Logistics real estate investment trust (REIT) Prologis Inc. (NYSE: PLD) reported “robust” activity within its portfolio as more sectors come back on line.

On the Tuesday third-quarter earnings call, CFO Tom Olinger said operating conditions are “meaningfully better than they were 90 days ago,” with utilization at its properties “returning to near-peak capacity,” which has driven earnings above pre-COVID levels.

The increase in logistics real estate demand is in part being driven by robust e-commerce growth and the need for more final-mile delivery capacity. The duration of the pandemic has accelerated these trends as more consumers increase their online spending on hard goods, which require storage and shipment. Further, many supply chains are seeking logistics warehouses closer to the consumer in efforts to streamline operations and improve delivery times.

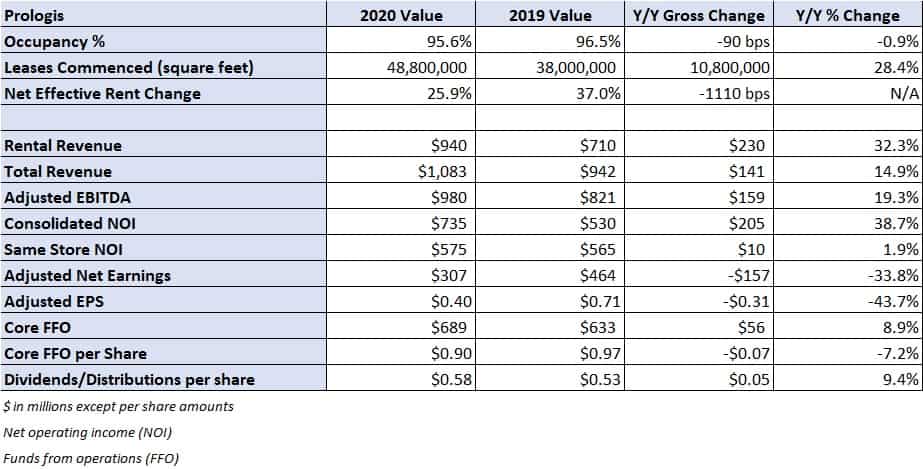

The San Francisco-based company reported third-quarter core funds from operations (FFO) of 90 cents per share, 2 cents ahead of the consensus estimate.

Takeaways from the call

New lease proposals are up 12% year-to-date and 3% higher than the second quarter. Management said the food and beverage, health care, and consumer products verticals continue to replenish “razor thin” inventories as other sectors have seen activity resume. E-commerce represented 37% of new proposals in the quarter compared to just 21% on average. Amazon.com (NASDAQ: AMZN) accounted for 13% of new leasing, with third-party logistics providers (3PLs) representing one-third, which was a record.

On the growth trajectory for e-commerce-related properties, Prologis Chairman and CEO Hamid Moghadam says he believes the industry is still in the “very early innings.” He said the growth rate will continue to be very significant during the pandemic but that there will likely be a pause as the impacts of the virus diminish. The growth will still be elevated compared to pre-COVID levels as consumers have a more digital approach to shopping.

On the concern over retail property being converted into logistics space and potentially upsetting the current low-vacancy dynamic, management believes retail conversions will be small, with only 77 million square feet of incremental supply being created in the next decade. They said that accounts for less than 5% of last-touch facilities, less than 1% of logistics facilities and less than 3% of annual new logistics real estate construction in the nation’s top 25 markets. Often the conversions are not economically feasible and face strong legal and zoning headwinds.

Asked about the concern level over California Proposition 15, which would tax commercial and industrial properties on market value instead of purchase price, management said that recent polling suggests it won’t pass. Either way, they don’t see it as a big impact to Prologis. But they do see the increase in commercial property taxes, which is expected to generate $6.5 billion for $11.5 billion to local governments and schools, as problematic to doing business in California, describing it as “just another tax from California to these businesses.”

Guidance raised slightly

Prologis raised 2020 guidance for core FFO to $3.76 to $3.78 per share from $3.70 to $3.75. New development starts were increased to $1.8 billion at the midpoint of the new range, compared to the prior midpoint of $1 billion that was provided in the second-quarter report. The new guide remains below pre-pandemic expectations issued at the beginning of the year. Building acquisitions are now expected to range from $700 million to $800 million.

Third-quarter results

Consolidated revenue increased 15% year-over-year to $1.08 billion, with rental revenue increasing 32% to $940 million, both of which are inclusive of prior portfolio acquisitions. Lease starts increased 28% to nearly 49 million square feet, customer retention dropped 810 basis points from the second quarter to 72.8% and occupancy dipped 90 basis points to 95.6%.

Retention has been negatively impacted as growing companies needing more space have moved and as struggling companies have closed. Retention rates are expected to remain lower near-term but in the 70% to 80% range, which is in line with the Prologis longer-term average of 75%.

Prologis ended the third quarter with $4.3 billion in available credit and $940 million in cash. Including open-ended funds and $2.6 billion of liquidity at co-investment ventures, Prologis has more than $13 billion in investment capacity. The company’s debt-to-market capitalization ratio was 19.2% at the end of the quarter.

Prologis’ industrial real estate portfolio exceeds $136 billion in total assets under management. The company’s nearly 1 billion square feet of owned and managed properties spans 19 countries, serving 5,500 customers. Many of its warehouses in the U.S. service ports on both coasts, regional distribution hubs, and rail and intermodal facilities.