Third-party logistics and multimodal transportation services company, Radiant Logistics, Inc. (RLGT), reported earnings of $0.11 per share for the quarter ending March 31, 2019 (RLGT’s third fiscal quarter 2019), $0.04 better than the consensus estimate and $0.06 better year-over-year.

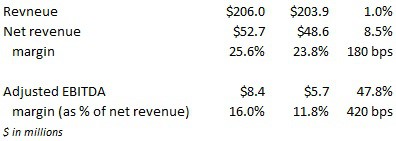

Total revenue increased 1 percent year-over-year to $206 million with net revenue climbing 8.5 percent to $52.7 million. The net revenue margin increased 180 basis points to 25.6 percent with an adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) margin 420 basis points better at 16 percent.

On the earnings call, management acknowledged the slowing revenue growth rate, but said that they “remain very bullish” regarding the overall business. Management’s goal is to grow revenue in the 4 to 6 percent range moving forward excluding acquisitions with EBITDA growth in the 8 to 12 percent range. Management said that some of the slowdown in growth was due to increased selectivity on new business. They feel that they can continue to drive EBITDA growth by moving more freight onto their transportation management system. The company has had nice traction doing this on the domestic side and will begin to do this internationally in the fall. Management has an optimistic outlook (“best financial position in the company’s history”), but noted that this quarter was the last easy quarter from a year-over-year comparison perspective due to some “chunky” business wins last year.

From the earnings press release, “The business also continues to deliver strong cashflows generating $17.1 million in cash from operations from the three months ended March 31, 2019 and generating $33.5 million in cash from operations for the nine months ended March 31, 2019.”

Strong cashflow generation has allowed RLGT to pay down debt and improve its capital structure. The company retired $21 million of preferred stock in December 2018. RLGT has $16.9 million outstanding on its $75 million credit facility and total net debt of $34.7 million. That is less than one time their trailing 12-month adjusted EBITDA of $39.7 million (up to four times EBITDA is typical for companies pursuing acquisitions).

This leaves RLGT in a position to acquire more agent-based networks that benefit from RLGT’s size and scale (improved purchased transportation economics) and creates cost synergies by streamlining the back office operations and operating the acquired entity on its current platform.

“We are open for business,” said management. They have the liquidity to pursue acquisitions and convert agent stations into company-owned stores. They have “been on the trail” looking at several potential targets with emphasis on freight forwarding, Canada and U.S. truck brokerage and intermodal opportunities.

If acquisitions and agent conversions slow, they will look to repurchase stock and continue to pay down debt.

Management concluded, “Our now more than 10-year first market advantage in executing our multi-brand strategy in consolidating agent-based forwarding networks, ongoing investment in technology and low leverage on our balance sheet puts us in a unique position to support further consolidation in the marketplace. We are patiently persistent in the pursuit of this long-term vision which we believe, over time, will deliver meaningful value for shareholders, our operating partners and the end customers that we serve.”