This week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 20 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Ocean freight deserts truckload markets, leaving them high and dry

With the inflation-squeezed consumer running through their discretionary budgets, freight demand is in a precarious state. Not only has it now become more expensive to buy goods outright, but it has also become much more costly to use credit, with the average interest rate on a credit card spiking to an all-time high above 20% in January. This credit bubble could force the economy toward another inflection point, with potentially devastating effects on the trucking industry greater than those of the typical boom-and-bust cycle.

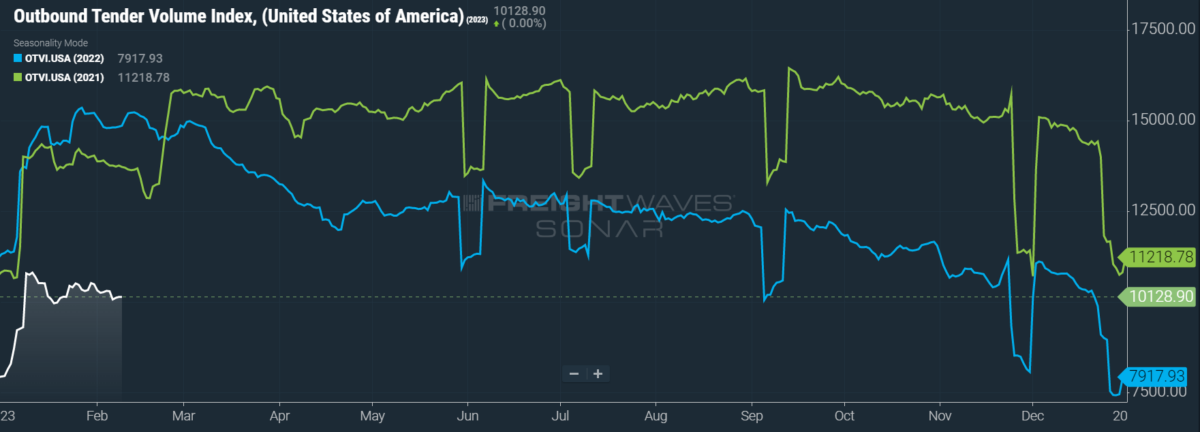

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ request for capacity, slid 1.13% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 32.66%, but such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

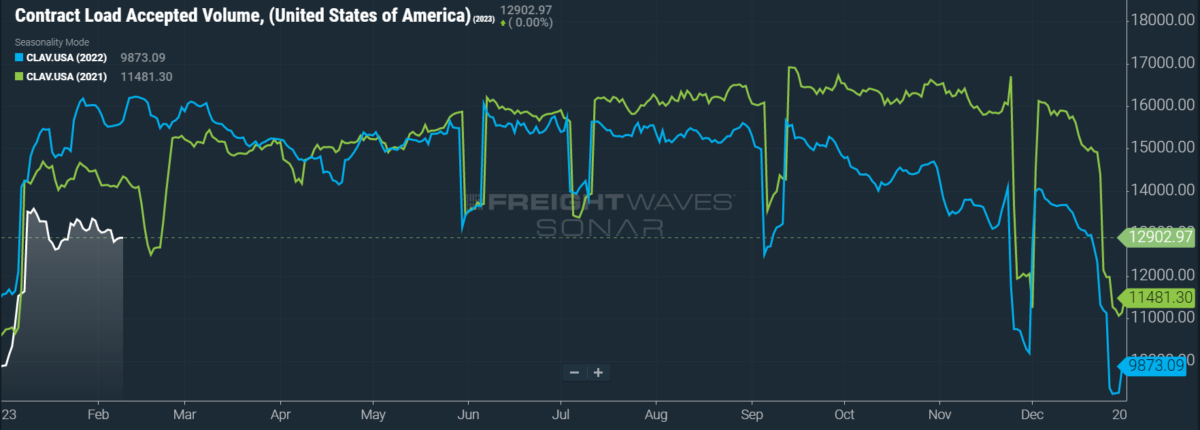

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a dip of 0.93% w/w as well as a fall of 17.6% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

Good news and bad news came for U.S. ocean imports, which are a major driver of domestic truckload volumes. The good news is that containerized imports in January saw their largest month-over-month (m/m) increase since May, rising 7.2%. This latest gain puts maritime volumes close to the pre-pandemic levels of 2019 and ’20, when ocean freight demand had yet to experience the boom of stimulus-fueled consumer spending for bulky durable goods. China, eager to prove its resilience in manufacturing after lifting COVID-related quarantine measures, was key to this latest rise in U.S. imports, accounting for over 70% of the m/m gains among the top 10 countries of origin.

