Drivers and fleet owners who don’t understand all the nuances of how the retail price of diesel is set should think of it as a stacked bar chart.

At the base is the price of crude. That will always be the biggest factor, because except for renewable supplies of diesel, the fuel comes from crude. From there, the stacked bar chart will grow with much smaller blocks: spreads between the price of ultra low sulfur diesel on CME and important spot markets like the Gulf Coast; wholesale margins; and static numbers like excise taxes.

But in 2021, there’s been another significant building block on that chart, at times possibly adding as much as 15 cents per gallon to the price of retail diesel.

It’s the Renewable Volume Obligation (RVO), which has been driven higher by a combination of government mandates and increasing prices for the agricultural products used to make the renewable fuels that are in the formula for calculating the RVO.

Companies involved in the commercial market for fuels are required to show use of a certain percentage of renewable fuels. They can get there by blending products such as ethanol into gasoline or biodiesel into finished diesel. Or they can acquire RVO credits, which are a way of essentially buying your way into compliance with the law.

A problem for the diesel market beyond the price of the RVO is the structure of the renewable fuels program: When the RVO gets high, it can incentivize making jet fuel instead of diesel. It can also incentivize exporting diesel rather than selling it into the domestic market. That is not new; it’s a permanent feature of the market. But as the price of RVOs increases, it increases those incentives.

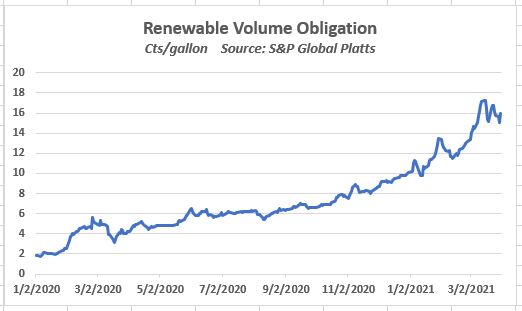

Matthew Kohlman, associate editorial director for clean products at S&P Global Platts, said the price of RVOs opened 2020 trading near 2 cents per gallon. It moved up to 5-6 cents per gallon by midyear and crossed 9 cents by the close of 2020.

Prices for virtually all commodities began to climb in late 2020 and continued into 2021, and the price of RVOs rose alongside those increases. RVOs peaked at above 17 cents per gallon by the middle of March. Prices have softened slightly since then but recently have been more than 15 cents.

“You had multiyear lows just a year ago, and now you have record highs,” Kohlman said.

That RVO value needs to be added to the ultimate price. “When you’re a trader trading 25,000 lots, that actually gets very expensive,” Kohlman said.

The daily number for an RVO is published by price-reporting agencies such as Platts. But the formula itself is complicated and comes from the Department of Energy, which administers the Renewable Fuel Standard (RFS) that the RVO is designed to support.

The formula is based on a tradeable credit called a Renewable Identification Number (RIN). There’s a RIN for ethanol, there’s a RIN for biodiesel, and there are RINs for other renewable fuel feedstocks.

The RIN allows any business that needs to meet renewable fuel requirements to use it toward RFS compliance. It is a credit that some player in the supply chain generated by blending renewable fuels into its final product. For somebody who hasn’t blended in enough renewable fuels to meet government requirements, purchasing a RIN moves the buyer toward compliance. Showing proof of the RIN, for compliance purposes, is the same as if that fuel supplier had blended ethanol into gasoline or biodiesel into diesel.

Driven in part by the higher costs for agricultural feedstocks, RINs prices have moved higher. That in turn has pushed up the price of RVOs.

Which brings us back to the analogy of the diesel price as a stacked bar chart. If there were no Renewable Fuel Standard in the U.S., there wouldn’t need to be an RVO value. But the standard does exist, so in some ways, the RVO is the last number tacked onto the chart, creating the final price of diesel. And for most of this year, that number has been in double digits.

“Over time, the diesel price will have to capture that RVO price,” Kohlman said. “The RVO price is inside it.”

While multiple factors are driving RIN prices and in turn RVO prices, inflation in agricultural commodities has been key. In the past year, soybeans have moved up to about $14.50 a bushel from $8 a bushel. And while corn is blended into ethanol, which in turn goes into gasoline — so it isn’t part of the diesel pool — the rising price of ethanol affects RVO values. At $6 a bushel, corn is near a five-year high.

But the impact of higher RVO prices doesn’t end there. Compliance with the Renewable Fuel Standard is part of the U.S. transportation fuel supply. But it doesn’t govern exports.

While the price of the RVO in a perfect economic model could be passed on to the consumer — like a fuel surcharge — the real world doesn’t always work so smoothly. Kohlman noted that the economics of whether to put diesel into the domestic market, where the RVO would impact its price, or the export market, where it wouldn’t, could incentivize sending diesel abroad if that RVO value can’t be captured by the supplier.

U.S. exports of all non-jet-fuel distillates were 1.074 million barrels a day in the week ended April 9, according to the Energy Information Administration. That is down from the second week of April in the last five pre-pandemic years.

But the latest number is only the fifth time it has been above 1 million barrels a day this year. U.S. exports of distillates like diesel — but not including jet — have been running consistently above 1 million barrels a day, with some exceptions, since 2012.

Diesel exports therefore are well below average, but that’s in a market still disrupted by the pandemic. That makes it difficult to draw a conclusion on whether they’ve been lifted by suppliers trying to avoid the RVO hit. But the fact that it is a possibility shows how the RFS and the RVO number can impact supply into the U.S. market.

The second impact in the distillate market is the trade-off between jet fuel and diesel production. Both are distillates, and at the start of the pandemic, refiners tried to shift as much distillate output away from jet and toward diesel given the massive collapse in jet demand. That shift has eased and a more normal balance between jet and diesel output has returned.

But there is no renewable fuel standard for jet fuel, for a variety of reasons, including concern about fuel performance in jet engines. What that means is that the same calculation that goes into exporting diesel — the absence of an RVO hit — also is a factor in a refinery decision about whether to produce jet or diesel.

So far, the data is not showing any significant shift. U.S. diesel output most recently was 4.44 million barrels a day, down from 4.76 million barrels a day two years ago and about that same amount as three years ago.

Jet output has been rising, up to 1.139 million barrels a day from 1.07 million at the start of the year. But that increase does not look to be coming out of diesel output and is to be expected given the increasing numbers of people in the air. But like the export market, it continues to have a potential impact on diesel supplies.

More articles by John Kingston

Latest California AB5-related decision spurs new appeals, court arguments

Pandemic-fueled hedging innovation on diesel may be a keeper

Teamsters protest in SoCal gets burst of support from longshoremen