As the second quarter 2019 earnings season approaches, the negative data and commentary centered on the lack of a seasonal increase in demand is forcing analysts to meaningfully lower earnings estimates and their outlook for the sector.

In a note out to clients on June 18, UBS analyst Tom Wadewitz lowered 2019 and 2020 earnings estimates for the truckload (TL) and intermodal companies he covers. Additionally, he lowered his investment ratings on J.B. Hunt (NASDAQ: JBHT) and Schneider National, Inc. (NYSE: SNDR) to “neutral” from “buy.”

In explaining the rationale for lowering estimates in 2019 and 2020, Wadewitz wrote, “The reductions are driven by our expectation that weakness in truckload and intermodal freight is likely to continue through 2019, and potentially into first-half 2020, and we expect a low-single digit decline in TL contract rates in 2020.”

The note highlighted expectations for a 3 percent decline in truckload pricing in 2019 and a 16 percent decline in operating income in 2020. The note cited outcomes in past downturns as a basis for cutting earnings estimates by 7 percent on average in 2019 and 17 percent in 2020.

Recent Trends

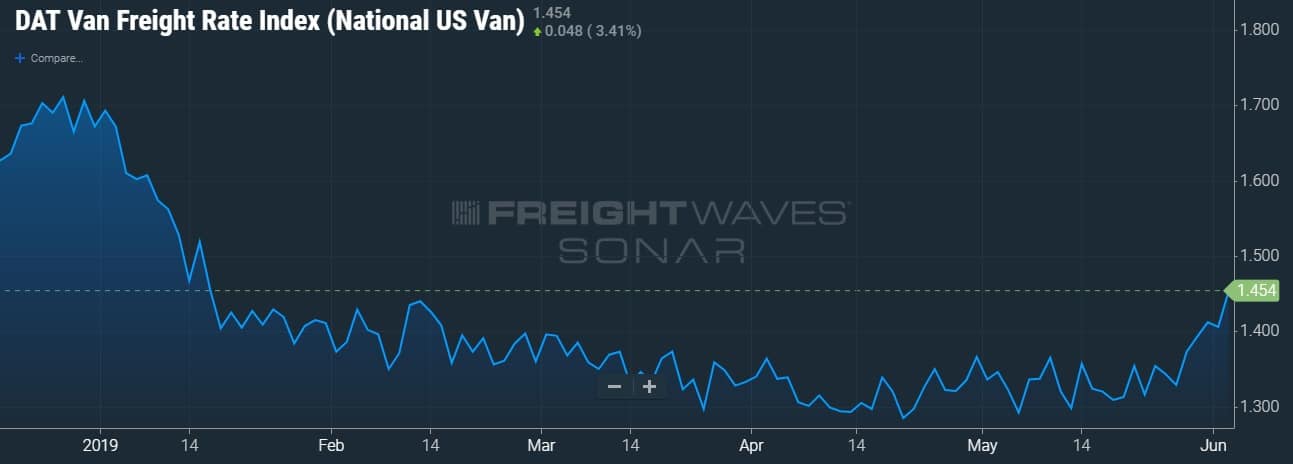

Truckload volumes have been soft for the bulk of the year. At recent investor conferences, management teams from different trucking companies bemoaned the lack of a normal seasonal uptick in freight demand. No carrier called out a specific geography or industry as particularly weak, instead noting a general demand malaise which was resulting in lower volumes (as highlighted in the decline in the outbound tender reject index below). Additionally, trade tensions and weather (cooler temperatures, flooding, etc.) were called out as negative factors.

Further complicating matters, the industry saw a run-up in fleet additions in 2018 when supply struggled to keep pace with demand. Many carriers used increased cashflows from strong volumes and surging spot market rates to add horsepower to their fleets. Since then, the market has flipped.

Volumes are lower on a year-over-year comparison (below 2017 levels in some instances) and spot pricing has moved meaningfully lower. While contractual pricing negotiations with the larger carriers and their shipper customer base may have had a favorable year-over-year comparison in the second quarter of 2019 (as compared to rates negotiated in the second quarter of 2018 – just before a precipitous increase in spot rates), FreightWaves reporters and analysts have heard from some carriers that they are renewing contracts at flat levels and even lower with some customers.

Landstar sees weakness in TL spot market, downplays Uber-Amazon impact on brokerage

With lower truckload volumes, weaker spot market pricing and relatively stable diesel fuel prices, intermodal volumes remain depressed compared to 2018. In the week ending June 8, 2019, intermodal containers and trailers were down 8 percent year-over-year according to the Association of American Railroads. For the month of May, intermodal traffic was down 5.9 percent compared to May 2018 and down 2.7 percent year-to-date compared to the same period in 2018.

While truckload management teams spoke openly of demand weakness at investor conferences in early June, none have officially lowered their earnings expectations. At the time, most were holding out for seasonal improvement in June, which has yet to take shape in a material way. The industry is in their last two weeks of the quarter, analysts are beginning to lower their forecasts and many will be watching to see if the companies follow suit by lowering guidance.

Maybe second quarter 2019 contractual pricing was favorable enough compared to second quarter 2018 to hold off earnings degradation. Diesel fuel prices were likely a tailwind to earnings and the group should have seen a reduction in driver recruiting and hiring expenses in the quarter. It will be interesting to see if these items were enough to save the quarter relative to expectations. That said, the lack of a more material increase in demand will likely weigh on truckload earnings at some point in the near future.

“Freight downturns typically last for 12 to 19 months… and we are in the seventh month,” said Wadewitz.

JBHT will be the first company to announce its second quarter earnings on July 15, 2019.