The bad news is that February will almost certainly see a m/m decline in import volumes. On the one hand, such a drop is perfectly seasonal given the Chinese celebration of Lunar New Year, during which manufacturing and exporting facilities shut down. On the other hand, February import volumes are expected to be outpaced by even 2019, which was a less-than-robust year for ocean freight demand (to say the least). In short, with weakened consumer demand and industrial activity, the coming dearth of imports will be another headwind on truckload volumes for the near future.

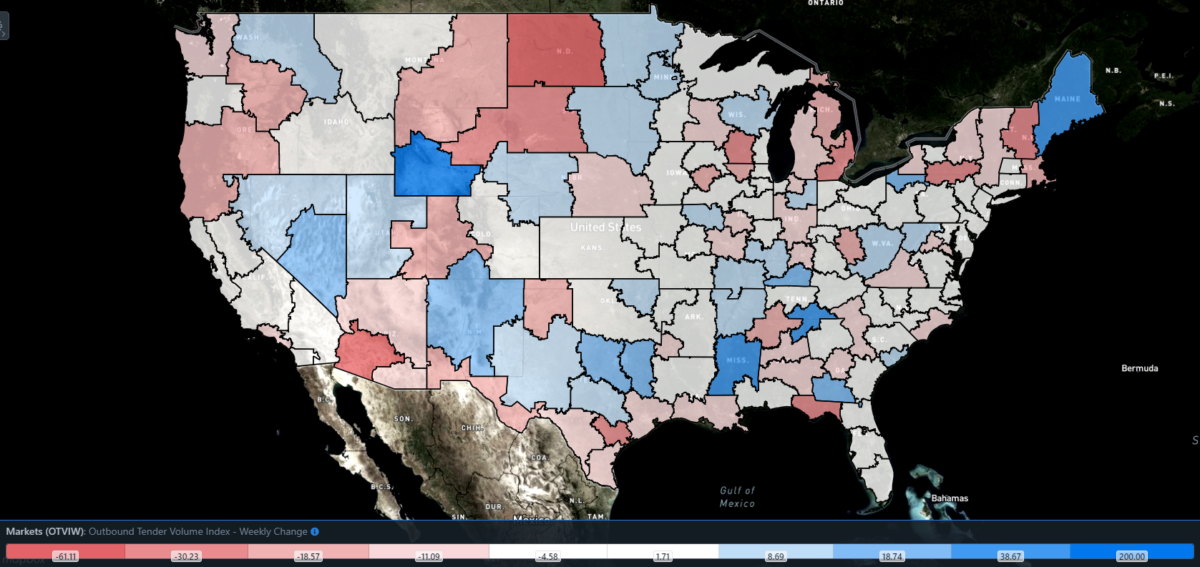

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 62 reported weekly increases in tender volume as truckload markets settled into this year’s rhythm.

Minor improvements in freight activity are being seen in many heavyweight markets this week. The market of Ontario, California — which handles import volumes from the nearby ports of Los Angeles and Long Beach — saw a 1.35% w/w gain in tender volumes, driven by ocean demand slowly returning to West Coast ports. On the flip side, Port Houston has suffered contraction in maritime volumes after a string of record-shattering months, leading truckload volumes in Houston to slide 5.67% w/w. Atlanta is both a regional node in transportation networks and a manufacturing hub in its own right, with volumes rising 4.38% w/w.

By mode: Reefer markets continue to suffer deterioration, especially in contrast to the wild 2021 winter season that brought severe, freezing temperatures and thus exceptional demand for reefers. Depending on where you live, it might be difficult to believe that current temperatures are relatively mild for the season, which is eating away at the Reefer Outbound Tender Volume Index (ROTVI). ROTVI is down 3.17% w/w and a stiff 35.1% y/y.

Van volumes are still the primary driver of the OTVI, as the Van Outbound Tender Volume Index (VOTVI) is down 0.35% w/w. As mentioned earlier, softening retail demand from consumers, which has both seasonal as well as economic causes, is surely impacting the flow of freight, as is the desert of maritime imports coming from China during the Lunar New Year celebrations. VOTVI is also down 32.9% y/y.

