P.A.M. Transportation Services (NASDAQ: PTSI) reported a “marked improvement” during the third quarter as the truckload (TL) industry distanced itself from a second quarter that displayed steadily improving demand trends, albeit off of a low base, and incremental costs associated with COVID-19.

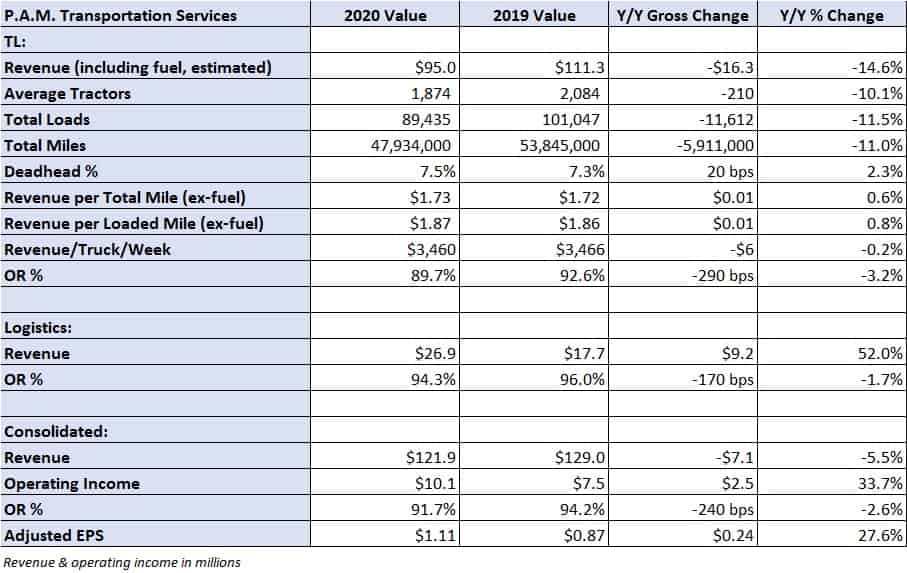

The Tontitown, Arkansas-based carrier reported net income of $6 million or $1.04 per share. Excluding losses from investments in equity securities, the carrier reported adjusted net income of $6.4 million, or $1.11 per share, ahead of the $0.47 consensus estimate and the prior-year result of $0.87.

Total revenue declined 6% year-over-year to $122 million, basically flat excluding fuel surcharges at $110 million. P.A.M. Transportation’s trucking segment saw revenue decline 15% year-over-year as average tractors in service declined by 210 units, down 10%, with similar declines seen in loads and total miles. Revenue per tractor per week was flat at $3,460.

“Our quarterly results show marked improvement as compared to the previous quarter of this year where the company felt the full impact of revenue losses associated with the closing down of three of our top 10 customers due to COVID-19 concerns,” stated the company’s new CEO and President Joe Vitiritto.

Vitiritto joined P.A.M. Transportation in mid-August. He was formerly head of pricing and network design at Knight-Swift Transportation (NYSE: KNX)

P.A.M. Transportation, which generates nearly half of its revenue from the auto manufacturing sector, posted a $2.5 million loss, 43 cents per share, excluding gains from equity securities during the second quarter.

“With the return to operations for these customers and the general increase in nationwide economic activity, we quickly bounced back to a more normal mode of daily activity. While we aren’t satisfied with these results, they are an indication of a strong model which will only require modest adjustments to attain our updated profitability improvement goals,” Vitiritto continued.

Revenue per loaded mile, excluding fuel, was down 1 cent year-over-year at $1.87. However, Vitiritto sees the current tightness in TL supply as conducive for future rate increases.

“This supply-and-demand imbalance allowed us to recover the rate declines experienced during the first few months of the pandemic. The page has now been turned and with shippers facing upward rate pressure, we continue to have the momentum necessary to significantly improve our rate structure as we move into the final quarter of 2020 and expect this upward pressure to continue well into next year,” Vitiritto said.

The company’s TL operating ratio, operating expenses as a percentage of revenue, improved 290 basis points to 89.7%. The release credited recent cost-savings initiatives as the reason for the improvement but noted that driver pay and insurance present future cost headwinds.

“Another lingering effect of the COVID crisis is the impact on our ability to hire enough drivers to fill all of our available trucks. Our current model relies on a strong pipeline of student drivers, and due to social distancing guidelines, schools were limited by capacity restrictions, which left us with a pipeline gap that we continue to try to fill,” stated Vitiritto. The company plans to increase recruitment efforts to “get back to full capacity utilization.”

The carrier didn’t provide a balance sheet or cash flow statement with the report. It has repurchased 50,000 shares so far this year and has almost 180,000 remaining on the existing repurchase authorization. P.A.M. Transportation continued with its capital expenditure program, reporting an average truck age of 1.6 years.

P.A.M. Transportation ended the second quarter with $12.9 million outstanding on its $60 million revolver and total availability of $47.1 million. The company reported $300,000 in cash and $25.7 million in equity securities holdings. P.A.M. Transportation listed current debt maturities of $64.6 million and total debt of $233.1 million in its second-quarter filing.

“We remain enthusiastic about our quick recovery and the prospect of entering the final quarter of the year with positive momentum on the rate front, along with an improved cost structure, provides a high level of confidence that we can achieve our profitability objectives,” concluded Vitiritto.