.0. In May, that number was 2.88, and has been climbing since its bottom at 2.27 in January 2017. The overall volume of shipments, measured by the Cass Freight Index – Shipments (SONAR code: cfis.usa) was at 1.31 for May, well above 2017’s high at 1.17, 2016’s high at 1.11, and 2015’s high at 1.16.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.