Rejection rates keep bottoming out

What more can be said about OTRI? Capacity is now much easier to find than it was at any point in 2019, the year of the trucking industry’s last recession. OTRI’s long decline, which began nearly one year ago, has been the main source of downward pressure on spot rates and is now weighing heavily on contract rates. It remains somewhat difficult to believe that OTRI was hovering around 20% last February.

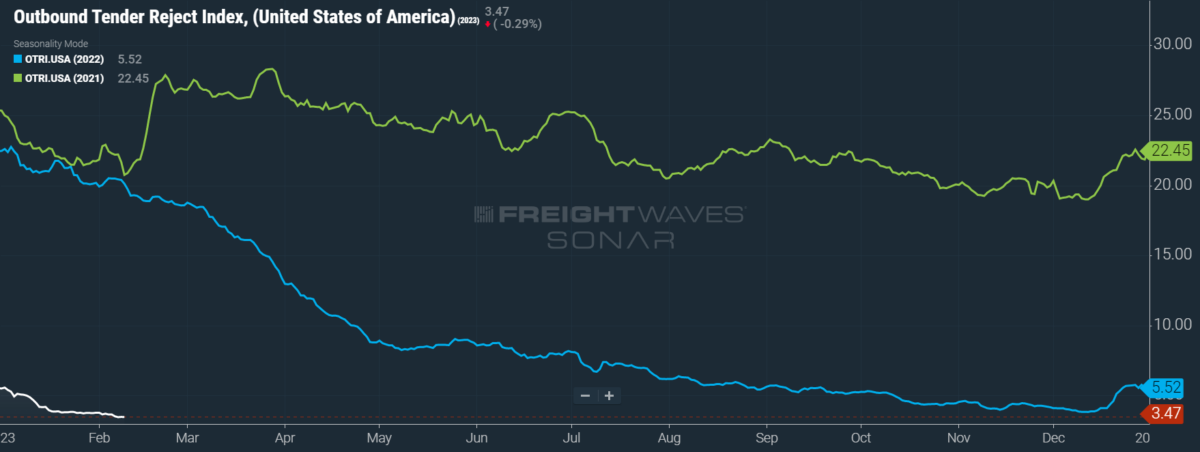

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 3.47%, a change of 19 basis points (bps) from the week before. OTRI is now 1,665 bps below year-ago levels.

In news equally shocking and of little surprise, cargo thefts were on a sharp rise at the end of 2022. Those crimes mainly targeted household goods and consumer electronics, occurring mostly in regions with heavy port activity like California. Overall, cargo thefts were up 15% y/y, with California suffering a 41% y/y jump in stolen goods. Simple breaking-and-entering cases in warehouses and distribution centers were the most common method of stealing, though carriers have also reported thefts of their tractors and trailers in parking lots.

In addition to the classic smash-and-grab, thieves are becoming more sophisticated in their operations. Identity theft, as might occur when cargo thieves pretend to be a legitimate carrier during the pickup, is on the rise. Double brokering, which is when a broker issues a load to a carrier that then re-brokers the load to another carrier, exists in more of a gray market. Rarely, a double-brokered load can arrive safely and with no complications. More commonly, the load is re-brokered to a shady practice that then can hold the cargo hostage or simply take off with the freight.

Double-brokering schemes are like the mythical Hydra: If you cut off one head, two more will grow back in its place. To be sure, these schemes are not built for longevity, as their trucking authority lasts for roughly 30 days on average before the jig is up. Given its insidious nature, double brokering has come under renewed fire by the Transportation Intermediaries Association (TIA), a leading advocacy group for 3PLs. In my brief stint as a broker, avoiding double-brokering schemes was as simple as not signing any carriers with a poor reputation and/or those from Glendale, California. But load board accounts have recently been hacked by these fraudulent actors, one instance of which resulted in 30 to 40 loads being double brokered. The TIA is urging the Federal Motor Carrier Safety Administration (FMCSA) to issue a penalty of $10,000 for each infraction of unauthorized double brokering, though the FMSCA has yet to comment on this proposal.

