Radiant Logistics, Inc. (NYSE: RLGT) reported several records for fiscal 2019, including a 15% increase in net revenue, an 80% jump in adjusted net income and a 40% improvement in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA).

“We are very pleased to report another year of solid financial results for fiscal 2019. We set new records across several key financial metrics,” said founder and CEO Bohn Crain.

The third-party logistics and multimodal transportation services provider reported adjusted earnings per share (EPS) of $0.15 for its fiscal fourth quarter 2019 (ended June 30), versus the consensus EPS estimate of $0.12 and $0.04 better than the prior year period.

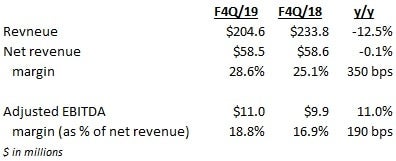

In its fiscal fourth quarter, Radiant reported a total revenue decline of 13% year-over-year to $204 million with net revenue remaining level at $59 million. The net revenue margin increased 350 basis points to 28.6% with an adjusted EBITDA margin improving 190 basis points year-over-year to 11%. Management said that the trends from the “softer freight environment” seen in the quarter have continued into its fiscal first quarter 2020 ending in September.

On the earnings call with analysts and investors, management talked about its strong financial position and its desire to make smaller tuck-in acquisitions. They prefer the smaller deals as the valuation multiples are typically more attractive and the acquisitions can be easier to integrate. Additionally, management said that they are comfortable leveraging debt to 2x to 3x EBITDA if the right deal or two came along.

Radiant has the liquidity to pursue acquisitions and/or convert agent-based forwarding stations into company-owned stores. At the end of the June 30 fiscal year, Radiant had just $13.8 million of its total net debt of $31.2 million drawn on its $75 million credit facility. This leaves the company levered at less than one time trailing twelve months adjusted EBITDA, which was $40.8 million. Up to four times debt-to-EBITDA is typically viewed as acceptable by investors for companies pursuing acquisitions.

“As we have previously discussed, our incremental cost of supporting that next dollar of gross margin is very small and we are very excited about our opportunity to drive further expansion in our adjusted EBITDA margins as we continue to scale the business and leverage the benefits of our on-going technology investments,” said Crain.