Prologis Inc. (NYSE: PLD), the world’s leading logistics real estate investment trust (REIT), sees its business slowing in the near-term, but believes that there will be a strong snapback in demand after a vaccine for COVID-19 is discovered.

On its first quarter 2020 earnings conference call, management said that approximately 60% of its customers are growing, while 40% are shrinking. The company is seeing strong demand for logistics real estate, especially anything related to the consumer staples and e-commerce segments while hospitality and brick-and-mortar retail real estate is off. Management believes that the “reduced demand environment” will persist for the remainder of the year, but noted that e-commerce as well as inventory increases in the supply chain will provide tailwinds.

In an update call held earlier in the month, management outlined the prospects for supply chains carrying incremental inventory moving forward in efforts to avoid the supply shock they just endured. Management believes that some supply chains could add as much as a 5%-10% to “safety stock” in the future.

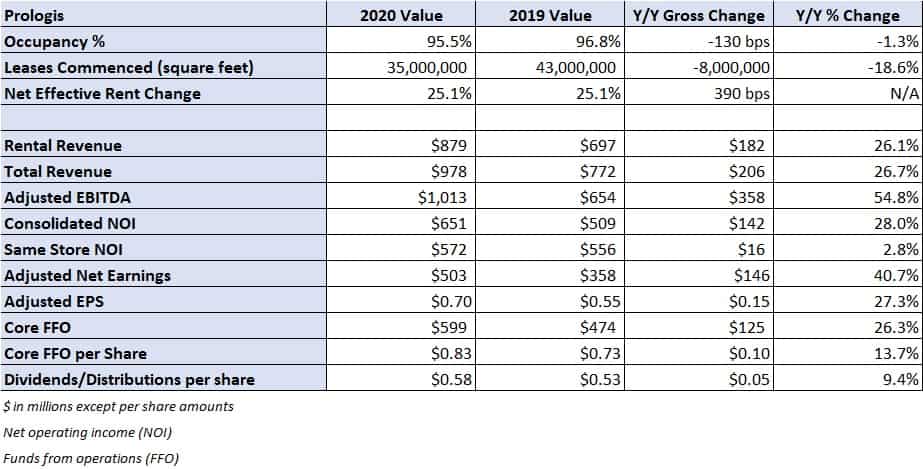

Prologis reported first quarter 2020 core funds from operations (FFO) of $0.83 per share, a penny ahead of analysts’ expectations.

“Our strong first quarter operating performance is a result of our long-term focus on the world’s top consumption markets. While the current environment is challenging, we are well-prepared. We have confidence in our team, our strategy and in the strength of our portfolio,” stated Prologis CEO Hamid R. Moghadam.

Prologis has seen an uptick in rent release requests, representing 4.3% of gross annual rent to date. Seventy percent of the requests have been denied, 23% are under review and 7% have already been granted. Prologis expects to grant rent deferrals in the form of a repayable loan due by the end of 2020 to clients representing less than 1% of the company’s annual gross rent. The company has already collected 85% of rent payments for April, a level that is within 1% of normal payment collection rates.

Management said that a high percentage of its customers will likely benefit from some form of government stimulus, but conceded that of its customers that are struggling, some will see longer roads to normalcy and some are likely to fail.

Prologis modestly trimmed its outlook. The company now expects to see $3.55 to $3.65 per share in core FFO in 2020 compared to its prior guidance calling for $3.67 to $3.75. Year-end occupancy is expected to be in a range of 94.5% to 96% versus the prior outlook of 96% to 97%. Management expects occupancy to spike higher around the time a COVID-19 vaccine is announced, noting that some experts are calling for this to occur next summer.

Prologis has roughly 8% of its leased properties up for renewal in 2020.

Management expects market rent growth to be flat in 2020 given the demand headwinds from the outbreak that have resulted in shutdowns and shelter-in-place mandates globally. They said that rent growth was 200 basis points better than expected in March and 400 to 500 basis points better that expected for its recently acquired portfolio. Prologis closed on the acquisitions of Liberty Property Trust and Industrial Property Trust, Inc. (IPT) earlier this year.

The company’s guidance assumes no new capital deployment other than the projects already under contract. Prologis is moving forward with speculative development that is fully committed and 30 previously negotiated build-to-suit agreements. The clients represented in all 30 of the build-to-suit agreements have “indicated their intention to move forward as planned.”

Management said that the cost to complete current projects stands at $1.6 billion.

Prologis ended the first quarter with $3.8 billion in credit line availability and $800 million in cash. The company’s debt-to-market capitalization ratio was 22%. Including the company’s co-investment ventures of $3.1 billion and open-ended funds, it has “well over” $10 billion in investment capacity.

“We entered the COVID-19 crisis in a position of financial strength. We have significant liquidity as well as investment capacity and our dividend is well-covered,” said chief financial officer Thomas S. Olinger.

San Francisco-based Prologis owns nearly one billion square feet in industrial real estate across 19 countries. Many of its warehouses in the U.S. service ports on both coasts, regional distribution hubs and rail and intermodal facilities.