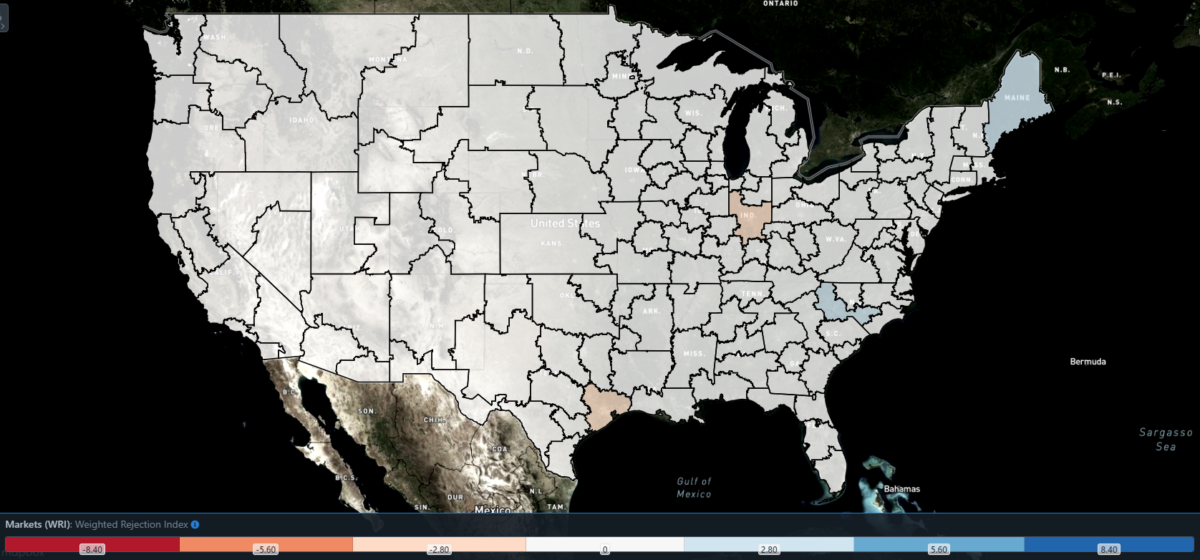

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, only a few regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 54 reported higher rejection rates over the past week, though 34 of those saw increases of only 100 or fewer bps.

Rejection rates spiked in the sleepy market of Augusta, Maine, which is staring down severe winter storms and freezing rain. Although Maine is not a powerhouse in terms of freight activity, it is linked to the port market of Quebec City, Canada, by the Jackman Port of Entry. Augusta’s local OTRI skyrocketed 1,515 bps w/w to 15.27%. Given the usual lack of freight in the market, carriers typically do not need any incentive to leave the region for greener pastures, but severe weather conditions almost always tip the scales of pricing power in favor of carriers.

To learn more about FreightWaves SONAR, click here.

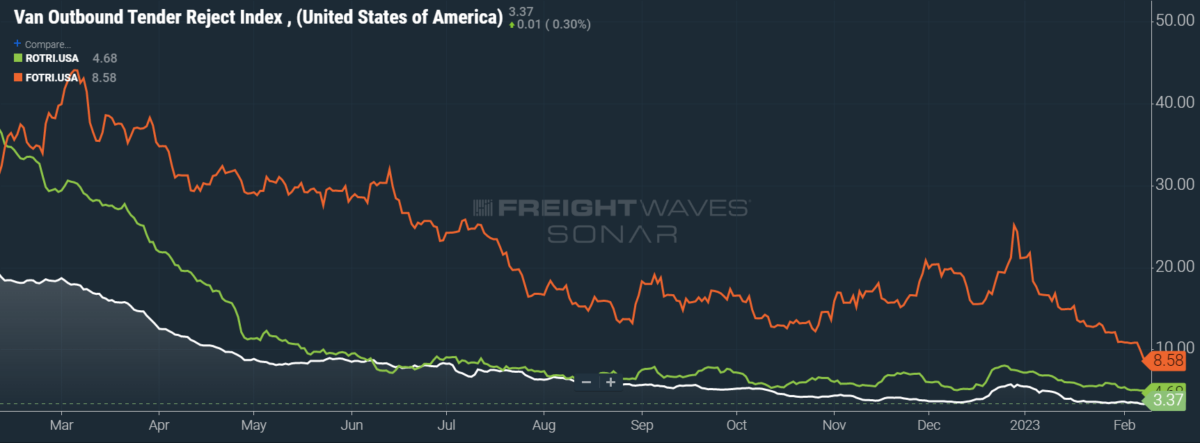

By mode: Flatbed rejection rates, which have been on a roller coaster since the back half of 2022, are firmly locked into a downward spiral. The Flatbed Outbound Tender Reject Index (FOTRI) fell 225 bps w/w to 8.58% — its first foray below 10% since late 2021. For context, FOTRI averaged 8.35% in the recessionary year of 2019. Multiple headwinds have stirred between then and now — namely, weakening demand from the industrial sector and a collapsing housing market.

