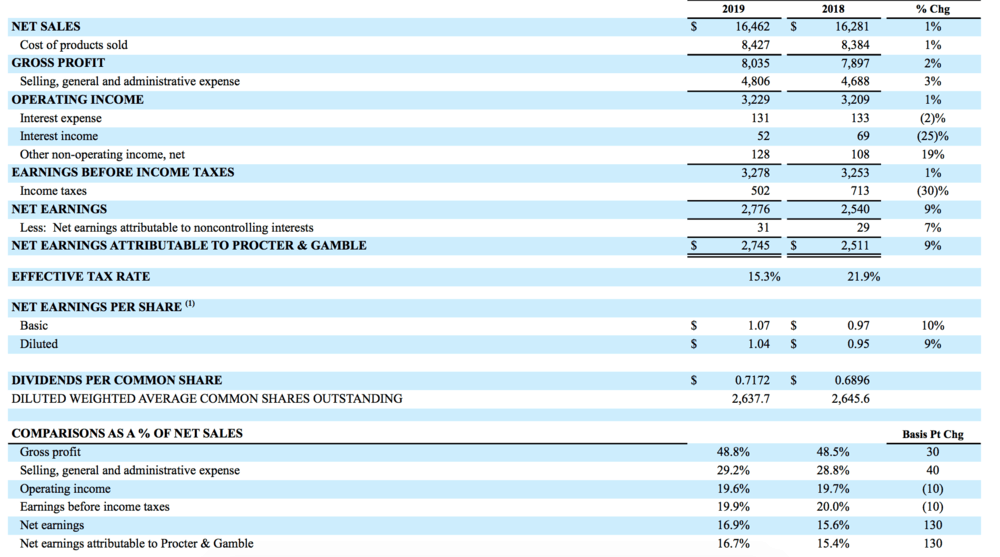

The Procter & Gamble Company (NYSE: PG) beat analysts’ expectations on both earnings per share (EPS) and net sales in the third quarter of fiscal year 2019. The company reported net sales of $16.5 billion, up 1 percent year-over-year and ahead of analysts’ $16.34 billion estimate.

Diluted net EPS came in at $1.04, up 9 percent from the same quarter in 2018. Core EPS climbed 6 percent to $1.06, beating estimates of $1.03. Currency-neutral core EPS increased 15 percent year-over-year.

The company attributed the rise in core EPS to an increase in net sales and a lower effective tax rate. Those benefits were partially offset by a reduction in operating margin, due primarily to negative currency and commodity cost impacts, according to the company’s earnings release.

P&G has beat earnings estimates every quarter for the past year.

“We delivered another quarter of strong organic sales growth, enabling us to further increase our outlook for the year,” David Taylor, chairman, president and CEO of P&G said in the earnings release. “Cash generation also remains strong, supporting an increase in our cash productivity target and extending our long track record of dividend increases. Our focus on superiority, productivity and improving P&G’s organization and culture is delivering improved results despite a challenging competitive and macroeconomic environment.”

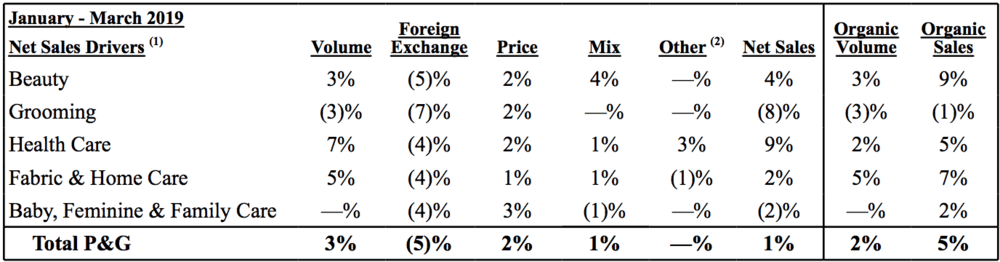

While net sales were up 1 percent year-over-year, organic sales increased 5 percent, thanks to a 2 percent increase in organic shipment volume, according to the company’s earnings release. Pricing also added 2 percentage points to organic sales.

Organic sales exclude the impacts of foreign exchange, acquisitions and divestitures.

Beauty segment organic sales showed a 9 percent increase over the same quarter last year. Skin and personal care organic sales showed the strongest growth in the segment, which the company attributed to premium innovation, positive product mix from the disproportionate growth of super-premium SK-II brand and increased pricing.

Grooming segment organic sales fell 1 percent year-over-year. The sale of grooming appliances decreased mid-single digits due to negative mix impacts from the disproportionate growth of mid-tier products, according to the company.

Organic sales in the company’s health care segment increased 5 percent year-over-year. Oral care organic sales and personal health care organic sales both increases mid-single digits. The company attributed the spike in oral care sales to strong volume growth and positive sales mix in developed markets driven by premium toothpaste and toothbrush innovations, while the growth in personal health care was due to devaluation and innovation related price increases.

The acquisition of Merck OTC caused all-in sales to rise double digits in personal health care.

The fabric and home care segment experienced a 7 percent rise year-over-year, driven by fabric care organic sales. As in other segments, the company attributed this growth to innovation, increased pricing and positive mix due to the disproportionate growth of premium products.

The company’s baby, feminine and family care segment saw a 2 percent increase in organic sales year-over-year. Feminine care sales increased high single digits, while family care sales rose mid-single digits. However, these increases were offset somewhat by a low single digit decrease in baby sales. P&G attributed the drop to competitive activity and market contraction.

Reported gross margin increased 30 basis points. Core gross margin was unchanged year-over-year, including 60 basis points of negative foreign exchange impacts.

“Operating profit margin decreased 10 basis points versus the base period on a reported basis including approximately 60 basis points help from lower non-core restructuring charges,” according to the report. “Core operating margin decreased 60 basis points including 100 basis points of negative foreign exchange impacts. On a currency-neutral basis, core operating margin increased 40 basis points including total productivity cost savings of 260 basis points for the quarter.”

The company issued a soft outlook, predicting fiscal 2019 all-in sales growth in the range of in-line to up 1 percent versus 2018, including a negative impact of 3 to 4 percentage points from the combination of negative foreign exchange and a modest positive impact from acquisitions and divestitures.

The company maintained its guidance on the bottom line, expecting diluted EPS to rise 17 to 24 percent year-over-year. Core EPS are expected to climb 3 to 8 percent in fiscal year 2019 over 2018.

P&G expects to pay over $7 billion in dividends and repurchase approximately $5 billion of common shares this fiscal year.

The company’s stock was down 1.91 percent in pre-market trading on Tuesday, April 23.