Retail, CPG pricing disagreement boils over in Europe

Depending on whom you believe, either European grocer Carrefour stopped selling Pepsi products in certain locations, or Pepsi pulled out and decided to stop selling at the grocer. Whatever the specifics, the parties couldn’t agree on the value of potato chips, and it’s clear that retailers and CPG companies have become even more at odds than usual as commodity prices have fluctuated. Even if the Carrefour impasse persists, it isn’t going to put much of a dent in Pepsi’s financials — some analysts estimate that sales in the impacted countries (France, Italy, Spain and Belgium) represent 0.25% of Pepsi’s total revenue. But the situation reflects the very impactful tension between retail and CPG that the public rarely sees.

What’s more typical is that closed-door disputes result in subtle, but impactful, changes in shelf placement. Retailers’ private-label investments and the pricing of those products are another form of recourse that retailers more typically employ. In this case, I wonder whether the grocer’s decision (if it was, in fact, the grocer’s) to stop carrying Pepsi products was a way to get the public on its side. After all, shoppers tend to blame retailers rather than suppliers for high prices.

A recurring topic on The Stockout, here is a quick summary of the rising tension: Inflation started accelerating in CPG cost structure in early to mid-2021, lead CPG companies to ask retailers for price increases in the subsequent quarters and years that were both more numerous, and of a greater magnitude, than retailers were accustomed to. Retail prices adjusted less quickly than CPG companies’ costs, so CPGs experienced significant margin compression — and margins had already been depressed due to extra supply chain costs associated with COVID. Adding to the strained relationship, most CPG companies last year were reluctant to cut prices even as commodity prices declined, citing cost increases in areas other than traded commodities, such as labor, packaging and processing. That caused retailers to place more onus on CPGs to demonstrate why any further price increases are necessary. The largest retailers have used more aggressive language on their latest round of analyst calls, suggesting that they expect price reductions, or at least very minimal price increases, from suppliers.

Constellation Brands’ beer business continues to face inflationary pressure

In its earnings presentation Friday, Constellation Brands (maker of Modelo and Corona beers in addition to wine and spirits), highlighted numerous cost pressures in its beer business for the current fiscal year (ending February 2024):

- Raw materials and packaging (55%-60% of cost of goods sold) up high-single digits.

- Freight (20%-25% of COGS) up high single digits.

- Labor and overhead (10%-15% of COGS), up high teens.

Freight costs up high single digits was surprising but may reflect rail costs in addition to truckload since much of the company’s beer is manufactured in Mexico. In addition, it should be noted that those cost comments were largely backward-looking since the company is already in its fiscal Q4.