Compared to flatbeds, other modes seem downright sunny. But the Van Outbound Tender Reject Index (VOTRI) just hit its lowest point since the dark, early pandemic days of May 2020. The Reefer Outbound Tender Reject Index (ROTRI) is even worse, now comparable to April 2020. This week, VOTRI tumbled 13 bps w/w to 3.37% while ROTRI lost 46 bps w/w, falling to 4.68%.

Contract rates maintain steady pace for dismal quarter

Training in philosophy led me to become a knee-jerk skeptic, but my attraction is ultimately to a particular form of idealistic philosophy. Well, idealism be damned. Contract rates are unmistakably settling into their quarterly stride with significant depreciation. If they continue to tread water throughout the first quarter at this level, contract rates will have avoided the worst case scenario, indicating shippers are still too shy to leverage their pricing power for fear of inconsistent capacity. That said, contract rates are still pretty bad, making for a rough Q1 earnings season for major carriers.

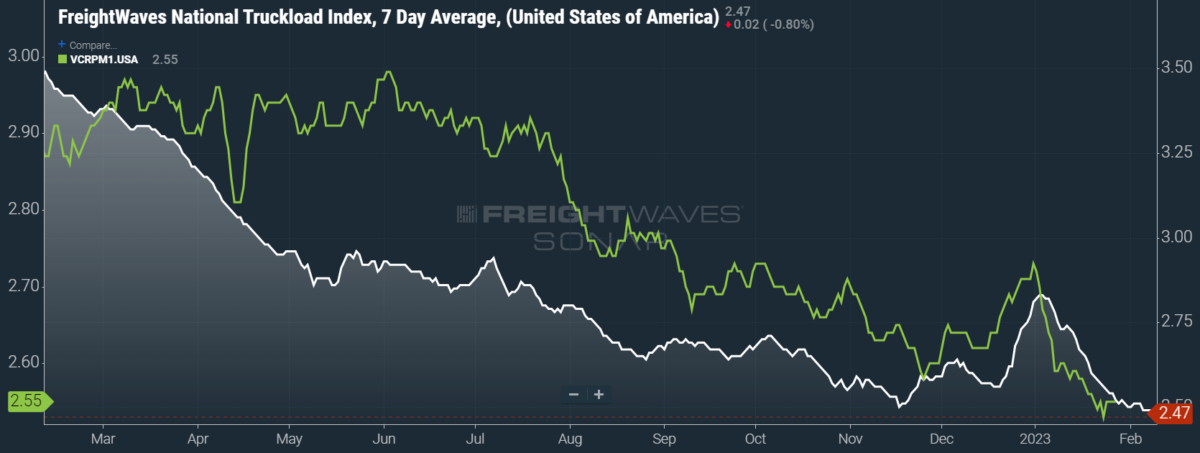

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

Worse than contract rates, however, are spot rates, which cannot seem to find a floor. This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — fell 4 cents per mile w/w to $2.47. Falling diesel prices accounted for roughly half of that stumble, as the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — dipped only 2 cents per mile w/w to $1.76. Any decline in diesel costs is another blow to major carriers that purchase fuel cheaply at wholesale prices but pass on fuel surcharges at higher diesel prices.

Contract rates, which exclude fuel surcharges and other accessorials like the NTIL, held firm at $2.55 per mile, though they did venture down to $2.53 earlier in the week. Since contract rates are reported on a two-week delay, the current data displays trends at the close of January. With January’s rates set in stone, it is rapidly becoming clear that contract rates will not gain from the rise typically seen during the first month of any given quarter.

To learn more about FreightWaves SONAR, click here.

