Several reports issued at the start of this week are driving home the enormous strength of the current freight market.

As a sub-headline on a Stifel report said: “Running out of ways to describe just how strong the orders are.”

That came in a Stifel commentary on the report by ACT Research on truck orders. ACT publicly released a limited amount of data on its March findings, highlighting that orders for truck classes 5-8 totaled more than 70,000 in March. ““For only the fourth time on record and for the second time in Q1’18, medium duty and heavy duty orders combined to exceed 70,000 units in a month, as activity in both the medium and heavy duty vehicle markets remained strong,” Kenny Vieth, ACT’s President and Senior Analyst, said in a prepared statement.

The Stifel analysis of the ACT data was more granular. It said that ACT reported class 8 net orders exceeding 40,000 units for the third consecutive month. The year-on-year gain was 102%, and the October-March “order season” gain was 97%.

Stifel said the actual count on class 8 vehicle sales was 46,900 units, which besides being up more than 100% year-on-year also was up 16% just from January.

Stifel’s report tried to tackle a question that has come up in other forums: if it’s tough to get drivers to take a truck on the road, why buy a new one? “Our response has become, ‘they can’t seat them unless they buy them.’” In a market with so much focus on retention and recruitment, offering up the most modern trucks is an asset, Stifel said. “Competent drivers have the pick of driving for a company putting them in a brand new truck and that, along with an increase in pay, is required to attract and retain drivers in the current market,” Stifel said.

There may be some FOMO working in the industry. FOMO, or fear of missing our, wasn’t cited by Stifel per se, but in its report—which was focused on the actual builders of trucks—analysts noted that “we believe that the rapid filling of available build slots encouraged build owners to put orders in quickly.” It also suggested that investors in the manufacturers of heavy duty vehicles, like Navistar, may be starting to transition away from the idea that 2018 is the peak year in this market cycle to a likelihood that 2019 will be that.

The market also is being driven by the fact that trucks from the 2014-2015 peak are going to be traded in, given that they are at the end of their 4-5 year trade cycles.

FTR, which does its own estimate of vehicle sales, said its preliminary numbers for March on class 8 vehicle sales was 46,300 units, just 600 less than the ACT estimate. It called that number the third highest on record, up 15% from a month earlier and up 103% from March 2017.

It also talked about the demand going forward. “Fleets are attempting to add capacity as fast as possible in a dynamic market,” FTR said in a prepared statement. “Some OEMs had exceptional order months as fleets scramble to lock in order slots for this year.”

Don Ake, FTR’s vice president of commercial vehicles, was blunt in the statement: “The current capacity crisis may be the worst ever.”

In other indicators, the Morgan Stanley TLFI index was strong across the board. Both against what Morgan Stanley calls “sequentially” and “vs. seasonality,” the index was up for vans, refrigerated and flatbeds, though the latter was flat against season trends.

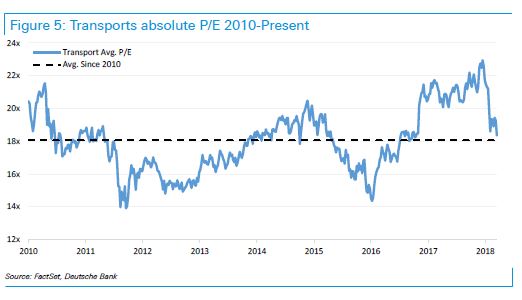

The ACT and FTR data were released just after Deutsche Bank’s transportation research team, led by Amit Mehrotra and Seldon Clarke, came out with a bullish report and an upgrade of the stocks of Union Pacific, J.B. Hunt and Werner Enterprises. Part of the reason for the upgrade to a Buy rating have been the pullbacks during the recent stock market slide.

But it was also driven by factors specific to those companies. The Deutsche Bank analysts said recent meetings with J.B. Hunt management were positive. The analysts’ estimate of $6.75 earnings per share in 2019 are 15% above consensus, the report said, but they are sticking to it. The EPS project, “(a)t today’s current valuation equates to $141 per share.” J.B. Hunt stock dropped to less than $114 in early trading Wednesday.

The recent selloff in Werner Enterprises stock is an opportunity, Deutsche said, because the company has set guidance of 6-10% growth in yield, “the highest growth in yield in the 32-year history of the company.” Also, Deutsche cited statements by Werner in its recent annual report that the early performance in 2018 has been strong.

The report contained numerous other increases in Deutsche estimates of company earnings. Increases in EPS this year, next year or both were projected for Old Dominion Freight, Landstar and ArcBest, though slight reductions were projected at C.H. Robinson and Heartland.

You can follow all of the freight-related stocks at: https://www.freightwaves.com/stocks