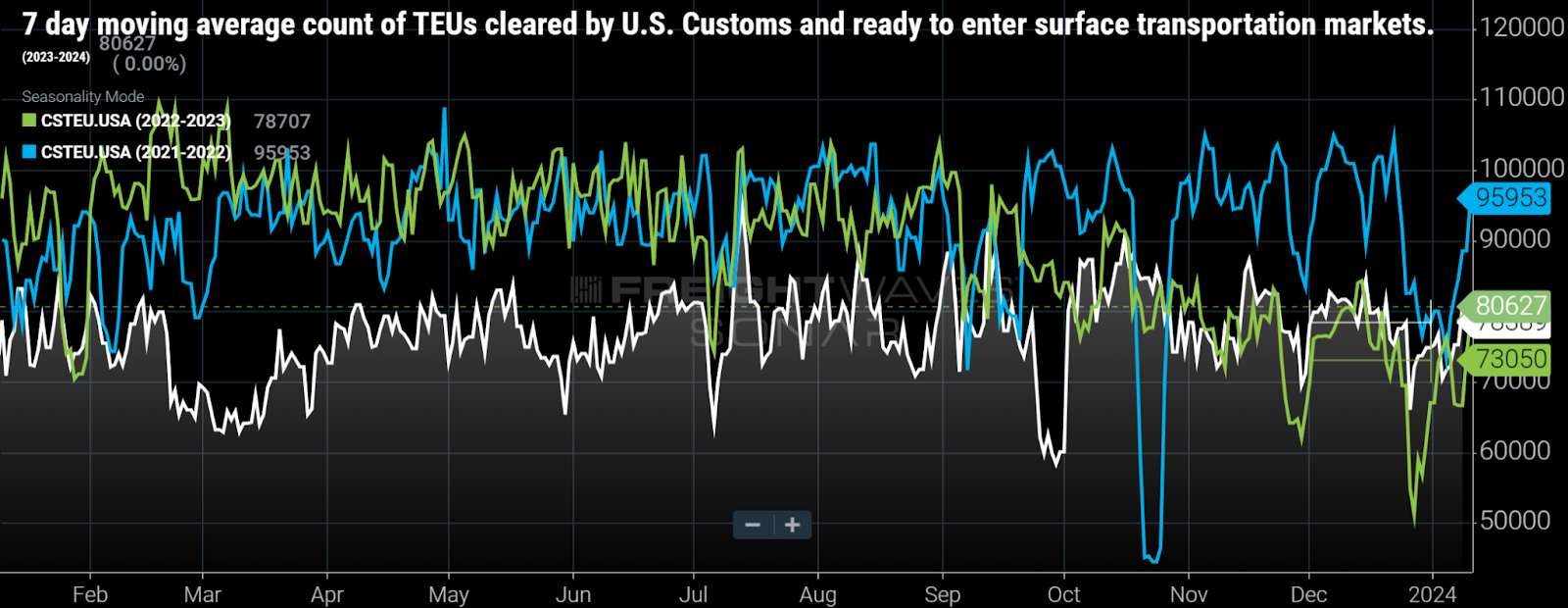

Import volume ekes out y/y growth in December

This article by Greg Miller breaks down U.S. import growth in December. Descartes’ data shows December imports up 9.2% y/y, while U.S. Customs data in SONAR shows similar volume growth of 7.4% in the same period. Part of that gain is related to easy year-ago comps, but it was perhaps remarkably stable considering the turmoil in the global shipping markets between the drought at the Panama Canal and the attacks in the Red Sea. Even more counterintuitively, volume comps were stronger in the Gulf Coast and East Coast import markets than they were on the West Coast.

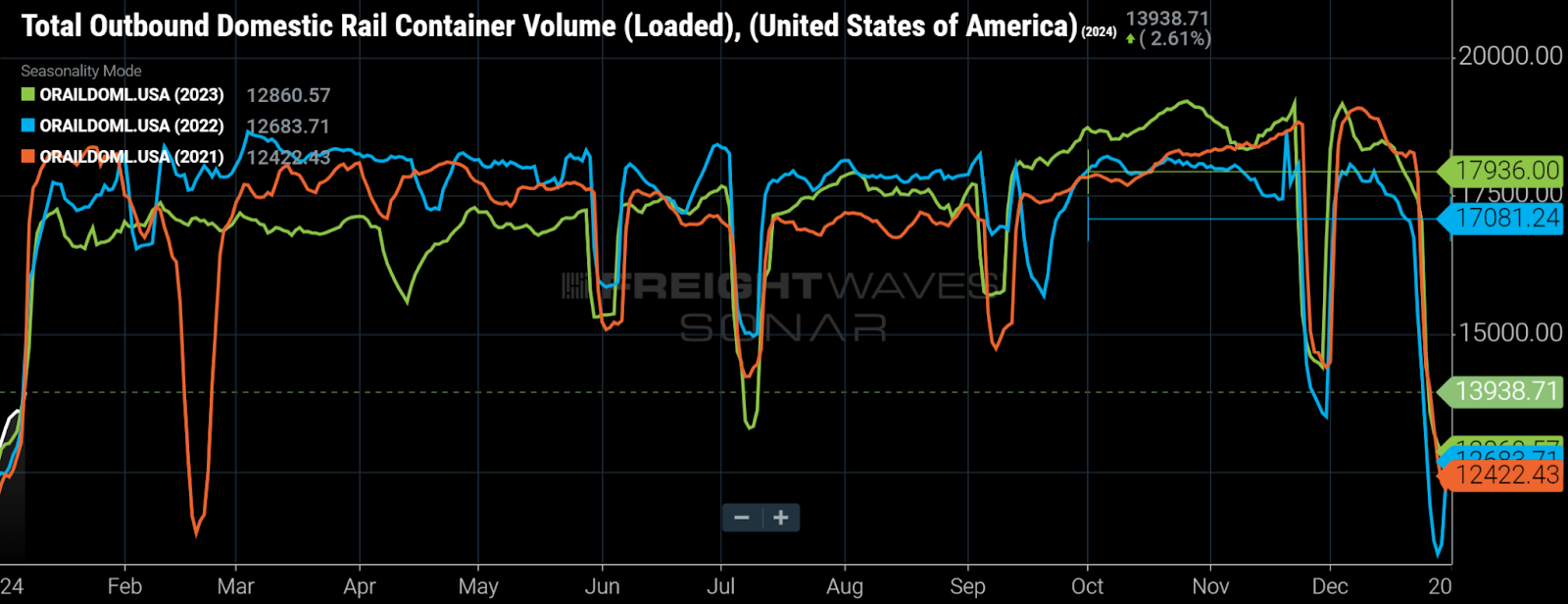

Loaded domestic intermodal volume posts 5% y/y growth in Q4 2023

Contrary to the expectations of most heading into the fourth quarter that there wouldn’t be much of a peak season in intermodal, when considering only loaded 53-foot containers, volume was up a meaningful 5% y/y in Q4. While intermodal service levels have been strong, and 5% y/y growth may represent a positive variance versus some analysts’ expectations, it’s not clear that represented a gain in market share when compared with long-haul truckload volume. The long-haul (>800 miles) truckload volume (LOTVI.USA) contained in SONAR showed a 7.9% y/y increase in tenders and a 7.1% y/y increase in accepted tenders (when considering the increase in the long-haul tender rejection rate from 4.2% in Q4 2022 to 4.9% in Q4 2023). Therefore, it appeared that the fourth quarter was more a story of increased long-haul demand rather than gain of modal share. However, that’s not to say definitively that intermodal lost share because many long-haul truckload volumes are in lanes that are not compatible with rail intermodal. Going forward, for the railroads and their domestic intermodal partners to capitalize on their newly established or expanded partnerships, service levels will be critical for volume growth.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.