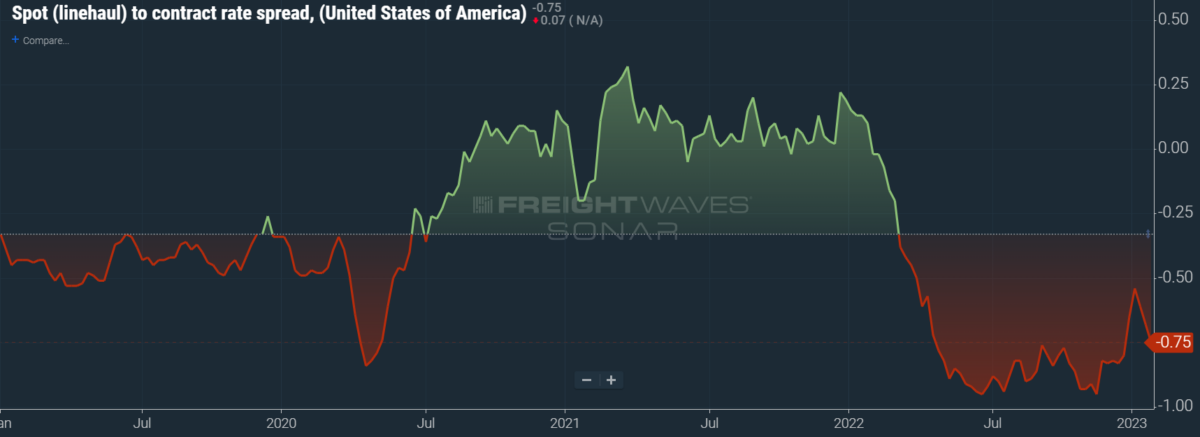

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly over the first few weeks of the year, tightening by 20 cents per mile since mid-December, it has started to widen again. Since linehaul spot rates remain 75 cents below contract rates, there is still runway for contract rates to decline over the coming months.

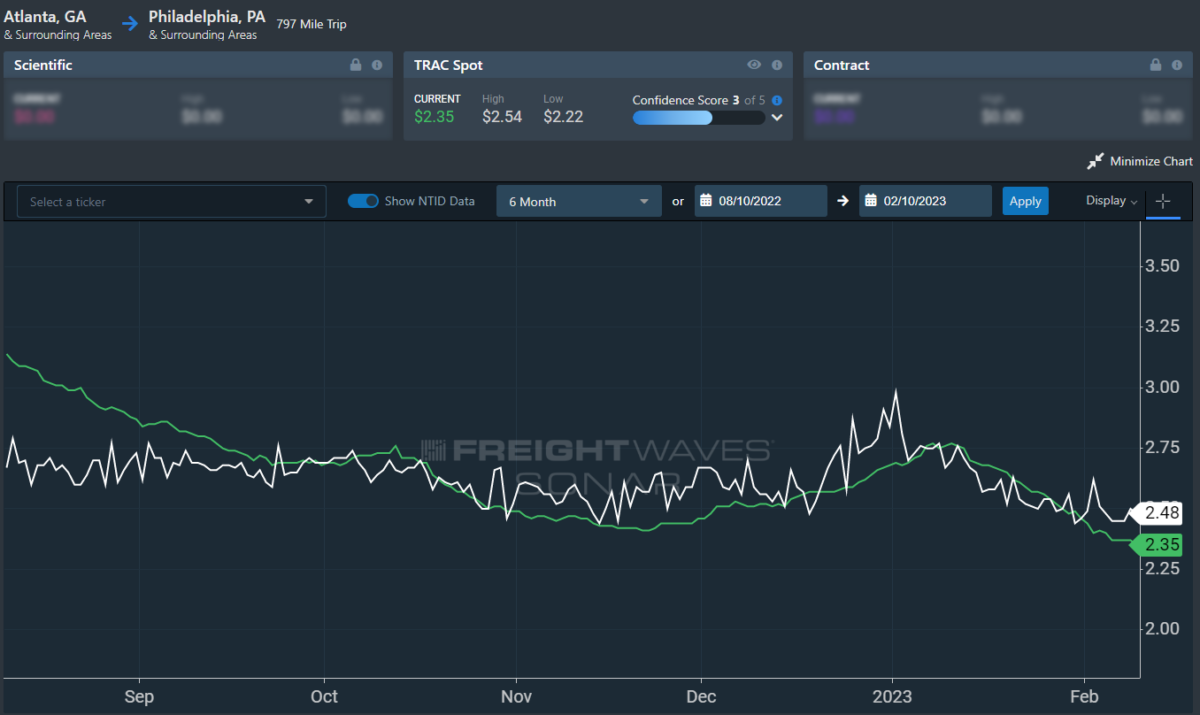

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, is quickly reaching new lows in the data set. Over the past week, the TRAC rate fell 4 cents per mile to $2.18. The daily NTI (NTID), which has fallen to $2.48, continues to outpace rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates are declining more quickly and are separating from the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia fell 5 cents per mile this week to reach $2.35, compounding last week’s loss of 14 cents w/w. Except for Q4’s holiday run, rates along this lane have been dropping stepwise since mid-July, when the TRAC rate was $3.48 per mile.

For more information on the FreightWaves Passport, please contact Michael Rudolph at mrudolph@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.